Life insurance exists to prevent exactly this. Yet according to LIMRA's 2025 Insurance Barometer data, 40% of American adults say their loved ones would be barely or not at all financially secure if the primary wage earner died unexpectedly. That's not a fringe concern — that's nearly half the country.

This guide covers what income replacement life insurance is, how it works, which policy type fits most families, how to calculate the right coverage amount, and when to revisit your plan as life changes.

Key Takeaways

- Life insurance gives beneficiaries a tax-free lump sum to cover ongoing expenses after the policyholder's death.

- Term life is the most cost-effective choice for income replacement during peak earning years.

- Coverage should account for salary, mortgage debt, childcare, college costs, and inflation — not salary alone.

- Calculate coverage for stay-at-home parents — their economic contribution is real and quantifiable.

- Major life events — marriage, new children, home purchases, income changes — are signals to review your policy.

Why Income Replacement Through Life Insurance Matters

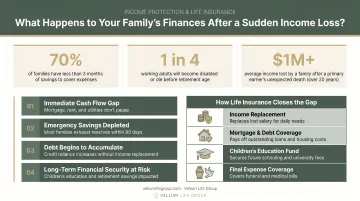

Most households run closer to the financial edge than they realize. LIMRA's 2024 research found that 47% of consumers would have trouble paying living expenses within six months of a primary wage earner's death. Six months. For most families, that's not enough time to rearrange finances, reorganize income sources, or sell assets without significant disruption.

The coverage gap extends beyond breadwinners. Consider what happens when a stay-at-home parent dies. There's no lost paycheck — but there are immediate, real costs:

- Full-time childcare at a national average of $13,128 per year (Child Care Aware of America, 2024 data)

- Household management, meal preparation, and scheduling

- Transportation, school coordination, eldercare for aging relatives

These aren't abstract costs. They're bills that arrive the following week.

Life insurance provides a lump-sum death benefit that replaces the financial contribution — paid or unpaid — that the deceased would have made. It gives surviving family members time to stabilize without being forced into rushed, pressure-driven decisions.

That stability matters in single- and dual-income households alike. In a two-income home, losing one earner can cut household cash flow by 40–60% overnight while fixed costs — mortgage, insurance, debt payments — remain unchanged.

How Life Insurance Works as an Income Replacement Tool

The Core Mechanics

The policyholder pays regular premiums to keep the policy active. Upon death, the insurance company pays a death benefit directly to the named beneficiaries. Under IRS rules and IRC Section 101(a)(1), life insurance death benefits are generally not included in gross income — meaning the full benefit is available to the family, not reduced by federal taxes.

That tax-free status has real dollar impact. A $1 million death benefit delivers $1 million to the beneficiary — unlike an inherited investment account that may trigger capital gains taxes on the growth portion.

Lump Sum vs. Installment Payouts

Most policies default to a lump-sum payout, and for good reason — it gives the beneficiary full control and flexibility. Some insurers also offer installment payment options, where the death benefit is distributed in monthly amounts over a set period.

| Payout Structure | Pros | Cons |

|---|---|---|

| Lump Sum | Full flexibility, immediate access | Risk of mismanagement without financial guidance |

| Installments | Mimics a paycheck, easier to budget | Less flexibility; may earn minimal interest |

For most families, the lump sum is the better default — though how you manage it afterward matters just as much. A financial advisor can help structure how those funds are invested or distributed over time.

What the Death Benefit Should Cover

The death benefit isn't just a salary replacement. A complete income replacement plan should account for:

- Ongoing living expenses — housing, food, utilities, transportation

- Debt obligations — mortgage balance, car loans, credit cards, student loans

- Future goals — college tuition, retirement savings contributions

- Final expenses — funeral costs, medical bills

Beyond the death benefit itself, permanent policies (whole life, universal life) build cash value over time. That value can be accessed via loans or withdrawals during the policyholder's lifetime — a secondary feature, not the primary reason most families purchase coverage, but a meaningful one during job loss or illness.

Term vs. Permanent Life Insurance for Income Replacement

Term Life: The Income Replacement Workhorse

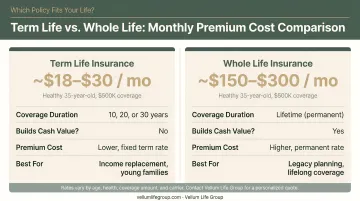

Term life insurance provides coverage for a fixed period — typically 10, 20, or 30 years. If the insured dies during that term, beneficiaries receive the death benefit; if the term expires, there's no payout and no cash value.

For income replacement, this structure fits most families well. The coverage period aligns with the years of greatest financial obligation: while children are at home, while the mortgage is being paid down, while career earnings are at their peak.

The cost difference versus permanent coverage is substantial. Policygenius 2024 data puts a 20-year, $500,000 term policy for a healthy 30-year-old nonsmoker at around $23/month for women and $29/month for men. Compare that to a whole life policy at the same coverage level:

The cost difference versus permanent coverage is substantial. Policygenius 2024 data puts a 20-year, $500,000 term policy for a healthy 30-year-old nonsmoker at around $23/month for women and $29/month for men. Compare that to a whole life policy at the same coverage level:

| Policy Type | Monthly Premium (Women) | Monthly Premium (Men) |

|---|---|---|

| 20-year term ($500K, age 30) | ~$23 | ~$29 |

| Whole life ($500K, age 35) | ~$481 | ~$571 |

That's a $400–$500/month difference for the same death benefit.

Permanent Life: When It Makes Sense

Whole life and universal life insurance provide lifelong coverage with a cash value component. They cost significantly more, but they serve different needs:

- Estate planning with a predictable death benefit at any age

- Lifelong dependents who will require financial support indefinitely

- Tax-advantaged savings alongside permanent coverage

- Business succession planning

For pure income replacement during working years with dependents at home, permanent life is rarely the most efficient choice.

The Laddering Strategy

Some families use a policy laddering approach — holding multiple term policies with staggered end dates that match declining financial obligations over time. For example:

- A 30-year term to cover the mortgage

- A 20-year term to cover the child-rearing years

As obligations decrease, shorter policies expire naturally without the cost of maintaining a single large policy. Policygenius estimates this approach can save over 50% compared to maintaining a single oversized policy. Because laddering works best when you can compare staggered options across multiple carriers, an independent advisor has a clear advantage here. Vellum Life Group works with 15+ carrier partners — including Mutual of Omaha, Transamerica, and Corebridge Financial — so the comparison happens in one conversation rather than across multiple separate quotes.

How to Calculate Your Income Replacement Coverage Amount

Starting with the Basics

The simplest starting formula:

Annual income × number of years of support needed = baseline coverage

Example: $70,000/year × 20 years = $1.4 million baseline

That's a floor, not a ceiling. It doesn't account for inflation, debt, or specific family costs.

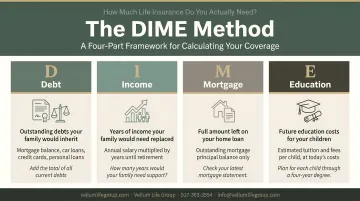

The DIME Method

A more comprehensive framework is the DIME method, a standard needs-analysis tool used across the life insurance industry:

| Component | What to Include |

|---|---|

| D — Debt | All outstanding loans, credit cards, car loans, student debt |

| I — Income | Annual salary × years of support needed |

| M — Mortgage | Full remaining mortgage balance |

| E — Education | Estimated future college costs per child |

Add all four components. That sum becomes a more complete coverage target.

Factoring In Inflation

A fixed death benefit loses purchasing power over time. The Life Happens needs calculator uses a 2% annual inflation assumption alongside a 4% interest rate for present-value calculations. Applied to a $1.4 million baseline over 20 years, the inflation-adjusted need can climb by 20–30% or more. A financial advisor or online calculator can run this projection based on your specific numbers.

Non-Working Spouses Have Calculable Value

A stay-at-home parent's death doesn't eliminate financial loss — it redirects it. The services they provide have real market value. According to Salary.com's annual survey, the estimated median annual value of a stay-at-home parent's unpaid work exceeds $184,820, spanning more than 20 roles including childcare, household management, and family coordination.

Coverage for a non-working spouse should account for the annual cost of replacing those services, multiplied by the number of years those services would have been needed.

What to Subtract

The DIME total represents maximum need. Subtract:

- Existing savings and accessible liquid assets

- A surviving spouse's continuing income

- Existing life insurance policies (group plan coverage and individual)

- Retirement accounts that would be accessible

The net figure is a more accurate coverage need — and often lower than the initial DIME calculation.

These calculations are a starting point, not a final answer. Vellum Life Group uses a general guideline of 10–12x annual income as an initial benchmark, then refines that number during a free consultation based on each family's specific debts, dependents, and financial goals.

Key Factors That Affect How Much Coverage You Need

Three factors consistently shape how much income replacement coverage a family actually needs. Understanding each one prevents the most common mistake: underinsuring at the worst possible time.

Life Stage and Dependents

A 30-year-old with young children and a 30-year mortgage needs substantially more coverage than a 55-year-old whose kids are independent and the home is paid off. Coverage needs shift along two axes:

- Policy amount — higher when dependents are young and debts are large

- Term length — longer when financial obligations extend further into the future

Existing Debt

Large obligations amplify the coverage gap. A $400,000 mortgage, student loans, and a car payment don't pause because the primary earner died. Each outstanding debt should appear explicitly in the coverage calculation.

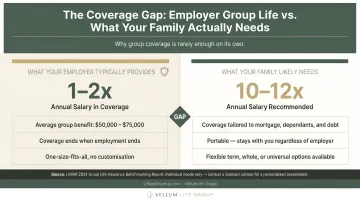

The Group Coverage Trap

Many people assume their group plan benefits cover them. They don't — not fully. According to BLS March 2025 data, 59% of private industry workers have access to group-provided life insurance. But LIMRA 2025 reports the median basic group plan coverage is just $20,000 or 1x salary.

The risks of relying solely on group coverage:

- The benefit is typically 1–2x salary — far below income replacement needs

- Coverage ends when the plan ends (plan changes, lapses, or transitions)

- 49% of households with only group life insurance say their families would struggle financially in less than six months if a wage earner died

Individual coverage supplements what your group plan provides — and unlike a plan-based policy, it travels with you through every coverage transition.

When to Review and Update Your Life Insurance Coverage

Life insurance isn't a set-it-and-forget-it decision. Coverage that made sense three years ago may be inadequate — or excessive — today.

Schedule a policy review after any of these events:

- Getting married or divorced

- Having or adopting a child

- Purchasing a home or refinancing a mortgage

- A significant salary increase or decrease

- A spouse returning to or leaving the workforce

- A child leaving home

- Paying off a major debt

- Approaching retirement

Each event can shift your coverage need up or down. Marriage adds a dependent; paying off a mortgage reduces the protection gap. Reassessing after each major change ensures your policy reflects what your family actually depends on — not outdated circumstances.

That's where an independent advisor makes the process straightforward. Vellum Life Group provides annual policy reviews as part of their ongoing client support — included at no additional cost. For existing policyholders who haven't reviewed coverage recently, or for those just getting started, reach out for a free consultation at info@vellumlifegroup.com or by calling 917-363-3554.

Frequently Asked Questions

How does life insurance replace income?

When the insured dies, the life insurance company pays a tax-free death benefit to the named beneficiaries. That lump sum can be used to cover the expenses the policyholder's income would have funded — housing, childcare, debt payments, and daily living costs — giving the family financial stability during a difficult transition.

How much life insurance do I need to replace my income?

A starting point is annual income multiplied by the number of years of support needed. The DIME method (Debt, Income, Mortgage, Education) provides a more complete picture by factoring in your specific debts, dependents, existing assets, and coverage timeline.

Is term or whole life insurance better for income replacement?

Term life is the right choice for most people — it offers higher coverage at lower premiums during the years when financial obligations are greatest. Permanent life may suit those with estate planning needs, lifelong dependents, or a goal to build tax-advantaged cash value.

Should a stay-at-home parent get life insurance for income replacement?

Yes. Non-working spouses provide real economic value through childcare, household management, and other services that would cost thousands per month to replace. Their death creates immediate, calculable financial costs that warrant life insurance coverage even without a traditional paycheck.

What happens if I only have group life insurance through a group plan?

Group plan coverage typically pays only 1–2x annual salary — well short of most income replacement needs. It's also tied to your plan and may be lost if the plan changes or lapses. Individual coverage supplements the gap and remains in force regardless of your coverage status.

Can I get life insurance if I have cirrhosis?

It depends on the severity and stage of the condition. Some carriers, including certain ones in Vellum Life Group's network, take a more flexible approach to impaired-risk underwriting. Working with an independent advisor who can shop across multiple carriers improves your chances of securing coverage at a competitive rate.