Convertible term life insurance solves this problem directly. It's a provision built into many term policies that lets you switch to permanent coverage without a new medical exam, even if your health has changed significantly since your original application.

This guide explains exactly how convertible term life insurance works, what happens during a conversion, when to act, and what to watch out for before the window closes permanently.

Key Takeaways

- Convert to permanent coverage without a new medical exam, even if your health has declined

- Your original health rating carries forward — but premiums are recalculated at your current age

- The conversion window has a hard deadline that cannot be reinstated once it passes

- You can convert all or only a portion of your death benefit to permanent coverage

- Compare permanent policy types against your financial goals before the conversion deadline closes

What Is Convertible Term Life Insurance?

Convertible term life insurance is a standard term policy that includes a conversion privilege — either as a built-in provision or an optional rider — allowing the policyholder to exchange their temporary coverage for a permanent policy within a defined period.

The New York Department of Financial Services defines it clearly: a conversion provision lets the term owner convert to a permanent policy during a specified period without showing that the insured is in good health. That single feature — no proof of good health required — is what makes the conversion privilege genuinely valuable.

What Convertible Term Is Not

Convertible term is often confused with other policy types. Here's what it is not:

- Not a separate product — it's a feature embedded in (or added to) a term policy

- Not automatic — you must actively elect to convert before the deadline

- **Not the same as renewable term** — renewal simply extends the same temporary coverage at increasing rates; conversion produces a fundamentally different type of policy with permanent protection and cash value

Most people start with term coverage because premiums are lower at younger ages. Convertibility gives them a future pathway to permanent protection without locking in higher permanent premiums from day one. How that conversion pathway is structured — and what it costs — depends on the carrier.

Conversion Rider vs. Built-In Provision

Whether convertibility costs extra depends on the carrier and product:

- Built-in provision: Some carriers include convertibility as a standard contractual feature at no additional cost

- Conversion rider: Others require adding a named rider, which adds a small amount to the premium

- Extended Conversion Rider (ECR): An optional add-on that extends the standard conversion window beyond its default limit — sometimes up to the full term length or a maximum age. Guardian calls this an Extended Conversion Rider; Ameritas uses the name Conversion Extension Rider

For example, Guardian's Standard Level Term includes a built-in 5-year conversion window, with the ECR available to extend it up to 30 years. Ameritas's Value Plus Term offers a standard 5-year window, extended by rider to the end of the level term or the policy anniversary nearest age 70.

How Does Convertible Term Life Insurance Work?

The conversion process moves through several stages: from the initial policy setup to the moment you elect to convert. Knowing what happens at each stage helps you act before the window closes.

The Conversion Window

Every convertible policy has a defined window during which you can elect to convert. Common structures include:

- The first 5 years of the policy (standard window at many carriers)

- The entire level-premium period (available with ECR at some carriers)

- Up to a maximum attained age, typically 65, 70, or in some cases 80

MassMutual's producer materials show windows ranging from the 5th policy anniversary to ages 65, 70, or 80 depending on the product series. Pacific Life allows conversion within the level premium period up to attained age 70.

This deadline is a hard cutoff. Once the window expires, the conversion option is permanently gone — there is no reinstatement. No change in health, finances, or circumstance will reopen it.

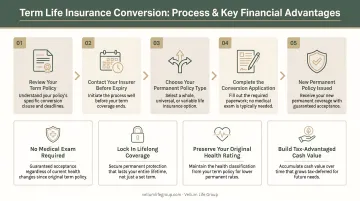

The Conversion Mechanics

When you decide to convert, here's what happens:

- Contact your insurer or advisor to express intent to convert

- Choose your permanent policy type — whole life, universal life, or variable universal life, depending on what your carrier offers

- Complete conversion paperwork — no new medical exam, no health questionnaire, no new underwriting

Two things happen at conversion that work in your favor:

- Your health rating is locked in. The insurer uses the risk class from your original term application. If your health has declined since then, this is a significant financial advantage — you're effectively getting permanent coverage priced as if you were still as healthy as you were years ago.

- Premiums are recalculated at your current age. The health classification carries forward, but permanent policy premiums are set based on how old you are at the time of conversion. Converting earlier means lower ongoing premiums.

Full vs. Partial Conversion

Many insurers allow partial conversions, where only a portion of the term death benefit moves to permanent coverage while the remainder stays as term insurance.

Example: You have a $500,000 term policy. You convert $200,000 to whole life insurance, leaving $300,000 as term coverage. The result is two active policies: the new permanent policy with its own premium, and the remaining term running until expiration.

Partial conversion lets you establish permanent coverage at a lower cost while keeping your term benefit in place. Carriers handle this differently, so confirm the rules with your insurer before applying:

- Transamerica, Pacific Life, and MassMutual all offer partial conversion

- Each carrier applies minimum face amount requirements

- Pacific Life limits partial conversions to two per original policy

What Can You Convert To?

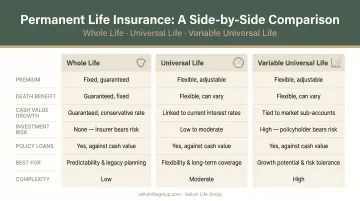

Conversion options vary by carrier, but the three most common permanent policy types available are:

| Policy Type | Key Features | Best For |

|---|---|---|

| Whole Life | Fixed premiums, guaranteed death benefit, steady cash value growth | Those prioritizing guarantees and stability |

| Universal Life | Flexible premiums, interest-based cash value accumulation | Those wanting premium flexibility |

| Variable Universal Life | Investment subaccounts with market-linked growth potential | Those comfortable with investment risk for higher growth potential |

That said, not every carrier offers all three options. Many restrict conversion to specific products within their lineup — Pacific Life, for example, converts exclusively to its PL Promise Conversion UL product. Corebridge Direct lists state-based restrictions on available conversion products, with certain options unavailable in New York or Vermont.

The permanent policy you choose at conversion should match your actual financial goals:

- Whole life — best if you want guarantees and a stable cash value asset

- Universal life — best if you need the flexibility to adjust premiums as income changes

- Variable universal life — best if you have a longer time horizon and can absorb investment risk for higher growth potential

Vellum Life Group works with 15+ A-rated carriers, including Ameritas, Corebridge Financial, Transamerica, and Mutual of Omaha. Before you commit to converting with your existing insurer, it's worth comparing what permanent options are available elsewhere — the right fit may come from a different carrier entirely.

Pros and Cons of Convertible Term Life Insurance

Pros

- Your original health rating applies at conversion — no new medical exam required. This matters more than most people expect: CDC data from 2025 shows 76.4% of U.S. adults have one or more chronic conditions, meaning health changes during your term are common, not rare

- Start with affordable term premiums now and keep the door open to permanent coverage later. According to Guardian, convertible policies may cost only "fractionally more" than non-convertible term — a small price for the added flexibility

- Cash value begins building once you convert to a permanent policy. That cash value grows tax-deferred under IRC Section 7702 and can be borrowed against, used to offset premiums, or accessed as a supplemental financial resource

Cons

- Conversion deadlines vary by carrier and rarely come with reminders — policyholders who lose track of the window lose the option permanently

- Whole life can cost more than five times what term costs at the same coverage amount. Run the numbers before converting to confirm the new premium fits your long-term budget

- You can only convert into permanent products your insurer makes available — which may not be the most competitive options on the market

When Should You Consider Converting?

Most policyholders don't think about conversion until a deadline looms or a health diagnosis changes the math. These four situations are worth acting on sooner.

Health Has Changed Since You Bought the Policy

If a chronic condition has emerged since you bought your term policy, converting while your original health rating still applies locks in pricing that new underwriting would almost certainly not match. Given that KFF reports 54.31% of U.S. adults ages 18-64 had at least one chronic condition in 2023, this scenario is common — not exceptional.

Your Conversion Window Is Approaching Its End

This is the most actionable signal. Know your conversion deadline and set a calendar review well before it arrives. Working with an independent advisor like Vellum Life Group — which conducts annual policy reviews for clients — means you're less likely to miss the window.

Because we work with multiple A-rated carriers, we can also help you compare permanent policy options across insurers before you commit to the conversion product your current carrier offers.

Your Financial Goals Have Shifted Toward Legacy Planning

If estate planning, wealth transfer, or leaving a guaranteed death benefit for heirs has become a priority, the conversion pathway is often the most cost-effective route to permanent coverage — no re-underwriting, no new health review. This is especially relevant for individuals managing long-term legacy planning or succession planning needs.

You Want to Start Building Cash Value

The earlier you convert, the more time cash value has to accumulate. Inside a qualifying permanent policy, that growth is tax-deferred — meaning you don't owe income tax each year on the policy's growth. Per IRS Publication 525, taxable gain is generally recognized only if you surrender the policy for cash above your cost basis, not while the policy remains in force.

Frequently Asked Questions

Is a convertible term life insurance policy worth it?

For most people, the small premium difference between a convertible and non-convertible term policy is justified by the flexibility it provides. If there's any uncertainty about future health or long-term coverage needs, the built-in conversion privilege is a low-cost safety net in case your health changes later.

Does taking Lexapro affect my ability to get convertible term life insurance?

Lexapro (escitalopram) may affect your initial health rating and premium when applying for term coverage, but it doesn't prevent approval. At conversion, no new medical exam or health review is required — so your Lexapro use would not be a factor in the conversion itself.

Can I get convertible term life insurance if I have a serious medical condition like lupus or cirrhosis?

A serious condition may result in a rated policy or higher premium at initial application, but most conditions won't disqualify you outright. An independent advisor can shop across multiple carriers to find the most favorable underwriting for your specific health history.

Does converting term life insurance require a new medical exam?

No. Conversion requires no new medical exam and no health questionnaire. The insurer uses the health rating from your original term application, which makes conversion especially valuable if your health has changed since you first bought the policy.

What is the conversion window and how long do I have?

It varies. Common structures include the first 5 years of the policy, the full level-premium period (with an Extended Conversion Rider), or up to a maximum age of 65–70. Check your specific policy documents or ask your advisor for the exact deadline.

Can I partially convert my term life insurance policy?

Yes, many insurers allow partial conversions where only a portion of the death benefit moves to permanent coverage. This creates two active policies and can help manage the premium increase while still establishing some permanent protection.