Life insurance fills that gap. A death benefit can reach named beneficiaries within weeks, while the probate process often takes a minimum of four months — and frequently longer for complex estates. That timing difference matters enormously for families facing estate taxes, settlement costs, or estate transfer decisions.

This article covers the key decisions: which policy type makes sense for estate planning, how to use life insurance to solve specific inheritance problems, how an Irrevocable Life Insurance Trust (ILIT) can keep proceeds outside your taxable estate, and which mistakes to avoid.

Key Takeaways

- Permanent life insurance (whole or universal) fits estate planning better than term — estates don't expire

- Naming a living beneficiary on your policy keeps proceeds out of probate entirely

- An ILIT removes the death benefit from your taxable estate, but requires you to give up policy ownership

- Beneficiary designations override your will — outdated forms can redirect assets to the wrong people

- The right policy depends on your estate size, family structure, and goals

What Is Estate Planning and Where Does Life Insurance Fit In?

Estate planning is the process of organizing your assets, designating beneficiaries, and creating legal documents (wills, trusts, powers of attorney) so your wealth transfers according to your wishes. If you have dependents, property, or anything you want to pass on, you have an estate worth planning.

Most people don't get there, though. According to Caring.com's 2025 survey, only 24% of American adults have a will, 13% have a living trust, and 56% have no estate plan at all. Even among those with basic documents in place, life insurance is often missing from the picture.

Why Life Insurance Belongs in the Plan

Most estate assets — real estate, investments, and other holdings — take time to convert to cash. They move through legal processes, valuations, and transfers. Life insurance operates differently. When a named beneficiary is on file, the death benefit transfers directly, outside of probate, often within 30 to 60 days of a claim.

Estates frequently face immediate cash demands:

- Federal estate taxes due within 9 months of death

- Probate and settlement costs that arrive before assets can be liquidated

- Inheritance equalization when assets can't be divided evenly among heirs

- Estate succession funding when an estate transfer occurs unexpectedly

Life insurance provides the liquidity to meet those demands without forcing heirs to sell property at the wrong time.

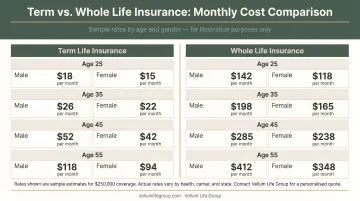

Term vs. Permanent Life Insurance for Estate Planning

Not all life insurance serves the same purpose. For estate planning specifically, the type of policy matters.

Term Life Insurance

Term coverage provides a death benefit for a defined period (typically 10 to 30 years), with lower premiums and no cash value accumulation. It's well-suited for temporary needs: covering a mortgage while children are young, or closing a specific financial gap.

For estate planning, term coverage has a structural problem. Your estate doesn't expire on a schedule. If the goal is to transfer wealth at death (whenever that occurs), a policy that lapses after 20 years doesn't guarantee anything.

Permanent Life Insurance

Whole life and universal life policies provide lifetime coverage as long as premiums are paid. They build cash value over time and guarantee a death benefit regardless of when the policyholder dies. That unconditional guarantee is what makes permanent coverage the logical fit for estate planning.

Whole life offers fixed premiums and a guaranteed death benefit — consistent and easy to plan around.

Universal life offers more flexibility: adjustable premiums and death benefit amounts that can shift as your financial situation changes.

Neither is universally better. The right choice depends on your age, budget, health, and specific estate goals.

The Cost Trade-Off

Permanent coverage costs significantly more than term. According to Forbes Advisor, a 30-year-old woman can expect to pay roughly $16/month for $500,000 in term coverage versus $329/month for a comparable whole life policy — about 20 times more. For a 50-year-old man, that gap narrows to roughly 12x.

That cost reflects lifetime coverage and cash value growth, not just a higher price tag. The younger and healthier you are when you apply, the more affordable permanent premiums become — which is why delaying the decision tends to cost more than making it.

Key Ways Life Insurance Strengthens Your Estate Plan

Life insurance isn't just a safety net in an estate plan — it's a targeted tool that solves specific problems most families will eventually face.

Covering Estate Tax Liability

Current federal estate tax thresholds:

- 2025 exemption: $13,990,000 per individual ($27,980,000 for married couples with portability)

- 2026 exemption: $15,000,000, per current IRS guidance

- Tax rate above exemption: Up to 40%, due within 9 months of death

Fewer than 0.2% of estates currently trigger federal estate tax. But estates concentrated in appreciating real estate, farmland, or collectibles can cross those thresholds as values compound over decades. Exemption amounts have also shifted significantly over time — today's comfortable margin can narrow quickly under new legislation.

A life insurance payout provides the cash to cover that tax bill without forcing heirs to sell assets at the wrong moment.

Equalizing Inheritance Among Heirs

Hard-to-divide assets create hard family conversations. When one heir receives the family farm, a primary residence, or other illiquid property, it's difficult to provide comparable value to siblings who receive nothing tangible.

Life insurance solves this cleanly. The heir who takes over the family farm or estate property receives that asset. Other heirs receive a death benefit of comparable value through the policy. The University of Nebraska's Center for Agricultural Profitability specifically cites this approach — second-to-die permanent policies are commonly used to equalize estates when one heir continues farming and others don't.

Assets stay intact, and so does the inheritance each heir receives.

Supporting an Heir With Special Needs

A direct inheritance to a dependent with disabilities can disqualify them from SSI or Medicaid. The SSA's current SSI resource limits are $2,000 for an individual and $3,000 for a couple — a threshold most inheritances would immediately exceed.

The solution: name a Special Needs Trust (SNT) as the policy beneficiary. The trustee pays qualifying expenses directly on behalf of the beneficiary without transferring countable resources. Government benefits stay in place, and ongoing care stays funded through the trust.

Providing Liquidity for Business Succession

Estate succession and inheritance arrangements often require careful planning to ensure assets transfer efficiently and that all heirs are treated equitably. Life insurance can provide the liquidity to facilitate these transfers without forcing rushed asset sales.

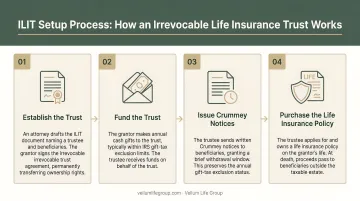

How an Irrevocable Life Insurance Trust (ILIT) Works

Here's a problem that surprises many families: if you own a life insurance policy at death, the entire death benefit is included in your taxable estate under IRC Section 2042. A policy purchased specifically to cover estate taxes can inadvertently increase the taxable estate instead.

An ILIT fixes this by removing the policy from your estate entirely. Here's how the structure works:

How an ILIT Is Set Up

- The grantor creates an irrevocable trust, naming a trustee (not themselves) and beneficiaries — typically children or other heirs

- The trust applies for and owns the life insurance policy on the grantor's life

- The grantor funds premium payments through annual gifts to the trust

- At death, proceeds pass to beneficiaries outside the taxable estate

The 2025 annual gift tax exclusion is $19,000 per donee, which often covers premium payments without triggering gift tax.

The Crummey Provision

For gifts to the trust to qualify for the annual exclusion, they must be "present interest" gifts. A Crummey provision gives beneficiaries a short withdrawal window — typically 30 to 60 days — on each contribution, satisfying this requirement. Beneficiaries almost never exercise that right, but the legal structure is what makes the gift tax exclusion work.

Key Limitations

- No going back: Once the trust owns the policy, the grantor gives up control permanently

- The 3-year lookback: Under IRC Section 2035, if an existing policy is transferred into an ILIT and the grantor dies within three years, the death benefit is pulled back into the taxable estate

The clean solution: have the ILIT purchase a new policy from the start, rather than transferring an existing one.

Is Life Insurance in an Estate Plan Right for You?

Profiles That Benefit Most

Life insurance adds the most value to an estate plan when one or more of these apply:

- Illiquid estate: Real estate, farmland, or collectibles that can't be easily divided or quickly sold

- Potential estate tax exposure: Estates approaching or exceeding the exemption threshold, especially with appreciating assets

- Multiple heirs, unequal assets: Situations where fair division is genuinely difficult

- Estate complexity: Illiquid assets, inheritance equalization, or succession funding needs

- Dependent with disabilities: Long-term care needs that require benefit-preserving SNT structure

Who May Not Need It

Not every estate has a liquidity problem. If your assets can cover all obligations without a forced sale and you have no dependents requiring long-term support, life insurance may add little value to your estate plan.

The key is an honest assessment of whether your estate has the kind of complexity that life insurance can actually solve.

Getting the Policy Right

The right coverage amount, policy type, and ownership structure depend entirely on individual circumstances. A thorough review should address:

- Coverage amount relative to estate liabilities and liquidity gaps

- Policy type (term, whole, or universal) based on timeline and goals

- Ownership structure to avoid unnecessary estate inclusion

- Carrier selection across A-rated options for competitive pricing

Vellum Life Group works with clients to match the right policy to the estate plan — not the other way around. A free, no-obligation consultation is available to get started.

Common Mistakes to Avoid

Naming the Estate as Beneficiary

Naming your estate rather than a specific person or trust as beneficiary routes the death benefit through probate — a public, time-consuming process that delays access and adds costs. Always name a living individual or a properly structured trust.

Failing to Update Beneficiary Designations

Life changes. Beneficiary designations often don't keep up. As the Ohio State Bar confirms, a life insurance policy payable to named beneficiaries is completely unaffected by what a will says — the designation controls.

Update your designations after any of these events:

- Divorce or remarriage

- Birth or adoption of a child

- Death of a named beneficiary

- Significant change in financial circumstances

Vellum Life Group includes annual reviews and beneficiary change assistance as part of its ongoing client support — because outdated forms are one of the most common ways a well-built plan fails at the moment it matters most.

Assuming the Death Benefit Is Outside the Taxable Estate

Ownership matters here. If the insured owns the policy at death, the full death benefit is included in the gross estate for tax purposes. Families who purchased insurance specifically to cover estate costs sometimes discover it increased their taxable estate instead. An ILIT — or a change in policy ownership — resolves this, but it has to be set up correctly and well in advance.

Frequently Asked Questions

How does life insurance work with estate planning?

A life insurance death benefit can pay estate taxes, cover settlement costs, equalize inheritance among heirs, or fund a trust. Whether it helps or complicates your plan depends on who owns the policy and who is named as beneficiary — getting both right determines whether the benefit reaches your heirs efficiently.

Can a son buy a $500,000 life insurance policy for his father?

Yes — an adult child can purchase a policy on a parent's life, provided insurable interest exists (the child would suffer a financial loss from the parent's death) and the parent consents to and participates in underwriting.

What is the most common inheritance mistake?

Failing to update beneficiary designations after major life events — divorce, remarriage, a new child, or the death of a named beneficiary. These designations legally override your will, which means an outdated form can send assets to an ex-spouse or a deceased individual.

Do life insurance proceeds go through probate?

No — when a living beneficiary is named directly on the policy, proceeds transfer outside of probate entirely and are typically paid within 30 to 60 days. Proceeds only enter probate if the estate itself is named as the beneficiary, or if no living beneficiary is available.

Is a life insurance death benefit taxable to beneficiaries?

Under IRC Section 101(a)(1), death benefits are generally income tax-free when received as a lump sum. However, if the insured owned the policy at death, the full benefit may be included in the gross estate for estate tax purposes.

When should I review my life insurance as part of my estate plan?

At least once a year, and after any major life change — marriage, divorce, the birth of a child, an inheritance, or a significant change in net worth. As estate values grow or tax laws shift, both coverage amounts and ownership structures may need to be revisited.