Most families have no dedicated plan for this. Final expense insurance exists to change that.

This guide covers what final expense insurance actually is, what it costs in Kentucky, who qualifies, and how to choose a policy that fits your budget and health profile.

Key Takeaways

- Final expense insurance is a small whole life policy ($2,000–$50,000) designed to cover funeral, burial, and related end-of-life costs

- No medical exam required — many Kentucky residents get approved same-day or within a few days

- Premiums are fixed for life based on your age, gender, tobacco use, and health at application

- Kentucky law gives buyers a 30-day right to return replacement policies for a full refund

- An independent advisor like Vellum Life Group shops 15+ carriers to match your health profile with the most competitive rate available

What Is Final Expense Insurance?

Final expense insurance — also called burial insurance or funeral insurance — is a type of permanent whole life policy with a smaller death benefit. It's designed specifically to relieve family members of end-of-life financial burdens, not to replace income or fund retirement.

It is not the same as a prepaid funeral plan. A prepaid plan is a contract with one specific funeral home for specific services at today's prices. Final expense insurance pays a tax-free lump sum directly to your named beneficiary, who can use it for any expense — funeral costs, medical bills, credit card debt, or anything else. Your family keeps control of the money.

How It Works

The mechanics are straightforward:

- You pay a fixed monthly premium for life

- When you die, the death benefit is paid directly to your beneficiary

- Your beneficiary can spend it however they choose — no restrictions, no funeral home involvement required

- Coverage never expires as long as premiums are paid

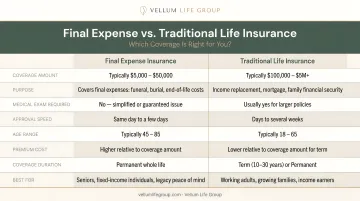

How It Differs from Traditional Life Insurance

| Feature | Final Expense | Traditional Life Insurance |

|---|---|---|

| Coverage amount | $2,000–$50,000 | $100,000–$1M+ |

| Medical exam | Not required | Usually required |

| Application | Short health questions | Full underwriting |

| Primary purpose | End-of-life costs | Income replacement |

| Typical applicants | Ages 45–85 | Ages 18–65 |

That combination — no medical exam, simplified questions, and coverage up to age 85 — is why final expense policies are often the most practical option for older adults who no longer qualify for traditional life insurance.

How Much Does Final Expense Insurance Cost in Kentucky?

Four factors determine your premium:

- Age at application — the single biggest driver; the younger you apply, the lower your rate

- Biological sex — women typically pay less than men at every age

- Tobacco use — tobacco users pay higher premiums than non-tobacco applicants

- Coverage amount — higher face amounts mean higher monthly premiums

Sample Monthly Rates (Non-Tobacco)

The table below shows sample rates from Aetna/Accendo for non-tobacco applicants. Rates are applicable across most states and were sourced from broker-published rate data dated March 2026.

| Age | Female — $5K | Female — $10K | Female — $25K | Male — $5K | Male — $10K | Male — $25K |

|---|---|---|---|---|---|---|

| 50 | $15 | $27 | $63 | $19 | $34 | $81 |

| 60 | $22 | $41 | $96 | $27 | $51 | $123 |

| 70 | $31 | $58 | $140 | $38 | $73 | $178 |

| 80 | $52 | $101 | $248 | $72 | $140 | $345 |

Source: Aetna/Accendo final expense rate data via Choice Mutual, March 2026. Rates are samples only; your actual premium depends on your health classification and the carrier you qualify for.

The $20–$150/month range quoted elsewhere holds reasonably well for $10,000 in coverage between ages 50 and 80. For $25,000 policies — particularly for men at age 80 — rates run significantly higher. Your health classification is the other key variable, and it affects your rate just as much as age.

Health Classification and What It Means for Your Rate

Your health status determines which benefit tier you fall into, which directly affects your premium:

- Level benefit — full death benefit from day one, lowest premiums; requires passing health questions

- Graded benefit — partial payout in years one and two, full benefit from year three onward; for applicants with moderate health conditions; higher premiums than level

- Guaranteed issue — no health questions at all, full benefit after a two-year waiting period; highest premiums

Applying younger locks in the lower rate permanently. Because final expense is whole life, your premium stays fixed and your coverage remains in force as long as you keep paying.

Who Qualifies for Final Expense Insurance in Kentucky?

Most carriers offer final expense policies to Kentucky residents between ages 45 and 85 — some carriers extend to 89 or 90. No medical exam is required at any age in this range.

What "Simplified Underwriting" Actually Means

Simplified underwriting means you answer a short list of health questions (typically 5–15), and the carrier reviews your prescription history and MIB records in the background. There is no paramedical exam, no blood draw, and no waiting weeks for a doctor's report. Many applicants receive a decision the same day.

Kentucky's Health Context

Kentucky's life expectancy was 73.5 years in 2021, well below the national average. Kentucky adults have an 11.2% COPD prevalence — one of the highest rates in the country — and 13.8% of Kentucky adults have been diagnosed with diabetes. Heart disease mortality sits at 196.9 deaths per 100,000 residents.

Final expense underwriting was built with these realities in mind — many carriers have designed their products to accommodate chronic conditions that would disqualify someone from standard life insurance.

What Typically Qualifies vs. What May Not

Conditions that often qualify for level or graded benefit coverage:

- Controlled type 2 diabetes

- COPD (stable)

- Heart attack more than 2 years ago

- Cancer in remission for 2+ years

- High blood pressure on medication

When guaranteed issue is the likely path:

- Active cancer (currently in treatment)

- Congestive heart failure

- Currently on dialysis

- Recent major cardiac event

These are general patterns — specific carrier decisions vary. Vellum Life Group works with 15+ carriers, which makes it possible to match your health profile to the carrier most likely to offer you the strongest benefit tier.

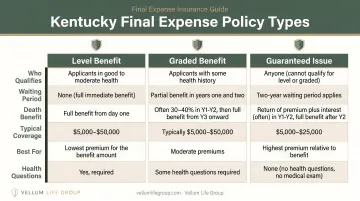

Types of Final Expense Policies Available in Kentucky

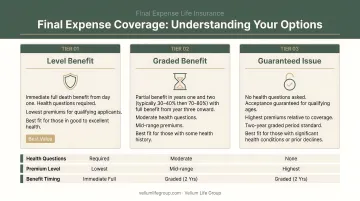

The Three Policy Tiers

Level Benefit (Immediate Coverage)

- Full death benefit from day one

- Lowest premiums of the three tiers

- Requires answering health questions and passing underwriting

- Best option if your health qualifies

Graded Benefit

- Partial payout in years one and two (typically 25–50% of the death benefit)

- Full benefit kicks in at year three or later

- For applicants with moderate health conditions

- Premiums higher than level, lower than guaranteed issue

Guaranteed Issue

- No health questions — approval is guaranteed within the eligible age range

- Two-year waiting period before full death benefit is paid

- If death occurs during the waiting period, the insurer returns premiums paid plus interest

- Highest premiums; appropriate only when other options are unavailable

- No medical exam required, making it accessible regardless of health history

Once you understand which tier fits your situation, the next step is knowing how much coverage you can actually secure.

Coverage Amounts and Policy Structure

Most carriers in Kentucky offer coverage from $2,000 up to $25,000–$40,000, with select carriers offering policies up to $50,000 for eligible applicants. To cite verified carrier ranges: Mutual of Omaha's Living Promise goes up to $40,000 in its producer guide, and Foresters' PlanRight goes up to $35,000.

Because these are whole life policies, they build modest cash value over time that the policyholder can borrow against if needed. Unlike term insurance, which expires with no value, a final expense policy, once issued, stays in force for life.

An independent advisor can compare all three tiers side-by-side and match your health profile to the right option. Vellum Life Group partners with 15+ A-rated carriers — including Mutual of Omaha, Foresters Financial, Aetna, and Transamerica — so you're not limited to one carrier's offer.

What Kentucky Funerals and Burials Actually Cost

Planning your coverage amount requires understanding what funerals actually cost today. The NFDA's 2023 data provides the clearest benchmarks:

| Service Type | National Median Cost |

|---|---|

| Funeral with viewing and burial | $8,300 |

| Funeral with viewing and cremation | $6,280 |

These are median figures — costs in some Kentucky markets run higher. They also do not include the cemetery plot, grave marker, or vault, which can add $1,000–$3,000 or more.

Funeral Costs Are Only Part of the Picture

A final expense benefit commonly covers more than the funeral itself:

- Medical bills from the final months of life

- Outstanding credit card balances or personal loans

- Utility bills, rent, or mortgage payments due immediately after death

- Travel costs for family members coming from out of state

This is why many financial advisors suggest $10,000–$25,000 as a more practical target than a minimum-coverage policy.

The Cost-of-Waiting Problem

Funeral costs are rising. NFDA's 2023 study documented a 5.8% increase in the cost of a burial funeral between 2021 and 2023 — and that's during a period when overall inflation was running at 13.6%. Funeral costs have historically tracked below general inflation, but the trend is steadily upward.

Every year you wait also means applying at an older age — and premiums are locked in at the rate for your age at the time of application. Rising funeral costs combined with rising premiums make a straightforward case: the sooner you lock in coverage, the less you pay over time.

How to Find the Right Final Expense Policy in Kentucky

Independent Advisor vs. Single Carrier

Going directly to one carrier means you see one set of products at one price point. If that carrier's underwriting doesn't fit your health profile well, you may pay more than necessary or end up in a higher benefit tier than you need.

An independent advisor shops across multiple carriers using your specific age, health history, and budget. The result is a genuine comparison built around your situation, not a single carrier's product lineup.

What the Application Process Looks Like

Most people are surprised by how simple this is:

- Short consultation — phone or online, typically 20–30 minutes

- Health questions — answered verbally or on a simple form; no doctor visits

- Coverage selection — choose your benefit amount and name your beneficiary

- Decision — often same-day or within a few days for simplified issue policies

That's the entire process for most Kentucky applicants.

Getting Started with Vellum Life Group

Vellum Life Group is an independent, licensed insurance advisory firm founded by Eva Ikonomakos, who brings over 15 years of experience across financial services, healthcare, and international business. The firm works with 15+ A-rated carriers — including Mutual of Omaha, Foresters Financial, Aetna, Transamerica, and American Amicable — to match each client's health profile and budget with the right policy.

Getting started is straightforward:

- Free consultation — no obligation to purchase

- Transparent process — no jargon, no pressure from the first call

- Reach Eva directly — call 917-363-3554 or email info@vellumlifegroup.com

Kentucky Consumer Protections to Know Before You Buy

Replacement Policy Free Look: 30 Days

Kentucky law is clear on this: if you replace an existing life insurance policy with a new one, you have 30 days from delivery to return the replacement policy for an unconditional full refund. This is codified in KRS 304.12-030 and reinforced by 806 KAR 12:080.

Note: the replacement-specific return window in Kentucky is 30 days, not 20 days. If you're purchasing a brand-new policy (not replacing an existing one), confirm the applicable free-look period directly with your carrier, as specific provisions vary by policy form.

The FTC Funeral Rule

State protections govern your policy — but a separate federal law governs what happens when your beneficiary uses it. The FTC Funeral Rule gives consumers the following rights when working with funeral homes:

- Funeral homes must provide a General Price List with itemized pricing upon request

- You have the right to choose only the services you want — no bundled packages required

- Funeral homes must accept a casket you purchased elsewhere and cannot charge a handling fee

These protections mean your beneficiary isn't locked into overpriced packages — they can direct the death benefit toward exactly the services your family chooses.

Frequently Asked Questions

What is the average monthly cost of final expense insurance in Kentucky?

Premiums vary by age, gender, health, and coverage amount. For $10,000 in coverage, non-tobacco rates generally run $27–$101/month for women and $34–$140/month for men (ages 50–80). Higher coverage amounts and guaranteed issue policies cost more.

Who is eligible for final expense insurance in Kentucky?

Most Kentucky residents between ages 45 and 85 are eligible, with no medical exam required. People with common chronic conditions — including controlled diabetes, COPD, and a history of heart disease — can typically qualify for some level of coverage, even if it's through a graded benefit or guaranteed issue policy.

Are $50,000 final expense policies available in Kentucky?

Select carriers offer coverage up to $50,000, though availability depends on age and health classification. Verified maximums include $40,000 through Mutual of Omaha's Living Promise and $35,000 through Foresters' PlanRight. An independent advisor can match you with carriers offering higher benefit amounts for your profile.

Is there a waiting period for final expense insurance in Kentucky?

Level benefit policies provide full coverage from day one. Graded benefit policies pay a partial benefit in the first two years. Guaranteed issue policies have a mandatory two-year waiting period — if the insured passes away during that period, the insurer returns premiums paid plus interest to the beneficiary.

Can I get final expense insurance in Kentucky if I have serious health problems?

Yes. Guaranteed issue policies approve any Kentucky resident within the eligible age range regardless of health history — no medical exam, no health questions. Premiums are higher than standard policies, and the two-year waiting period applies, but coverage is available.

What is the difference between final expense insurance and a prepaid funeral plan?

A prepaid funeral plan is a contract with one specific funeral home locking in specific services at today's prices. Final expense insurance pays a flexible cash benefit to any beneficiary, who can use it for any expense at any funeral home — giving your family far more control over how the money is spent.