Introduction

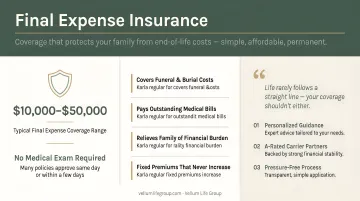

The 2023 national median cost of a funeral with viewing and burial was $8,300, according to the National Funeral Directors Association — and that figure doesn't include outstanding medical bills, legal fees, or the debts many families are left sorting through after a loss. It's no surprise that final expense insurance has become one of the fastest-growing segments in life insurance, with new annualized premium rising 16% to $1.05 billion in 2024 according to LIMRA.

For seniors researching how to cover these costs, Aflac is one of the most recognized names that comes up. A familiar brand name, however, isn't the same as the right fit for your health profile and budget.

This guide covers what Aflac final expense insurance actually covers, how premiums break down by age and gender, what separates the Level and Modified plans, and whether Aflac is the right fit compared to other carriers for your specific situation.

Key Takeaways

- Aflac offers whole life final expense coverage from $2,000–$50,000, for applicants ages 45–80, with no medical exam required

- Premiums lock in permanently at purchase; the earlier you apply, the lower your rate for life

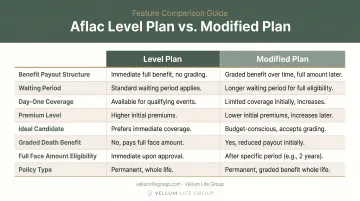

- Two plans available: Level (full Day 1 coverage up to $50,000) and Modified (2-year waiting period for non-accidental death, up to $25,000)

- Aflac is competitively priced, but comparing multiple carriers before committing can reveal better-fit options

What Is Aflac Final Expense Insurance?

Aflac Final Expense Whole Life is underwritten by Tier One Insurance Company, a subsidiary of Aflac Incorporated, and administered by Aetna Life Insurance Company. It is a permanent whole life policy — meaning the death benefit never decreases, premiums never increase, and cash value accumulates over time and can be accessed through policy loans.

Plan Structure and Eligibility

Aflac's final expense product uses simplified issue underwriting — no physical exam, just a few health questions. Applicants qualify under one of two health rating tiers:

- Preferred / Standard — Full death benefit payable from Day 1 for any cause of death

- Modified — Full benefit for accidental death immediately; non-accidental death benefit is limited during years 1–2, with full benefit beginning in year 3

Coverage amounts and issue ages vary by plan:

| Plan | Issue Ages | Coverage Range |

|---|---|---|

| Level | 45–80 | $5,000–$50,000 (age-banded maximum) |

| Modified | 45–75 | $2,000–$25,000 |

The Level plan's maximum benefit is age-banded: applicants ages 45–55 can access the full $50,000, while the maximum steps down at older age bands. The policy is available in all U.S. states except New York.

Key Policy Features

- Guaranteed level premiums for life

- Cash value accumulation with loan access once sufficient value builds

- Coverage never lapses as long as premiums are paid

Optional Riders (Level Plan Only)

Three riders are available exclusively on the Level plan:

- Accelerated Death Benefit Rider — Early access to the death benefit upon a terminal illness diagnosis

- Accidental Death Benefit Rider — Doubles the payout if death results from an accident

- Children's Term Insurance Rider — Adds term coverage for dependent children

None of these riders are available on the Modified plan.

How Much Does Aflac Final Expense Insurance Cost?

Premiums lock in at the age you apply and never change — which means every year you wait permanently raises your monthly cost.

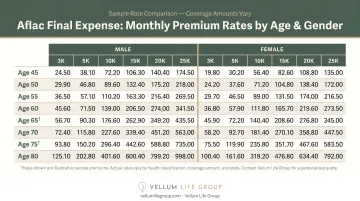

Sample Monthly Premium Rates

The table below shows estimated monthly premiums for non-tobacco Level plan applicants, sourced from Choice Mutual's licensed quote calculator (rates valid as of March 9, 2026; accessed June 2026). These are third-party estimates, not Aflac's official published rates.

| Age | Female $5k | Female $10k | Female $25k | Male $5k | Male $10k | Male $25k |

|---|---|---|---|---|---|---|

| 45 | $15 | $25 | $57 | $17 | $30 | $68 |

| 50 | $16 | $27 | $61 | $19 | $34 | $77 |

| 55 | $17 | $29 | $67 | $21 | $38 | $89 |

| 60 | $19 | $35 | $80 | $25 | $45 | $107 |

| 65 | $24 | $44 | $104 | $30 | $56 | $133 |

| 70 | $30 | $56 | $134 | $38 | $72 | $174 |

| 75 | $43 | $82 | $199 | $52 | $100 | $244 |

| 80 | $60 | $116 | $284 | $80 | $156 | $384 |

The age curve is steep: a 65-year-old male pays more than double what a 45-year-old male pays for the same $10,000 policy, and by age 80 that gap widens to roughly five times the cost.

Coverage Amount Context

- $5,000–$10,000: Covers basic funeral and cremation costs (NFDA median cremation: $6,280; burial: $8,300)

- $10,000–$25,000: Covers funeral costs plus outstanding medical bills or debts

- $25,000–$50,000: Provides additional financial cushion for beneficiaries beyond immediate expenses

How Aflac Compares to Competitors

Using the same $10,000 non-tobacco benchmark, here's how Aflac compares to Mutual of Omaha Living Promise and MoneyGeek's general market average:

| Profile | Aflac | Mutual of Omaha | Market Average |

|---|---|---|---|

| Female, 65 | $44 | $41 | $50 |

| Male, 65 | $56 | $54 | $66 |

| Female, 80 | $116 | $98 | $125 |

| Male, 80 | $156 | $135 | $164 |

Aflac tends to price below the general market average but slightly above Mutual of Omaha Living Promise at these age points. The right carrier, however, shifts based on your age, health history, and coverage amount — so running quotes across multiple carriers before committing is the most reliable way to find your best rate.

Key Factors That Affect Your Aflac Final Expense Premiums

Age

Age is the single largest cost driver. To illustrate: a 75-year-old male applying for $10,000 in coverage pays $100/month versus $30/month for the same coverage at 45 — that's $840 more per year for identical protection. MoneyGeek's 2026 final expense study found premiums jump an average of 45% for men and 44% for women between ages 75 and 80 alone.

Gender

Women pay less. According to CDC 2023 life tables, female life expectancy at birth is 81.1 years versus 75.8 years for males — a 5.3-year gap that insurers price directly into premiums. At age 65, a female applicant pays $44/month for $10,000 versus $56/month for a male applicant at the same coverage level.

Health Status and Plan Tier

Your answers to Aflac's health questions determine whether you receive Preferred/Standard or Modified placement. Better health means:

- Qualifies for full Day 1 coverage under the Level plan

- Unlocks access to optional riders

- Avoids the higher premiums tied to Modified placement

- Faces no waiting period before the policy pays out in full

Recent or serious health conditions may push an applicant to Modified — or make a different carrier with more lenient underwriting on specific conditions the smarter choice.

Coverage Amount

The relationship is direct: a $25,000 policy costs roughly 4–5x more per month than a $5,000 policy. Before automatically choosing the highest available amount, calculate what your family actually needs covered — funeral costs, outstanding debts, and final medical bills — and match coverage to that number.

Tobacco Use

Aflac classifies tobacco use within the prior 12 months as higher risk. MoneyGeek's data shows a 50-year-old female smoker pays approximately 27% more than a non-tobacco user for comparable final expense coverage. If you've quit recently, you may qualify for non-tobacco rates — confirm this with an advisor when you apply.

Aflac Level Plan vs. Modified Plan: What's the Difference?

| Feature | Level Plan | Modified Plan |

|---|---|---|

| Issue ages | 45–80 | 45–75 |

| Coverage range | $5,000–$50,000 | $2,000–$25,000 |

| Natural death — Year 1–2 | Full benefit | Limited (return of premiums + interest) |

| Natural death — Year 3+ | Full benefit | Full benefit |

| Accidental death | Full benefit immediately | Full benefit immediately |

| Optional riders | Yes (3 available) | No |

The Modified plan exists as a fallback for applicants whose health history disqualifies them from the Level plan. It's better than no coverage, but the two-year limitation on non-accidental death is a real financial risk, particularly for older applicants.

If you can qualify for the Level plan, it is nearly always the better value — more coverage, lower cost per dollar of benefit, and rider availability all favor it. If your health history limits you to the Modified plan, check whether another carrier's underwriting would qualify you for immediate full coverage before accepting those terms.

Is Aflac Final Expense Insurance Right for You?

Strong Fit Profiles

Aflac tends to work well for you if you:

- Are ages 45–80 seeking $5,000–$50,000 in permanent whole life coverage

- Want a nationally recognized carrier with an A+ AM Best financial strength rating (affirmed August 2024 for Aflac entities)

- Prefer no medical exam

- Can qualify for Preferred or Standard placement — including those with manageable conditions like well-controlled diabetes, COPD, or cancer in remission

When to Look Elsewhere

Aflac may not be the best option if:

- You need guaranteed issue coverage with no health questions at all

- A specific health condition is underwritten more favorably by another carrier

- You are primarily cost-driven — a competing carrier may offer a lower rate for your exact profile

- You need coverage in New York (Tier One is not licensed there)

Common Mistakes That Increase Your Effective Cost

- Delaying your application locks in a permanently higher rate — every year counts

- Accepting Modified without shopping around; other carriers may offer immediate full coverage for a similar health profile

- Underestimating inflation: NFDA data shows funeral costs rose roughly 15.6% from 2014 to 2023, meaning $10,000 today may fall short in 15 years

- Overlooking the waiting period risk — a Modified plan pays far less than face value if death from natural causes occurs in year one

Comparing Aflac side-by-side with other A-rated carriers is the most reliable way to confirm you're getting the right plan at the right price. Eva Ikonomakos at Vellum Life Group works with 15+ carriers — including Aflac, Mutual of Omaha, and American Amicable — and offers a free, no-pressure consultation with a 24-hour response commitment for clients nationwide.

Conclusion

Aflac final expense insurance is a legitimate, well-rated whole life option with no medical exam, coverage from $2,000–$50,000, and premiums locked in for life. For applicants who qualify for the Level plan, it delivers Day 1 full coverage with optional riders that the Modified plan can't match.

The right policy, though, depends on your age, health profile, and budget — not brand recognition. Final expense premiums increase with age, and the gap between a Level and Modified plan outcome in year one can be significant. An independent advisor with access to multiple carriers can match you to the most favorable underwriting for your specific situation, often finding better rates or Day 1 coverage where a single-carrier search falls short. The sooner you compare, the more options you have.

Frequently Asked Questions

Does Aflac offer final expense insurance?

Yes. Aflac offers a Final Expense Whole Life policy underwritten by Tier One Insurance Company, an Aflac subsidiary, available in all U.S. states except New York. Applicants ages 45–80 can apply without a medical exam using simplified issue underwriting.

Does Aflac offer a $50,000 final expense benefit?

Yes, but only through the Level plan for eligible applicants ages 45–80. The maximum steps down at older age bands, and the Modified plan is capped at $25,000 for ages 45–75. The $50,000 maximum requires qualifying for Level plan coverage.

Does Aflac final expense insurance cover kidney stones?

Aflac final expense is a life insurance policy, not health insurance. It does not pay for medical treatments or procedures. The tax-free death benefit goes to your named beneficiary, who can use those funds however they choose.

Can the Aflac final expense death benefit be used for anything?

Yes. The death benefit is paid as a tax-free lump sum to the named beneficiary with no restrictions on use. Beneficiaries can apply the funds to funeral costs, medical bills, legal fees, debts, or everyday living expenses.

Is there a waiting period with Aflac final expense insurance?

Applicants who qualify for the Preferred or Standard rating have no waiting period — full benefits apply from Day 1. The Modified plan includes a 2-year waiting period for non-accidental causes of death, after which the full benefit becomes payable.

Does Aflac final expense insurance require a medical exam?

No medical exam is required. Aflac uses simplified issue underwriting based on health questions and an electronic review of medical history, with most applicants receiving a decision and coverage typically becoming active within 3–5 business days.