Introduction

Most people want to leave something meaningful behind — not just memories, but a financial foundation their family can actually build on. That wish is real. Acting on it is where many people get stuck.

"Legacy life insurance" is a term that trips people up because it sounds like a specific product you can buy off a shelf. It isn't. It's a purpose — using life insurance with the deliberate goal of protecting and transferring wealth to the people or causes that matter most to you.

According to LIMRA's 2025 data, 42% of Americans cite leaving an inheritance as a reason they own life insurance — yet nearly 100 million adults still say they need more coverage than they have. That gap between intention and action is exactly what this guide addresses.

This guide covers what legacy life insurance actually means, the policy types that support it, who benefits most, how health history affects eligibility, and how to find the right approach for your situation.

Key Takeaways

- Legacy life insurance is a purpose-driven use of life insurance, not a separate product category

- Permanent policies (whole life, universal life) are best suited for long-term wealth transfer

- Death benefits are generally income-tax free for beneficiaries, making life insurance one of the most efficient wealth transfer tools available

- Medical conditions may affect premiums but rarely prevent coverage entirely

- Carrier rates and underwriting standards vary widely, so comparing options is the fastest way to find the right fit at the right price

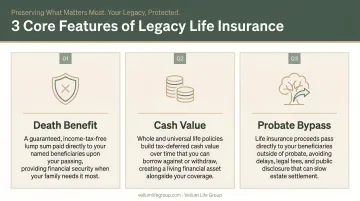

What Is Legacy Life Insurance?

Legacy life insurance isn't a product you'll find listed in a carrier's brochure. It's a strategy — the intentional use of a life insurance policy to create, protect, or transfer wealth to beneficiaries after death.

Two features make it work:

- A guaranteed death benefit: a predetermined, tax-advantaged payout to beneficiaries

- Cash value accumulation (in permanent policies): a living financial resource the policyholder can access during their lifetime

- Probate bypass: proceeds pass directly to named beneficiaries, outside the estate settlement process

Legacy Planning vs. Income Replacement

Standard life insurance often focuses on replacing a breadwinner's income for a defined period — bridging the gap until children are grown or a mortgage is paid off. Legacy life insurance works differently. The goal is to build something for the next generation, or to ensure that what was built doesn't get dismantled.

A $500,000 death benefit might fund a grandchild's college education, give a child the down payment on their first home, or provide the liquidity a family needs to preserve assets rather than selling them under pressure.

The Estate Planning Connection

Those financial outcomes hinge partly on how efficiently assets transfer. Life insurance with a named beneficiary generally avoids probate, meaning proceeds pass directly to heirs without the delays and legal costs of estate settlement. The Illinois State Bar Association's estate planning guide notes that property payable to a designated beneficiary falls outside the assets controlled by a will.

That speed and directness is what makes legacy life insurance a practical complement to wills and trusts — it fills gaps that legal documents alone can't close.

Types of Legacy Life Insurance Policies

The right policy type depends on your timeline, budget, and what you're trying to accomplish. Here's how each option fits into legacy planning.

Whole Life Insurance

Whole life is the most common vehicle for legacy planning. It provides:

- Lifelong coverage that doesn't expire, provided premiums are paid

- Guaranteed cash value growth you can borrow against or withdraw over time

- A fixed death benefit — a predetermined, predictable payout to beneficiaries

The cash value component gives policyholders a living financial resource — useful for retirement income, medical costs, or emergencies. Carriers like Mutual of Omaha, Foresters Financial, and Kansas City Life — all part of Vellum Life Group's carrier network — offer whole life products designed with long-term planning in mind.

Universal Life Insurance

If whole life feels too rigid, universal life adds flexibility without sacrificing permanence. Policyholders can adjust premium payments and death benefit amounts as circumstances change — useful when income fluctuates or family needs shift over time.

Indexed universal life (IUL) variants tie cash value growth to a market index, offering higher growth potential with some downside protection. These products carry real complexity — specifically around cap rates, participation rates, and cost-of-insurance charges — so it's worth pressure-testing the illustrations with an advisor before committing.

Term Life Insurance

Term doesn't build cash value and coverage expires — so it's not ideal for permanent wealth transfer. It still serves a real legacy function for younger families: a 20- or 30-year term policy taken out during peak earning years ensures dependents are protected if the worst happens before permanent coverage is in place.

Term is the most affordable starting point. A healthy 30-year-old can typically secure $500,000 in coverage for under $30 per month.

Final Expense Insurance

Final expense is a smaller-face-value permanent policy — typically $5,000 to $25,000 — designed to cover funeral costs, outstanding medical bills, and similar end-of-life expenses. The NFDA reports the national median funeral cost at $8,300 for a service with viewing and burial (2023 data).

For seniors or those on fixed incomes, final expense insurance is a practical, accessible option. The goal is straightforward: make sure family members have the funds to handle end-of-life costs without scrambling at the worst possible time.

Key Benefits of Legacy Life Insurance

Guaranteed, Tax-Efficient Wealth Transfer

Unlike stocks, real estate, or other illiquid assets whose value can drop or become difficult to access, a life insurance death benefit pays a fixed amount — regardless of market conditions.

That payout is also tax-advantaged. Under IRC Section 101(a)(1), death benefit proceeds are generally excluded from the beneficiary's gross income.

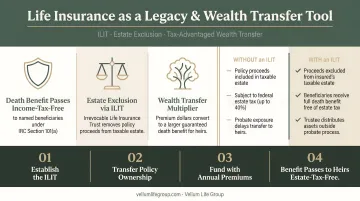

For families with larger estates, the structuring choices matter:

- Death benefits paid directly to a named beneficiary avoid probate and pass income-tax-free

- Placing the policy inside an irrevocable life insurance trust (ILIT) may also remove proceeds from the taxable estate

- ILIT transfers require careful legal coordination — policies transferred within three years of death carry a three-year inclusion risk

For context: the federal estate tax basic exclusion is $13.99 million in 2025, rising to $15 million in 2026 — so estate tax exposure is primarily relevant for larger estates.

Cash Value as a Living Asset

Whole and universal life policies accumulate cash value that the policyholder can access through loans or withdrawals while still alive. This flexibility provides a reserve for:

- Retirement income supplementation

- Medical or long-term care costs

- Business needs or opportunities

One important caveat: the tax treatment of policy loans and withdrawals depends on whether the policy is classified as a Modified Endowment Contract (MEC) and whether the policy remains in force. A lapsed or surrendered policy can trigger taxable income. Always review these specifics with a licensed advisor before accessing cash value.

Protection Against Estate Liquidation

More than 1 in 3 Americans took on debt after a loved one's death, according to a Debt.com consumer survey. Without adequate coverage, surviving family members often face a difficult choice: liquidate assets — a home, investment account, or inherited property — to cover final expenses and debts, or take on financial strain at an already difficult time.

A well-structured legacy policy keeps those decisions off the table when they matter most.

Who Should Consider Legacy Life Insurance?

Legacy life insurance fits a wide range of people — but a few situations make it particularly worth prioritizing.

Families with dependents: Parents and grandparents who want to guarantee a financial foundation for the next generation — regardless of what happens to other assets during their lifetime.

Individuals with estate succession needs: Life insurance can solve several inheritance challenges at once:

- Providing heirs with a cash equivalent when property or assets pass to only one heir

- Ensuring liquidity is available so inherited assets can be preserved rather than sold

Individuals with complex or illiquid estates: Real estate, farmland, and concentrated stock positions are hard to divide or sell quickly. Life insurance provides heirs with immediate liquidity to pay estate taxes or equalize inheritances — without forcing a rushed sale.

Anyone wanting to cover final expenses: Even a modest final expense policy prevents surviving family members from absorbing burial costs out of pocket during an already difficult time.

How Medical Conditions Affect Eligibility

Health history shapes how carriers evaluate applications, but it rarely closes the door entirely.

The Underwriting Process

Most life insurance applications involve health questions and, for fully underwritten policies, a medical exam. Insurers assess factors like age, diagnosis type, treatment history, current control, and complications. The outcome falls into one of three categories:

- Standard or preferred rates — competitive pricing for applicants who meet carrier health benchmarks

- Rated — coverage approved at higher premiums because the applicant's profile carries measurable added risk

- Declined or postponed — uncommon, but typically applies to recent diagnoses, active treatment, or severe uncontrolled conditions

Common conditions like type 2 diabetes, high blood pressure, and well-managed cancer history often result in rated approval rather than outright decline. The outcome depends heavily on specifics: how long ago a diagnosis occurred, whether the condition is controlled, and which carrier is reviewing the application.

When Standard Underwriting Isn't the Right Fit

Two alternatives exist for applicants with significant health histories:

| Policy Type | What's Required | Typical Benefit Range |

|---|---|---|

| Simplified Issue | Health questions, no exam | Varies by carrier |

| Guaranteed Issue | No questions, no exam | $2,000–$25,000 |

Guaranteed issue policies come with graded benefits — meaning the full death benefit typically isn't available if death occurs in the first two years of the policy. They also carry higher premiums for the coverage provided. But for applicants who can't qualify through standard underwriting, they ensure coverage remains accessible.

Carrier criteria vary substantially. A condition that results in a decline from one insurer may qualify for standard rates at another. An independent advisor who shops across multiple carriers — Vellum Life Group works with 10+ A-rated carriers — can match a complex health profile to the right fit rather than forcing it through a single underwriting lens.

How to Choose the Right Legacy Life Insurance Policy

Start With Your "Why"

The right policy depends entirely on what you're trying to accomplish:

- Covering final expenses only → Final expense whole life

- Protecting young dependents during earning years → Term life

- Building a guaranteed inheritance → Whole life

- Flexible long-term coverage that adapts → Universal life

- Business succession or estate equalization → Permanent life, often combined with legal structuring

The coverage amount follows from the goal. A policy designed to cover an $8,300 funeral looks very different from one designed to fund a trust or equalize an inheritance.

Compare Multiple Carriers Before Deciding

Premiums, underwriting standards, and cash value performance vary significantly from carrier to carrier. A policy that's declined or priced high by one insurer may be approved at competitive rates by another, particularly for applicants with health histories. Working with an independent advisor who has access to a broad carrier network makes real comparison possible.

Vellum Life Group works with 15+ A-rated carriers — including Mutual of Omaha, Foresters Financial, Transamerica, and Corebridge Financial — to find options matched to each client's situation and health profile. Many policies are approved the same day or within a few days; fully underwritten policies requiring a medical exam typically take two to four weeks.

Build in Long-Term Flexibility

A legacy policy that lapses because premiums become unaffordable defeats its purpose. Before committing, confirm the coverage is sustainable — then plan to revisit it over time. Life changes fast. Annual check-ins help ensure your policy stays aligned as circumstances shift:

- Confirm premiums remain affordable as income or expenses change

- Update beneficiary designations after major life events

- Adjust coverage amounts following marriages, new children, or significant changes in assets or obligations

- Revisit policy type if long-term goals evolve

Frequently Asked Questions

What is a legacy life insurance policy?

Legacy life insurance is a purpose-driven approach, not a specific product. It refers to using a life insurance policy — most commonly permanent whole or universal life — to intentionally create or transfer wealth to beneficiaries, cover estate costs, or support charitable causes after the policyholder's death.

How do medical conditions affect eligibility?

Medical conditions may result in higher premiums or limit available policy types, but they rarely mean complete ineligibility. Simplified issue and guaranteed issue options exist for applicants with significant health histories, and outcomes vary by carrier. Comparing multiple insurers is almost always worth the effort.

How is legacy life insurance different from traditional life insurance?

The difference is intent. Traditional life insurance often focuses on replacing income for a defined period. Legacy life insurance targets permanent wealth transfer and typically involves whole or universal life policies with lifelong coverage and no expiration date.

Who should consider legacy life insurance?

Strong candidates include:

- Parents who want to guarantee an inheritance

- Individuals with succession or estate transfer planning needs

- Individuals with illiquid estates or estate tax exposure

- Anyone who wants to cover final expenses without burdening surviving family

Is a medical exam required?

It depends on the policy. Fully underwritten policies require an exam and offer the best rates. Simplified issue policies require only health questions. Guaranteed issue policies require neither but come with lower face values, higher premiums, and graded benefit periods.

Can legacy life insurance help reduce estate taxes?

Potentially, yes — but proper legal structuring is required. Placing a policy inside an irrevocable life insurance trust (ILIT) may exclude proceeds from the taxable estate. This must be executed carefully with an estate attorney, as a three-year lookback period under IRC Section 2035 can trigger inclusion if not handled correctly.