This article is for current or prospective whole life policyholders and families using life insurance for legacy planning who want to know exactly when cash value becomes taxable. We'll walk through how cash value is taxed at each stage — from accumulation through withdrawals, loans, surrender, and the death benefit — and what factors can shift your tax exposure significantly.

Key Takeaways

- Cash value grows tax-deferred inside the policy — no annual income tax while it accumulates

- Withdrawals up to your cost basis (total premiums paid) are income tax-free; amounts above that threshold are taxed as ordinary income

- Policy loans are not taxable while the policy is active, but taxes apply if the policy lapses or is surrendered with an outstanding loan

- Surrendering a policy triggers a taxable gain when cash surrender value exceeds total premiums paid — you'll receive a Form 1099-R

- The death benefit is generally income tax-free under IRC Section 101(a), but may be subject to estate taxes depending on policy ownership

- Overfunding a policy in its first seven years can trigger MEC status, which permanently changes how withdrawals and loans are taxed

What Whole Life Cash Value Is and How It's Taxed

Every whole life premium payment does two things: it covers the cost of insurance and deposits a portion into a separate accumulation account — the cash value. Over time, that account grows through guaranteed contractual returns, and potentially through dividends if the policy is participating.

The Cost Basis: Your Tax-Free Threshold

The cost basis (also called "investment in the contract") is the total amount of premiums you've paid into the policy, minus any refunded premiums, dividends received, and unrepaid loans. This number matters more than almost anything else when it comes to taxation. Amounts you access up to your cost basis are generally tax-free — because you're simply recovering what you already paid with after-tax dollars.

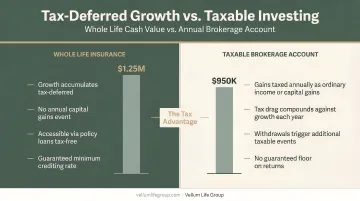

Tax-Deferred Growth Under IRC Section 7702

Your cost basis defines what's tax-free — but the growth on top of it gets a different benefit: tax deferral. As long as the policy qualifies as a life insurance contract under IRC Section 7702, the interest, dividends, and gains accumulating inside it are not subject to annual income tax. A taxable brokerage account, by contrast, can trigger a tax bill every year on realized gains.

The key phrase is tax-deferred, not tax-free. That distinction matters:

- Growth compounds inside the policy without annual IRS reporting

- Tax liability activates only when you access funds in certain ways, or if the policy lapses

- Dividends left inside the policy generally aren't taxed as current income

- Policy termination can trigger a taxable event on all accumulated gains above basis

With whole life specifically, the contractually fixed growth rate keeps the tax math straightforward. There are no market-driven fluctuations to track — which means your cost basis stays predictable, and so does your tax exposure.

Tax Treatment by Scenario: Withdrawals, Loans, Surrender, and the Death Benefit

How the cash value is taxed depends entirely on how — and whether — you access it.

Withdrawals (Partial Surrenders)

For non-MEC whole life policies, withdrawals follow first-in, first-out (FIFO) treatment under IRC Section 72(e)(5). The first dollars withdrawn are treated as a return of premiums paid — meaning they're tax-free. Only the portion above your cost basis is taxed as ordinary income.

Example: You've paid $80,000 in premiums and your cash value is $110,000. If you withdraw $90,000, the first $80,000 is tax-free (return of basis). The remaining $10,000 is taxable as ordinary income.

Keep two risks in mind before withdrawing:

- Withdrawals permanently reduce both the cash value and the death benefit

- Excessive withdrawals can trigger a policy lapse — at which point any remaining untaxed gain becomes taxable immediately

Policy Loans

Borrowing against cash value through a policy loan is not considered taxable income by the IRS. You're using the cash value as collateral, not receiving a distribution. This makes policy loans one of the most tax-efficient ways to access funds inside the policy.

That tax-free status disappears if the policy lapses or is surrendered with a loan outstanding. Under Rev. Rul. 2009-13, the IRS treats the discharged loan balance as part of the surrender proceeds — meaning any amount above your cost basis becomes taxable as ordinary income, even if you receive no cash. Loan interest accrues continuously and erodes cash value, so monitoring the loan balance against available cash value is essential.

Policy Surrender

Fully surrendering a whole life policy ends coverage and triggers a taxable event if the net cash surrender value exceeds your total premiums paid. The gain — surrender value minus cost basis — is taxed as ordinary income in the year of surrender, per IRS Publication 525.

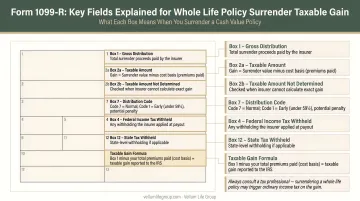

The 1099-R: When a taxable gain exists, the insurance company issues a Form 1099-R. Watch for these specifics when filing:

- Box 1: Total proceeds received

- Box 2a: Taxable amount (gain above cost basis)

- Distribution Code 7: Used for life insurance surrenders

- Form 1040, line 5b: Where you report the taxable portion

The Death Benefit

Under IRC Section 101(a)(1), death benefits paid to named beneficiaries are excluded from gross income — regardless of how large the policy was or how much cash value it had accumulated. Beneficiaries owe no income tax on what they receive.

Estate taxes are a separate question. Under IRC Section 2042, life insurance proceeds are included in your gross estate if you held "incidents of ownership" at death — which generally means owning the policy yourself.

The federal estate tax filing threshold is $13,990,000 for 2025, rising to $15,000,000 for 2026. For estates approaching those levels, an irrevocable life insurance trust (ILIT) removes the death benefit from the taxable estate by shifting policy ownership to the trust.

Factors That Can Change Your Tax Exposure

Modified Endowment Contracts (MECs)

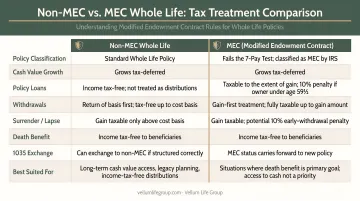

A policy becomes a MEC if cumulative premiums paid in the first seven policy years exceed the IRS-defined 7-pay limit under IRC Section 7702A. Once triggered, MEC status is permanent — distributions during that contract year and every later year are affected.

The tax consequences are significant:

| Feature | Non-MEC Policy | MEC Policy |

|---|---|---|

| Withdrawal order | FIFO (basis first) | LIFO (gains first) |

| Early withdrawal penalty | None | 10% on taxable portion if under age 59½ |

| Loan treatment | Not taxable | Treated as taxable distribution |

A MEC eliminates most of the tax advantages that make whole life cash value attractive in the first place.

Policy Lapse Risk

A lapse — whether from missed premiums or a loan balance that consumes all available cash value — can create taxable income with no cash payment. If the accumulated loan exceeds your cost basis at the time of lapse, that gain is taxable in the year the policy terminates. This is one of the most overlooked tax risks in whole life ownership.

ACLI's 2024 Fact Book reported a 4.3% individual life insurance lapse rate by face amount in 2023 — a meaningful number, not a theoretical edge case.

The Value of Professional Guidance

Structuring a whole life policy correctly requires ongoing attention. An experienced advisor ensures the policy is funded to build cash value without inadvertently crossing the MEC threshold.

Loan balances are equally worth watching — left unchecked, they can gradually erode cash value to the point of lapse.

At Vellum Life Group, Eva Ikonomakos conducts annual policy reviews as part of her ongoing client support across 10+ A-rated carrier partners. These reviews are built to catch issues — like a loan balance growing faster than the cash value — before they create tax problems.

Common Misconceptions About Whole Life Cash Value and Taxes

"Cash value is always tax-free"

Tax-deferred and tax-free are not the same thing. Growth inside the policy avoids annual taxation — but gains above your cost basis on withdrawals, surrenders, and loan lapses are taxable. LIMRA research found that consumers correctly answered only 28% of life insurance comprehension questions on average. Mistaking tax-deferral for tax-exemption is one of the most frequent — and expensive — errors policyholders make.

"Policy dividends are taxable income"

Dividends paid by a mutual life insurance company are generally treated as a return of premium, not taxable income — up to the amount of premiums paid. They represent a partial refund of overpaid premiums — with two important nuances:

- Dividends reduce your cost basis (the IRS adjusts basis for dividends received)

- If you leave dividends with the insurer to accumulate at interest, that interest is taxable in the year it is credited

"Surrendering a policy has no tax consequences because I paid after-tax premiums"

This is the most expensive misconception policyholders carry. The IRS doesn't tax the return of your premiums — it taxes the gain above what you paid in. If your policy has grown significantly, the taxable gain on surrender could be substantial. Before surrendering, request an in-force illustration from your carrier and identify your current cost basis — that number determines exactly what you'd owe.

Conclusion

Whole life insurance cash value offers real tax advantages: tax-deferred growth, income tax-free access up to your cost basis, and an income-tax-free death benefit for your beneficiaries. Those advantages hold — as long as you understand the conditions attached to them.

The nuances around MECs, policy loans, surrender taxation, and lapse risk make this a topic where personalized guidance is worth seeking out. Getting these details wrong doesn't just cost money — it can trigger an unexpected tax bill in an otherwise routine year.

If you're a current policyholder or a family focused on legacy planning, a policy review with a licensed advisor is a smart step before making any major decisions about accessing or exiting a policy.

Eva Ikonomakos at Vellum Life Group offers no-obligation consultations for individuals and families nationwide. She specializes in life insurance and legacy planning, works with 10+ A-rated carriers, and provides ongoing annual reviews as part of her client commitment.

To get in touch:

- Email: info@vellumlifegroup.com

- Phone or text: 917-363-3554

- Schedule online: calendly.com/eva-ikonomakos/30min

Frequently Asked Questions

Is the cash value of a whole life insurance policy taxable when surrendered, and why might I receive a 1099?

Yes — surrendering a policy is taxable to the extent the cash surrender value exceeds your total premiums paid. The insurer is required to issue a Form 1099-R reporting the taxable gain to both you and the IRS, and you report it on Form 1040, lines 5a and 5b.

Will a life insurance payout affect SSDI?

A death benefit paid to a beneficiary generally does not affect SSDI eligibility, since SSDI is based on disability status and work history rather than financial resources. However, if you receive SSI (a separate, means-tested program), life insurance proceeds or investment income from them could affect your eligibility.

Are whole life insurance policy loans taxable?

Policy loans are not taxable income while the policy is active. However, if the policy lapses or is surrendered with a loan outstanding, the unpaid balance is treated as a distribution, and any portion above your cost basis becomes taxable as ordinary income.

How are dividends from a whole life policy taxed?

Dividends are generally not taxable as income up to the amount of premiums paid, because the IRS treats them as a return of premium. However, any interest earned on dividends you leave with the insurer to accumulate is taxable in the year it is credited.

What is a Modified Endowment Contract (MEC) and why does it matter for taxes?

A MEC is a policy overfunded beyond IRS limits in the first seven contract years. Once triggered, MEC status is permanent: it strips the policy of FIFO tax treatment, meaning distributions are taxed gains-first (LIFO), and withdrawals before age 59½ may also carry a 10% penalty.

Can I withdraw from my whole life cash value without paying taxes?

Yes — withdrawals up to your cost basis (total premiums paid) are income tax-free for non-MEC policies. Any amount withdrawn above that threshold is taxed as ordinary income, and withdrawals also permanently reduce the policy's death benefit.