But the pitch and the reality don't always match. IUL can be a genuinely useful financial tool for the right buyer. It can also be an expensive, complicated product that underdelivers for people who weren't a good fit to begin with.

This article gives you an honest look at both sides — how IUL actually works, what the real benefits are, what the real drawbacks are, and how to figure out whether it belongs in your financial plan. It's written for people considering IUL for the first time, those who've already been pitched a policy, and anyone comparing IUL against simpler alternatives like term or whole life.

Key Takeaways

- IUL ties cash value growth to an index like the S&P 500, but your money is never directly in the market

- A 0% floor prevents index losses, though ongoing fees can still erode cash value in flat or down years

- Participation rates and crediting caps limit gains — strong market years won't translate to full returns

- Best suited for high earners who've maxed other tax-advantaged accounts and want permanent, tax-efficient coverage

- A poor fit for anyone who simply needs affordable, straightforward death benefit protection

How IUL Insurance Works

When you pay premiums into an IUL policy, those premiums don't go entirely to work for you. A portion covers the cost of insurance and various policy fees. The remainder builds your cash value. That cash value then earns interest based on the performance of a chosen stock market index — typically the S&P 500 — through a crediting formula managed by the insurer.

Your money is never actually invested in the market. The insurer credits interest using a formula tied to index performance, but you don't own index shares. Pacific Life's own disclosures state that IUL products "do not directly participate in stock or equity investments."

Caps, Floors, and Participation Rates

Three terms control how much interest actually gets credited to your cash value:

- Floor — the guaranteed minimum credit, usually 0%, meaning your cash value won't drop due to index losses alone

- Cap — the maximum interest rate that can be credited, regardless of how well the market performs

- Participation rate — the percentage of the index's gain that gets applied to your policy

A concrete example: if the S&P 500 gains 18% in a given year but your policy cap is 10%, you receive 10%. If the index gains 6% but your participation rate is 60%, you receive 3.6%.

Caps and participation rates are not guaranteed. They're set by the insurer and can be adjusted periodically. Midland National's index selections guide explicitly states that these rates are "current rates and are subject to change."

What looks attractive in an illustration today may look very different five years into the policy.

The Real Benefits of IUL Insurance

Downside Protection with Upside Potential

The 0% floor is a genuine differentiator. In years when the index drops — as it did significantly in 2022 — your cash value doesn't follow it down due to index losses. Compare that to direct market investment, where you absorb every loss, or a fixed whole life policy, where growth is predictable but typically lower. For risk-conscious buyers who want some growth potential without full market exposure, this trade-off is meaningful.

Tax-Deferred Growth and Tax-Free Access

Cash value in an IUL grows without annual tax liability. Policy loans are generally income-tax-free as long as the policy stays in force and hasn't been classified as a Modified Endowment Contract (MEC). Withdrawals up to your cost basis — the premiums you've paid — are also typically tax-free under IRC Section 72.

This makes IUL most useful for high earners who've already maxed out their 401(k) and IRA — it creates another bucket for tax-advantaged accumulation. There's also a lesser-known Social Security angle worth noting:

- Policy loan proceeds don't count as wages or freelance or independent income for the Social Security earnings test

- According to SSA POMS guidance, bona fide loan proceeds carry a repayment obligation — so they're not treated as income

- For retirees drawing on a policy before full retirement age, this can meaningfully reduce benefit reductions

Flexibility and Permanent Coverage

Unlike whole life's rigid fixed premiums, IUL lets you pay more in prosperous years to accelerate cash accumulation or reduce payments during financial hardship — as long as cash value covers ongoing charges. You can also adjust the death benefit over time.

Term insurance expires. An IUL policy with adequate premium contributions provides lifelong coverage — which matters when the timing of the death benefit is part of the plan. Legacy transfers and estate equalization depend on coverage that doesn't have an expiration date.

The Hidden Drawbacks of IUL Insurance

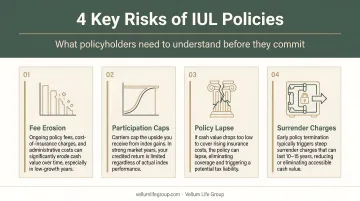

Fees Can Erode Returns

This is where the pitch diverges most sharply from reality. IUL policies carry multiple cost layers:

- Premium expense charges — Nationwide's IUL product disclosures list charges of 8% in year 1 and 6% in subsequent years, with a 10% guaranteed maximum

- Monthly cost of insurance (COI) — deducted monthly and increasing as you age

- Administrative fees — Nationwide lists a $10 current monthly per-policy fee ($20 guaranteed maximum)

- Indexed account charges — additional fees tied to specific account options

These charges continue regardless of whether the index credits any interest. In a year where the index gains nothing and the floor applies, you still pay all of them. That means your cash value can decline even in a zero-index-return year.

Caps and Dividends Mean You're Not Getting Market Returns

When an advisor shows you S&P 500 historical performance to justify an IUL's growth potential, they're showing you the wrong number. IUL index accounts track price return only — dividends are excluded. According to S&P Dow Jones Indices, dividends have contributed approximately 31% of S&P 500 total return since 1926. In some decades, that figure was much higher.

Add crediting caps on top of dividend exclusion, and the actual returns credited to your policy in strong market years are a fraction of what headline index performance suggests.

Surrender Charges Lock Up Your Money

Withdrawing or canceling a policy in the first 10–15 years typically triggers steep surrender charges. If you fund an IUL policy and then face a major financial disruption — job loss, medical expenses, or unexpected costs — you'll either pay steep penalties to access it or be locked out entirely.

Treat IUL as a decade-plus commitment. If there's any chance you'll need that cash in the first five to ten years, the surrender charge structure alone makes it the wrong product.

Policy Lapse Risk Is Real

Surrender charges aren't the only structural threat. If cash value falls too low to cover rising insurance costs, the policy can collapse entirely. This risk compounds when:

- Premiums fall short of what's needed to sustain coverage

- Policy loans grow large enough to drain available cash value

- Crediting rates stay persistently low for multiple consecutive years

A lapsed policy with outstanding loans can trigger a significant unexpected tax bill, even if you receive no cash.

The New York Department of Financial Services warned in 2019 that internal charges can increase annually and policies may lapse when premiums or cash value are insufficient.

A SOA-LIMRA lapse study covering 33.5 million policy exposures found that IUL lapse rates rose sharply between 2015–2018 and 2019–2020 — a real-world signal that these risks aren't theoretical.

IUL vs. Other Life Insurance Options

Before deciding whether IUL fits your situation, it helps to see it against the alternatives:

| Product | Coverage Type | Cash Value | Premiums | Best For |

|---|---|---|---|---|

| Term Life | Temporary (10–30 yrs) | None | Lowest | Maximum death benefit at lowest cost |

| Whole Life | Permanent | Guaranteed growth | Fixed, higher | Predictable, guaranteed cash value |

| IUL | Permanent | Index-linked, capped | Flexible | High earners wanting tax-efficient growth |

| VUL | Permanent | Direct market investment | Flexible | Higher risk tolerance, no floor protection |

The right choice depends on your primary goal:

- Maximum death benefit at low cost → term wins. A 30-year-old male can get $250,000 of 20-year term coverage for roughly $14/month, according to Forbes 2026 benchmarks

- Simple, guaranteed, predictable cash value → whole life makes more sense

- Permanent coverage with growth potential and comfort managing complexity → IUL may fit

Is IUL Right for You?

Buyers Most Likely to Benefit

IUL tends to make the most sense for a specific profile:

- High earners who have already maxed 401(k) and IRA contributions

- Individuals who genuinely need permanent life insurance coverage — not just temporary income replacement

- Those with a 15+ year time horizon and the ability to fund premiums consistently

- Business owners using IUL for key-person coverage or tax-advantaged wealth transfer

- People comfortable actively monitoring a financial product over time

Buyers Who Should Look Elsewhere

IUL is probably the wrong fit if you:

- Primarily need affordable death benefit protection

- Want simple, guaranteed products without complexity

- Haven't yet maximized your 401(k) or IRA

- Have short-term cash needs or uncertainty about sustaining long-term premiums

- Are unwilling or unable to review in-force illustrations annually

Questions to Ask Before Buying an IUL Policy

Use these questions to evaluate any IUL before signing:

- What are current caps, participation rates, and floors — and how often can the insurer change them?

- What is the full fee structure in year 1 and over 10 years? Ask for actual dollar amounts, not just percentages.

- What happens if cash value becomes insufficient to cover policy charges?

- Can you see multi-scenario illustrations — low, moderate, and high crediting rate assumptions — not just the optimistic base case?

- What are the surrender charges, and how long do they last?

These questions matter because IUL policies vary significantly across carriers in caps, floors, participation rates, and fee structures. Comparing multiple illustrations side by side — rather than reviewing a single carrier's best case — is the only way to make an informed decision. An independent advisor like Vellum Life Group, who works with multiple A-rated carriers, can walk through those comparisons with you and help you choose based on the full picture.

Frequently Asked Questions

Can you take money from your IUL anytime you want?

Access is generally available through policy loans or withdrawals, but early withdrawals in the first 10–15 years may trigger surrender charges. Outstanding loans reduce your death benefit and may trigger a taxable lapse if they grow too large relative to cash value.

Can you lose money in an IUL policy?

The 0% floor protects against index-driven losses, but ongoing policy fees and rising cost of insurance charges can still erode cash value — particularly in flat or low-crediting years. A policy that lapses with outstanding loans can also trigger a taxable event even if you received no cash.

What is the downside of IUL insurance?

IUL comes with several compounding drawbacks:

- Multiple fee layers that erode returns over time

- Crediting caps that limit gains in strong markets

- Dividend exclusion from the tracked index

- Surrender charges for early exit

- Lapse risk if the policy is underfunded

Is IUL better than a 401(k) for retirement savings?

No — IUL is not a replacement for a 401(k) or IRA. Those accounts should be maximized first. IUL can serve as a supplemental strategy for high earners who have already exhausted other tax-advantaged options and need permanent death benefit coverage alongside retirement savings.

Who should NOT buy an IUL policy?

IUL is a poor fit for:

- Anyone who needs maximum coverage at the lowest cost

- Those who prefer simple, guaranteed products

- Anyone who hasn't yet maxed out their 401(k) or IRA

- Individuals unwilling or unable to actively monitor a complex policy over many years