That's not a flaw in how insurance works. It's just a mismatch between a static policy and a life that keeps changing.

Laddering solves this by replacing one large policy with multiple smaller term policies, each sized to a specific obligation and set to expire when that obligation ends. The result: you're never paying for more coverage than you actually need.

This article covers how excess coverage costs accumulate quietly over time, what actually drives your premiums, and six practical strategies for building a ladder — whether you're starting fresh or rethinking a policy you already hold.

Key Takeaways

- Laddering stacks multiple term policies with staggered amounts and end dates, so coverage shrinks as your financial obligations do.

- The biggest savings come from decisions made upfront — buying shorter terms for shorter obligations instead of defaulting everything to 30 years.

- Locking in all policies simultaneously while young captures the lowest possible rates across every layer of the ladder.

- Review your coverage at major life milestones — marriage, new children, paid-off debts.

- An independent advisor with access to multiple carriers can compare pricing across every tier of your ladder simultaneously.

How Life Insurance Costs Accumulate Over Time

Life insurance costs rarely feel excessive month to month. A $75 premium doesn't raise alarms. The problem shows up over years — when you keep paying for $1 million in coverage while the financial reality that justified it has gradually shifted.

Financial responsibilities typically peak in early-to-mid career years: a new mortgage, children under ten, student debt, or personal loans. From there, most of these obligations follow a predictable downward arc.

- Mortgages get paid down

- Children grow up and become independent

- Debts get retired on schedule

The question most people never stop to ask is: What would my family actually need today if I passed away?

For many households, the honest answer is significantly less than what the original policy was written to cover. A 30-year policy purchased at age 32 doesn't automatically recalibrate as your mortgage balance drops from $400,000 to $90,000.

That gap — between what you're covered for and what your family would actually need — is where unnecessary premium costs live. Unlike a subscription you notice going unused, it just keeps renewing without a second glance.

What Drives the Cost of Your Life Insurance Policy

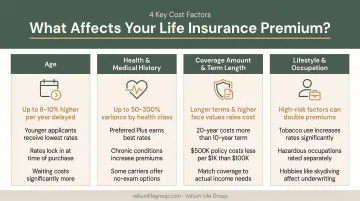

Term life premiums are primarily shaped by four variables:

| Variable | What It Means for Your Premium |

|---|---|

| Age at purchase | Premiums rise 4.5% to 9.2% per year you wait, according to Policygenius's 2024 benchmark data |

| Term length | Longer terms cost more for the same face amount and applicant profile |

| Coverage amount | Higher death benefit = higher premium |

| Health classification | Each table rating below Standard adds roughly 25% to the base rate |

A 30-year-old male can get $500,000 in 20-year term coverage for around $29/month. By age 50, that same policy costs around $102/month — more than three times as much, for identical coverage.

The decision of how much to buy and for how long is the primary lever you control. Overpaying almost always traces back to carrying more coverage than you still need — not to how insurers set their base rates.

That age-to-cost gap is precisely the problem laddering is designed to solve. By splitting one large long-term policy into smaller policies with staggered terms, you stop paying for coverage you've already outgrown at each stage of life.

How to Build a Life Insurance Ladder Strategy

The right ladder looks different for everyone. It depends on which financial obligations you're protecting against, how those obligations change over time, and how actively you're willing to manage coverage along the way. But the underlying mechanics follow a consistent logic.

Strategies That Reduce Costs Through Upfront Decisions

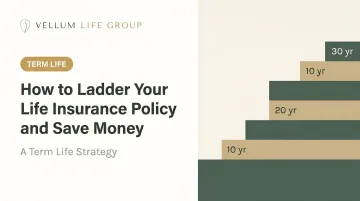

Strategy 1: Buy multiple shorter-term policies instead of one maximum-term policy.

The clearest published illustration comes from NerdWallet's 2025 laddering analysis: a 30-year-old in excellent health splits $1 million in coverage into three policies — $500K for 10 years, $300K for 20 years, and $200K for 30 years — and pays $10,470 in total premiums over 30 years. A single $1M, 30-year policy for the same applicant runs $16,260 total. That's nearly $5,800 in savings.

The math is straightforward: the 10-year and 20-year layers expire when those obligations end, so you stop paying for them. Only the longest-term obligation carries coverage for the full 30 years.

Strategy 2: Lock in rates while young and healthy.

Every year you wait to buy costs more. The ladder only captures this advantage if all three policies are purchased simultaneously — not sequentially. Buying a 20-year policy at 30 and then adding a second policy at 40 defeats the purpose, because the second policy gets priced at your older age and potentially worse health classification.

Starting the full ladder at once, while young and healthy, locks in the lowest available rates across every tier.

Strategy 3: Match each policy to a specific financial obligation.

Arbitrary term lengths leave money on the table. Each layer of the ladder should align with a concrete liability:

- A 10-year policy for student loans (standard repayment runs 10 years)

- A 20-year policy for child dependency coverage (Pew Research data shows full financial independence often extends into the early 30s)

- A 30-year policy for a long-term mortgage or income replacement through retirement

Sizing each layer to the actual obligation — not a round number — avoids both over-coverage and gap years.

Strategies That Reduce Costs Through Active Management

Strategy 4: Review coverage at major life milestones.

A mortgage payoff, a child becoming financially independent, or a significant income change — these aren't just life events, they're signals to reassess whether your current coverage still reflects actual need. Skipping these reviews means continuing to pay for obligations that no longer exist.

Vellum Life Group includes annual policy reviews as part of its ongoing client support, specifically to catch these moments and adjust coverage accordingly.

Strategy 5: Coordinate with group life insurance coverage.

BLS data from March 2025 shows that access to group life insurance ranges from 42% at small organizations to 87% at large ones, with typical coverage equal to one times annual salary. That's a meaningful supplement — but not a foundation. Group coverage often ends when the plan ends, and portability is limited.

The practical approach: size your private ladder around what the group plan doesn't cover, and adjust when your group benefits change.

Strategy 6: Drop policies intentionally as obligations are met.

When a policy's purpose has been fulfilled — the mortgage is paid, the kids are independent — allowing it to expire is a deliberate cost-reduction step. That's the ladder working as designed, not a coverage gap. The remaining policies continue to cover whatever obligations are still active.

The Broader Context: Why Working With an Independent Advisor Matters

Designing a ladder requires comparing term lengths, pricing, and underwriting criteria across multiple carriers simultaneously. A 10-year policy and a 30-year policy on the same applicant may be priced most competitively by two different insurers — and you won't know that unless you can see the full market.

An independent advisor like Eva Ikonomakos at Vellum Life Group has access to 10+ A-rated carriers, so each tier of your ladder can be placed with whichever insurer offers the best pricing for that specific term — not whatever a single carrier happens to offer. The initial consultation is free and starts by mapping coverage to your actual financial obligations, before any policy is recommended.

When Laddering Life Insurance Makes the Most Sense

Laddering works best when financial obligations follow an uneven, declining trajectory over time. The ideal candidates:

- Young families with a mortgage, children under 10, and ongoing student debt — three obligations with three different end dates

- Dual-income households where each income stream needs separate protection for a defined period

- Individuals with personal loans that will be paid down or retired over time, alongside income replacement needs

Laddering isn't the right fit for every situation, though:

- If your primary obligation is a single 30-year mortgage with no other major liabilities, one well-sized policy may be simpler and equally cost-effective

- If your financial picture is unpredictable or not expected to decline in a clear pattern, managing multiple policies adds complexity without guaranteed savings

- If a major life change occurs — a divorce, a new dependent, or new financial obligations — the ladder structure needs to be reassessed entirely, not just maintained on autopilot

Like any financial strategy, a ladder works only as long as it reflects your actual life — which means revisiting it when circumstances shift, not just setting it and walking away.

Conclusion

Reducing life insurance costs means aligning your coverage with your actual financial obligations at each stage of life, not locking in the worst-case scenario from a decade ago.

A well-designed ladder accomplishes this by letting coverage shrink as obligations shrink, while keeping the right protection in place for as long as it's genuinely needed.

If you're not sure whether your current coverage matches where your life actually is right now, a conversation with an independent advisor is the fastest way to find out. Vellum Life Group offers a free, no-obligation consultation to walk through your coverage, map it to your financial timeline, and identify where a ladder strategy might reduce what you're paying without leaving your family underprotected.

Reach out at info@vellumlifegroup.com or call 917-363-3554 to get started.

Frequently Asked Questions

Is laddering life insurance worth it?

For people with predictable, declining obligations — a mortgage, young children, student debt — laddering avoids years of overpaying for coverage that exceeds actual need. It requires upfront planning and periodic review, so it works best for those willing to manage coverage actively over time.

Can you have multiple life insurance policies at the same time?

Yes. Holding multiple term life policies simultaneously is legal and common — it's exactly what the ladder strategy relies on. Insurers will review your total coverage in force during underwriting, with limits typically tied to age and income (up to 35x annual income for applicants under 40).

What is the difference between laddering up and laddering down?

Laddering down means allowing policies to expire or reducing coverage as financial obligations decrease. Laddering up means adding new coverage when new responsibilities arise — a new mortgage, a child, or a new loan. Both are valid adjustments as your financial picture changes.

Does laddering life insurance work with whole life insurance?

The ladder strategy applies to term life insurance, which has defined end dates and lower premiums that make stacking affordable. Whole life insurance doesn't expire and builds cash value over time — it serves different planning purposes and isn't designed to be layered and dropped as obligations end.

When should I reassess my life insurance ladder strategy?

Review your ladder after any major milestone: marriage, divorce, a new child, paying off a mortgage, a job change, or a child becoming financially independent. Any shift in your obligations is a signal to check whether your coverage still matches what your family would actually need.

How much is a $500,000 life insurance policy for a 70-year-old man?

Premiums rise sharply with age. Policygenius's 2024 benchmark puts a 70-year-old male non-smoker in Preferred health at $456.78/month for a $500,000 10-year term policy. Coverage locked in at 30 or 35 costs a fraction of that — which is the core financial case for laddering early.