Introduction

Most families insure their cars, their homes, even their phones — yet when it comes to life insurance for a spouse or child, the conversation often gets pushed to "someday." That someday can carry a serious cost.

Consider a dual-income household with two kids and a mortgage. If one partner dies without adequate coverage, the surviving spouse doesn't just lose emotional support — they lose income, potentially the home, and the financial stability their children depend on.

According to LIMRA's 2025 data, 47% of adults would struggle to pay living expenses within six months of a primary wage earner's death. That's not a fringe scenario — that's nearly half of American families.

This guide covers the key life insurance options for spouses and children, when each makes sense, and how to build a plan that actually fits your family — not a generic checklist.

Key Takeaways

- Term life insurance is typically the most affordable and practical choice for most spouses during peak earning and child-rearing years

- Stay-at-home spouses need coverage too; replacing their contributions can cost families over $162,000 annually

- Families can choose individual policies, joint life insurance, or spouse/child riders, each with distinct trade-offs

- The earlier you lock in coverage, the lower the premiums — for both spouses and children

Why Life Insurance Matters for Both Spouses

Life insurance for a spouse isn't just about replacing a paycheck. It's about keeping the mortgage paid, the children's routines intact, and giving the surviving partner breathing room during an already devastating time — not a financial crisis on top of grief.

The coverage need is real regardless of coverage status. Both earning and non-earning spouses carry financial weight that disappears when they're gone.

The Hidden Financial Value of a Stay-at-Home Parent

Stay-at-home spouses don't draw a salary, but the work they do has a measurable price tag. According to Salary.com's updated 2026 valuation, the estimated annual replacement value for a stay-at-home mother's contributions — childcare, household management, transportation, and more — is $162,581.

Investopedia's own analysis puts that figure even higher, at over $204,000 annually, when accounting for the full range of tasks including cooking, cleaning, and grocery management.

If that spouse passes away, the surviving partner faces immediate, concrete costs:

- Full-time childcare or after-school care

- Household cleaning and management services

- Meal preparation or dining costs

- Transportation and scheduling that one parent now handles alone

Without life insurance, the surviving spouse covers these costs out of pocket — often while also dealing with grief and trying to maintain their career.

Dual-Income Households: Why Both Partners Need Coverage

In 2025, both spouses were earning in 66.3% of married-couple families with children under 18, according to Bureau of Labor Statistics data. In most of those households, both incomes are load-bearing — meaning the loss of one doesn't just hurt, it restructures the entire financial plan.

Mortgage payments, childcare costs, retirement contributions, and college savings all become harder or outright impossible on a single income. Both partners should carry coverage that reflects what they actually contribute— full stop.

That urgency is highest when households have the least margin for disruption:

- Families with young children (under 10)

- Households with a mortgage or significant debt

- Single-breadwinner families

- Any household where one spouse would need to reduce work hours to manage childcare alone

Life Insurance Options for Your Spouse

There are three main ways to insure a spouse: individual policies for each partner, a joint life insurance policy covering both, or a spouse rider added to an existing policy. Some families combine approaches.

Individual Term or Permanent Policies for Each Spouse

With individual policies, each spouse is insured separately under their own contract. Each names the other — or children, or a trust — as beneficiary.

Why individual policies work well:

- Coverage continues for the surviving spouse after a claim is paid

- Each policy can be sized independently (different amounts, different terms)

- Term life is the most affordable option for families in active earning years

- Policies aren't tied to each other — one lapsing doesn't affect the other

For most families, two separate term policies are the clearest, most flexible starting point.

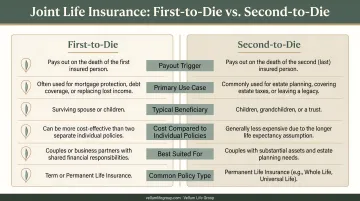

Joint Life Insurance: First-to-Die vs. Second-to-Die

Joint policies cover two people under a single contract, but they work very differently depending on the type.

| Type | When It Pays | Best Used For |

|---|---|---|

| First-to-Die | After the first spouse passes | Replacing lost income, covering shared debts with young dependents |

| Second-to-Die (Survivorship) | After both spouses have passed | Estate planning, funding a special needs trust, leaving a legacy |

The distinction matters more than it might seem at first glance.

With a first-to-die policy, the surviving spouse receives the death benefit — useful for replacing income or covering shared debts. But once the benefit pays out, that coverage is gone. Policygenius notes these policies are relatively rare, partly because two individual policies are often easier to manage and more flexible long-term.

Second-to-die policies serve a different purpose entirely. They don't help a surviving spouse cover bills or replace income — they're designed for what comes after both partners are gone. They're commonly used to fund special needs trusts or support legacy planning in larger estates.

If you're still raising children or carrying a mortgage, the income-replacement gap left by a first death is what needs covering most — and individual term policies tend to address that more directly than either joint structure.

Life Insurance for Children: What You Need to Know

Most financial professionals agree: children rarely need life insurance. Children don't provide income a family depends on, so traditional income-replacement logic doesn't apply.

That said, a few specific situations justify coverage:

- Covering funeral and final expenses (which can run $7,000–$12,000+)

- Giving a grieving parent time off work without financial pressure

- Locking in a child's insurability before any health conditions develop

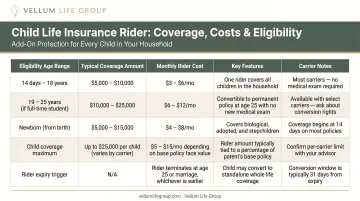

Child Life Insurance Riders (The Most Common Approach)

A child rider is an add-on to a parent's existing term or permanent policy. Rather than a separate policy, it covers all eligible children under one flat fee.

How child riders typically work:

- Coverage range: $5,000 to $25,000 per child

- Cost benchmark: approximately $5/month per $10,000 of coverage (per NerdWallet; actual premiums vary by insurer and age)

- Eligibility: children from 15 days old up to age 18, with coverage often continuing until age 25 or the parent reaches age 65

- One rider typically covers all current and future eligible children

The conversion privilege gives a child the option to convert their coverage to a permanent individual policy as an adult — with no medical exam required. If a child later develops a health condition like diabetes or a heart issue, this feature can be financially significant. Transamerica, for example, allows conversion up to five times the rider death benefit or $50,000, whichever is less. Conversion privileges aren't universal, so confirm this feature before buying a rider.

Standalone Whole Life Policies for Children

Standalone children's whole life policies offer permanent coverage with premiums locked in at the child's current age. Mutual of Omaha, for example, offers children's whole life policies from 14 days to age 17, with coverage amounts from $5,000 to $50,000.

NerdWallet reports an average annual premium of roughly $166 for a $25,000 policy on a newborn — though actual costs vary by insurer and underwriting.

Who might consider standalone whole life:

- Parents who want to guarantee future insurability regardless of health changes

- Those interested in the cash value component as a supplemental long-term savings vehicle

Whole life cash value typically grows at 1%–4% annually — slow compared to other options. The same premium dollars invested in a 529 education account or index fund may generate better long-term returns for a child's future. Whether that trade-off makes sense depends on the family's goals, so it's worth running the numbers before committing.

Spouse and Child Riders: A Closer Look

Riders are optional add-ons that extend coverage to a specific person without requiring a separate standalone policy. They're typically cheaper than a second policy, but they come with limitations.

Spouse term riders add a defined death benefit for a spouse onto the policyholder's existing policy. The rider usually expires when the base policy ends or when the spouse reaches a certain age.

There's an important catch: if the policyholder dies first, the surviving spouse collects the death benefit — but then has no remaining life insurance coverage of their own. At that point, they'd need to qualify for a new policy, potentially at an older age or with health changes that make coverage more expensive or harder to obtain.

Knowing the limitation helps clarify when a rider is the right call — and when it isn't.

When riders make sense:

- As a low-cost starting point while a family builds toward full individual coverage

- When budget is limited and the rider provides meaningful near-term protection

- For child coverage where the conversion privilege is included

When a standalone policy is smarter:

- When the rider's coverage limit falls well short of what the spouse actually needs

- When long-term, independent coverage is the priority

- When both spouses want coverage that isn't contingent on the other's policy staying active

Before adding a rider, compare its coverage limit against actual income replacement needs. A $100,000 spouse rider on a policy where the spouse's true need is $400,000 leaves a gap that matters when it counts.

How Much Life Insurance Does Your Family Need?

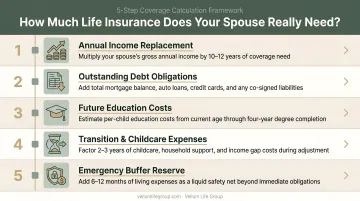

The most common starting point is 10–15 times annual income, per Life Happens. Some versions of this rule add $100,000 per child for college expenses. These are useful anchors, not final answers.

A more complete framework for spouse coverage:

- Income replacement: Multiply years until retirement by annual income

- Mortgage payoff: Cover the current outstanding balance

- Childcare and household costs: Factor in full replacement value, especially for stay-at-home spouses

- Outstanding debts: Include auto loans, student loans, and credit cards

- Emergency buffer: Set aside 6–12 months of living expenses

For children, the math is simpler: enough to cover final expenses and give the family 3–6 months to stabilize — typically $15,000 to $25,000.

Life events that should trigger a coverage review:

- Marriage or divorce

- Birth or adoption of a child

- A new mortgage or significant debt

- A major income change (promotion, job loss, a spouse returning to work)

At Vellum Life Group, Eva Ikonomakos works with families through all of these transitions — comparing options across multiple A-rated carriers and adjusting recommendations as life changes. Consultations are free and grounded in your family's actual numbers.

Frequently Asked Questions

What is spouse and child life insurance?

Spouse and child life insurance refers to policies or riders that pay a death benefit if a covered spouse or child passes away. These policies fit into a broader family coverage plan, protecting the entire household financially — not just the primary earner.

Do stay-at-home spouses need life insurance?

Yes. A stay-at-home spouse's contributions — childcare, household management, transportation — carry a real economic replacement cost, estimated above $162,000 annually. Their death creates immediate, concrete financial demands the surviving partner must cover.

Should I buy a separate policy for my spouse or add a rider to mine?

A rider is cheaper and simpler, but the surviving spouse loses coverage once the base policy pays out. A separate individual policy is more flexible and provides lasting, independent protection. For most families, it's the stronger long-term choice.

Is life insurance for children worth it?

Children rarely need coverage for income replacement. But a child rider or standalone policy can make sense to cover final expenses, cover income loss while a parent takes time off to grieve, or lock in a child's future insurability before any health conditions develop.

How much life insurance does a spouse need?

Start with 10–15 times annual income, then adjust for mortgage balance, childcare costs, outstanding debts, and long-term goals. For stay-at-home spouses, base the calculation on actual replacement cost of their contributions, not a zero-income figure.

Can unmarried couples get life insurance for each other?

Yes — unmarried couples can generally purchase life insurance on each other by demonstrating insurable interest, such as a shared mortgage, jointly owned assets, or documented financial dependence. Requirements vary by insurer and state.