Getting it wrong in either direction has real consequences. Too little, and the death benefit runs out before the mortgage is paid off or the kids finish school. Too much, and families overpay for coverage they don't need, diverting money from other financial priorities.

The right number isn't universal — it depends on your income, debts, dependents, existing assets, and what you're trying to protect. This guide walks through exactly how to find yours: the five factors that drive coverage needs, three proven calculation methods, life-stage guidance, and the most common mistakes to avoid.

Key Takeaways

- Most financial experts recommend 10–12 times your annual income as a starting baseline for term life coverage

- Your actual number depends on income, outstanding debts, dependents, future goals, and existing savings

- Three calculation methods (Income Multiple, DIME, and Human Life Value) offer progressively more detailed estimates

- Coverage needs peak during high-obligation years and should be reviewed after every major life event

- An independent advisor who shops multiple carriers finds the right coverage at the most competitive rate

What Factors Determine How Much Term Life Insurance You Need

Before running any numbers, it helps to understand the five financial categories that directly shape your coverage needs. Overlook even one, and your family could end up underprotected.

Income Replacement

This is the foundation of any coverage calculation. The goal is to replace the income your family would lose — enough to maintain their standard of living, cover ongoing expenses, and continue working toward financial goals without your salary.

Don't anchor to today's paycheck alone. A complete income replacement estimate accounts for:

- Current annual income and expected career growth

- Inflation's effect on purchasing power over the policy term

- Years remaining until your youngest dependent reaches financial independence

- Any second income your spouse contributes (and whether that could cover household needs alone)

Outstanding Debts

All outstanding debts should be covered so surviving family members aren't forced to liquidate assets or shoulder financial hardship alone. That includes:

- Mortgage balance (typically the largest single debt factor)

- Car loans

- Student loans

- Credit card balances

According to Experian's 2024 data, the average mortgage debt in the US sits at $252,505 — a number that deserves serious attention when sizing a policy.

Dependents and Their Future Needs

The number, age, and circumstances of your dependents directly scale how much coverage makes sense. Younger children with more years of support ahead require a larger benefit. Consider:

- Children who need years of childcare and living expenses

- A non-working or lower-earning spouse

- Aging parents who rely on your financial support

College costs also belong in this calculation. The College Board's 2025–26 data shows annual costs (tuition, fees, housing, and food) running $25,850 at public in-state schools, $45,780 out-of-state, and $60,920 at private nonprofits. For two children attending four-year public schools, that's roughly $207,000 — before accounting for tuition inflation.

Existing Assets and Savings

Savings, retirement accounts, and any existing life insurance policies offset your coverage needs. The goal is to fill the gap between what your family would need and what they already have.

Future Financial Goals

A death benefit can also protect longer-range goals: funding a spouse's retirement, leaving an inheritance, or covering final expenses. The NFDA reports the median funeral with viewing and burial costs $8,300 — a modest but real number to build into your calculation.

Three Methods to Calculate Your Term Life Insurance Amount

No single formula works for every situation. These three methods offer progressively more detailed estimates — start simple and refine from there.

The Income Multiple Rule (10–12x)

The quickest starting point: multiply your annual gross income by 10 to 12. Sources like Ramsey Solutions and Baird both endorse this range, though some institutions (U.S. Bank, NerdWallet) cite 8–10x as their baseline.

It's a useful first estimate, not a final number. It doesn't account for debts, specific dependents, or existing assets.

For families with children, NerdWallet and Northwestern Mutual both recommend layering on $100,000 per child for education costs on top of the income multiple. Guardian suggests $100,000–$150,000 per child depending on your college cost assumptions.

Quick example: A household earning $90,000 annually with two children would calculate: ($90,000 × 10) + ($100,000 × 2) = $1,100,000 as a baseline.

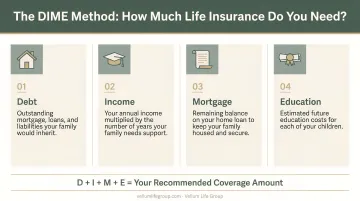

The DIME Method

DIME produces a more personalized estimate by accounting for specific financial obligations:

| Letter | What It Covers |

|---|---|

| D | All non-mortgage debts + final expenses |

| I | Annual salary × years until youngest child finishes high school |

| M | Current mortgage payoff balance |

| E | Projected college costs per child |

Example: A 35-year-old earning $85,000 with a $240,000 mortgage, $30,000 in other debts, two children (youngest age 5), and college costs of $100,000 per child:

- D: $30,000 + $8,300 = $38,300

- I: $85,000 × 13 years = $1,105,000

- M: $240,000

- E: $200,000

- Total: ~$1,583,300

That's meaningfully higher than the basic income multiple — and more accurately reflects this family's actual financial picture.

The Human Life Value (HLV) Approach

HLV estimates the present value of your future earning potential. Financial advisors often prefer it because it builds in a buffer for inflation and income growth over a career.

Guardian publishes these age-based HLV multiples:

| Age Range | Recommended Multiple |

|---|---|

| 18–40 | 30x income |

| 41–50 | 20x income |

| 51–60 | 15x income |

| 61–65 | 10x income |

A 35-year-old earning $90,000 would target $2,700,000 under HLV. That's substantially more than the basic income multiple produces, which is why advisors turn to this method when families want a comprehensive buffer rather than a minimum floor.

Run your numbers through at least two of these methods. If the results diverge by $500,000 or more, that gap usually signals an unaccounted variable — a debt, a dependent, or an income trajectory worth discussing with a licensed advisor before settling on a coverage amount.

How Much Term Life Insurance Do You Need at Different Life Stages

Coverage needs aren't static. They peak during your highest-earning, highest-obligation years, then gradually decrease as debts are paid off and dependents become independent.

Young Singles and Early-Career Adults (20s–Early 30s)

Coverage needs are often lower at this stage — fewer dependents, less debt. But this is the best time to lock in low rates.

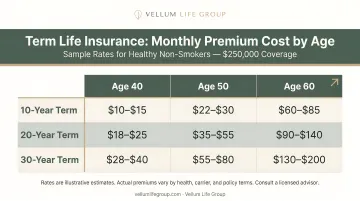

Even a modest policy serves two purposes: covering student loans so parents aren't left with the balance, and establishing insurability before health issues make coverage harder to get. A $500,000, 20-year term policy averages just $29/month for a 30-year-old male according to 2024 Policygenius data — a low cost for real protection.

Growing Families with Young Children (30s–40s)

This is typically when coverage needs are highest. Mortgage, young dependents, rising income, and education costs all converge at the same time.

The DIME and HLV methods covered earlier are most valuable at this stage. The difference between a rough estimate and a precise calculation can be hundreds of thousands of dollars in coverage — and the monthly premium gap between $750,000 and $1.2 million is often smaller than most people realize.

Mid-Career Homeowners Approaching Retirement (50s)

As debts decrease and children become financially independent, coverage needs often decline. But a policy still makes sense to protect a spouse's retirement income and cover any remaining obligations.

One thing to watch: premiums rise sharply in this decade. A $500,000, 20-year term policy that costs a 40-year-old male $42.94/month jumps to $102.50/month at 50 and $268.04/month at 60 (Policygenius 2024 data). Reassessing coverage at this point — rather than auto-renewing or dropping it entirely — often means right-sizing your policy and keeping premiums manageable into retirement.

Estate and Succession Planning Needs at Any Stage

Individuals with significant assets or financial obligations may carry additional coverage needs beyond personal protection:

- Estate equalization — ensuring heirs receive comparable value when assets cannot be evenly divided

- Legacy transfer funding — providing heirs with immediate liquidity so assets can be preserved intact

- Personal loan guarantees — debt personally guaranteed by an individual doesn't disappear; it flows back to the estate

Each of these requires its own analysis, separate from standard personal coverage calculations. Eva Ikonomakos at Vellum Life Group works with clients across all of these scenarios.

Common Mistakes When Estimating Your Term Life Insurance Amount

Most coverage gaps aren't accidental — they come from a few predictable missteps. Here's what to watch for:

Applying the 10x shortcut without adjusting for your actual debts. Leaving out debt balances, childcare costs, education expenses, or inflation can produce a death benefit that falls short within a few years. According to LIMRA's 2024 Insurance Barometer Study, 22% of life insurance owners say their coverage is already insufficient — and these are people who already have a policy.

Not updating coverage after major life events. Marriage, divorce, a new child, or a home purchase all shift what your family needs financially. A policy written five years ago may not reflect today's picture. Annual reviews aren't optional — they're how coverage stays accurate as life changes.

Choosing a term length based on price, not obligations. A 10-year policy may look affordable today but leave your family unprotected when the mortgage still has 20 years left or the youngest child is still in middle school. Match the term to your longest financial commitment, not your shortest.

How Vellum Life Group Can Help You Find the Right Coverage

Vellum Life Group is a nationwide independent life insurance advisory firm founded by Eva Ikonomakos, who brings over 15 years of experience across financial services, healthcare, and international business. The firm has protected 500+ families and written $50M+ in coverage.

Because Vellum partners with 10+ A-rated carriers — including Mutual of Omaha, Corebridge Financial, Transamerica, and Ameritas — clients aren't locked into one insurer's pricing or products. Eva compares options across the market to match each family or individual with coverage that fits their situation and budget.

Vellum's process is straightforward:

- Book a free consultation — Discuss your goals, family situation, and coverage needs with no obligation

- Review your options — Quotes compared across multiple carriers, presented side by side without jargon

- Apply with guidance — Simple application process; many policies approved the same day, medical exam policies take 2–4 weeks

- Stay covered long-term — Annual check-ins included at no extra cost, so your policy keeps pace as your life changes

To get started, book a free 30-minute consultation at calendly.com/eva-ikonomakos/30min, call 917-363-3554, or email info@vellumlifegroup.com.

Frequently Asked Questions

Frequently Asked Questions

What is the recommended amount of term life insurance?

Most experts recommend 10–12 times your annual income as a starting point. More precise figures come from the DIME method or Human Life Value approach, which account for your debts, dependents, existing assets, and financial goals to produce a number specific to your situation.

How long should my term life insurance policy last?

Match the term length to your longest financial obligation — typically 15–30 years for families with a mortgage and young children. Coverage should remain in place until dependents are financially independent and major debts are paid off.

Does a stay-at-home parent need term life insurance?

Yes. A stay-at-home parent's contribution carries real economic value — childcare and household management alone carry a significant price tag. Salary.com estimates the annual replacement cost at over $162,000, making coverage just as necessary as for an income earner.

What happens if I outlive my term life insurance policy?

The policy expires with no death benefit paid. Ideally, your debts are paid and your savings are sufficient that coverage is no longer needed — you're effectively self-insured. Some policies offer a conversion option to permanent coverage before the term ends.

How does my health affect how much term life insurance I can get?

Insurers use medical underwriting to assess your health — better health generally means lower premiums and higher coverage limits. Serious conditions may affect eligibility or raise costs. Working with an independent advisor helps identify which carriers offer the most favorable terms for your profile.

Should I buy one large policy or multiple smaller ones?

Laddering — purchasing multiple term policies with different lengths — can be a smart strategy. For example, combining a 30-year and a 20-year policy provides higher coverage during high-obligation years while reducing premiums as debts decrease and children become independent.