This isn't a rare scenario. According to LIMRA's 2025 data, roughly 100 million American adults believe they need more life insurance than they currently have. The gap between what people own and what they actually need keeps growing — and outdated policies are a major reason why.

This guide covers exactly what to review, which life events require immediate action, what the 2026 tax landscape means for your policy, and the most common mistakes people make when they finally do sit down and look at their coverage.

Key Takeaways

- Review your policy at least once a year and immediately after any major life event

- Verify beneficiary designations — they override your will, and outdated ones can't be corrected after death

- The 2026 federal estate tax exemption rises to $15 million per individual — larger estates should review policy ownership structures now

- A health improvement like quitting smoking can cut your premiums by 50% or more

- An independent advisor with access to multiple A-rated carriers can compare your current policy against today's market at no cost to you

Life Events That Should Trigger a Life Insurance Review

Most people know they should review their life insurance "at some point." Few have a clear list of what actually requires action. These are the events that do.

Marriage or Divorce

Marriage often creates shared financial dependency for the first time. Both partners may need new or updated coverage, and existing beneficiary designations — which may still name a parent or a prior partner — need to be corrected immediately.

Divorce is equally urgent. Without updating beneficiaries, an ex-spouse may remain legally entitled to the death benefit. In Sveen v. Melin (2018), the U.S. Supreme Court upheld Minnesota's revocation-on-divorce statute, which automatically revokes an ex-spouse's designation after divorce.

That protection only exists in 26 states — and ERISA can preempt state law for group-sponsored plans, meaning group policies may not follow the same rules.

Don't assume the law handles it. Update the designation yourself.

Having a Child or Gaining a New Dependent

The financial consequences of a parent's death change dramatically when children enter the picture. Coverage that was adequate for a couple rarely accounts for childcare costs, lost caregiver services, and education expenses. The USDA estimated it costs $233,610 to raise a child through age 17 for a middle-income family — and that figure doesn't include college.

One important detail: never name a minor directly as a beneficiary. Courts may need to appoint someone to manage the proceeds, adding attorney fees and delays. A trust or UTMA custodian designation is the cleaner route.

Buying, Refinancing, or Paying Off a Home

A mortgage is the largest single obligation most households carry. U.S. mortgage balances totaled $13.19 trillion at the end of Q1 2026. Taking on that obligation is a clear signal to ensure a surviving spouse could keep making payments.

Paying off a mortgage flips the equation — existing coverage may now exceed what you need, freeing up premiums for other priorities. Refinancing that extends your loan term also warrants a second look.

Significant Career or Income Changes

Changing plans can eliminate group-based life insurance the day the plan ends. According to LIMRA, 26% of life insurance owners rely solely on group coverage through a group plan — coverage that doesn't move with them.

A promotion or income increase creates a different problem: current coverage may no longer reflect what a family would need to replace. Plan-based coverage is typically one to three times salary. For most households, that's not enough on its own.

Retirement Planning or Reaching a Financial Milestone

As retirement approaches, the purpose of life insurance shifts — and so does what adequate coverage looks like. Income replacement becomes less central, while other needs step forward:

- Funding estate liquidity or minimizing the tax burden on heirs

- Supplementing a spouse's retirement income if one partner outlives the other

- Leaving a legacy gift to family or a charitable cause

A policy built around income replacement at 40 often needs to be restructured by 60. The right coverage amount changes — sometimes down, sometimes up — depending on what you're actually protecting against.

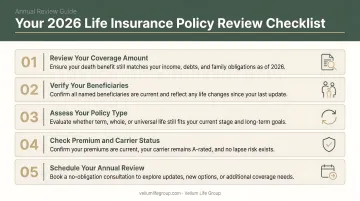

Your 2026 Life Insurance Policy Review Checklist

Before you start, pull out your actual policy documents, your most recent annual statement, and your beneficiary designation forms. You can't verify what you can't see.

Step 1: Verify Your Coverage Amount

The question isn't whether you have coverage — it's whether you have enough.

Life Happens recommends a rough starting point of 10 to 15 times gross annual income, plus approximately $100,000 per child for education. A more precise method from the CFP Board: divide the annual income your family needs to replace by a conservative return rate (4% is commonly used). A $60,000 annual income need translates to a $1.5 million death benefit under that model.

What to factor in:

- Current income and how many years it needs to be replaced

- Outstanding mortgage and other debts

- Estimated education costs per child

- Childcare or caregiving costs if a non-earning spouse passes

- Any other financial obligations specific to your dependents

Step 2: Confirm and Update Beneficiaries

Beneficiary designations override your will. Whatever name is on the policy receives the proceeds — regardless of what any other legal document says.

Verify:

- Primary beneficiary name, contact information, and relationship

- Contingent beneficiary (who receives proceeds if the primary predeceases you)

- No named beneficiary is a minor without a trust structure in place

- No listed beneficiary is deceased

This takes under 10 minutes and is the single most consequential step on this list.

Step 3: Review Policy Type and Term Status

Term policies have an expiration date — and many people don't know how close theirs is. Check:

- Remaining term length — is coverage expiring in 2–3 years?

- Conversion option — does your policy allow conversion to permanent coverage without a new medical exam? This is valuable if your health has changed since you originally bought the policy

- Policy fit — does the original policy type still match your current goals? A term policy bought for income replacement may not serve well as a legacy planning tool

If conversion is available and your health has declined, using it before the term expires can lock in permanent coverage without new underwriting.

Step 4: Assess Premiums, Carrier Health, and Your Risk Classification

Confirm your premium amount is still accurate and payments are current. Then check three things most people skip:

- Carrier financial strength. A policy is only as valuable as the company behind it. Verify your carrier's current rating through A.M. Best or S&P Global — look for an A- or better (classified as "Excellent" by A.M. Best). Ratings can shift over time.

- Your health classification. If you've quit smoking, lost significant weight, or resolved a prior health condition, you may qualify for a better risk class and noticeably lower premiums. Smoker premiums are often two to four times higher than non-smoker rates. Most carriers require 12 months tobacco-free for basic non-smoker classification — and up to five or more years for top-tier rates.

- Whether your current rate is still competitive. Carriers price risk differently. A rate that was competitive five years ago may not be today, especially if your health has improved.

When health changes are in play, shopping across multiple carriers matters. Because each insurer weighs risk factors differently, the same applicant can receive meaningfully different offers. Eva Ikonomakos at Vellum Life Group works with 15+ A-rated carriers — including Mutual of Omaha, Transamerica, Corebridge Financial, and Ameritas — to identify where your current policy stands and whether a better option exists.

Step 5: Evaluate Active Riders

Riders are add-ons to your base policy. Some remain valuable throughout the policy's life; others become irrelevant as circumstances change.

Common riders to review:

| Rider | What It Does | Still Relevant? |

|---|---|---|

| Waiver of Premium | Waives premiums if you become disabled | Check disability income situation |

| Accidental Death Benefit | Pays extra if death is accidental | Assess value vs. cost |

| Child Term Rider | Covers children under the policy | May no longer be needed once children are financially independent |

| Long-Term Care Rider | Accelerates benefit for LTC expenses | Growing relevance as you age |

The Long-Term Care rider is the most commonly overlooked addition — particularly for policyholders in their 40s and 50s, when adding it is still affordable. Review whether your existing riders still match your life stage, and whether any gaps have opened up since you first bought the policy.

2026 Tax and Estate Planning Updates That Affect Life Insurance

The Estate Tax Exemption: What Actually Changed in 2026

This is where 2026 is genuinely different from prior years. Under the One Big Beautiful Bill (Public Law 119-21), the IRS has set the 2026 basic exclusion amount at $15,000,000 per individual — up from $13,990,000 in 2025. For married couples using portability, that's effectively $30 million.

Prior analysis anticipated the elevated exemptions from the 2017 Tax Cuts and Jobs Act would sunset to approximately $7 million in 2026. That did not happen. The new legislation locks in a higher threshold, but it doesn't eliminate the estate tax issue for everyone.

Why Policy Ownership Still Matters

Life insurance death benefits are income-tax-free for beneficiaries under IRC Section 101(a)(1). But under IRC Section 2042, if the insured owns the policy at death, the death benefit is included in the taxable estate.

For a policyholder with a $5 million death benefit, $3 million in home equity, and $8 million in retirement accounts, the combined estate could exceed the exemption threshold — triggering a federal estate tax rate of up to 40% on the excess.

Verify who owns your policy. If you own it and your estate is large, that death benefit increases your taxable estate.

The ILIT as a Solution

An Irrevocable Life Insurance Trust (ILIT) removes the death benefit from your taxable estate. The trust owns the policy — not you — so the proceeds don't count as part of your estate for tax purposes.

Key points:

- Setting up an ILIT requires working with an estate planning attorney

- Under IRC Section 2035, if you transfer an existing policy into an ILIT and die within three years, the IRS may still include the proceeds in your estate — so timing matters

- Starting with the ILIT as owner (rather than transferring an existing policy in) avoids the three-year rule entirely

These considerations primarily affect higher-net-worth individuals with significant estates. But anyone with a large death benefit plus significant home equity, retirement assets, or other holdings should run the numbers with a tax professional. An independent advisor can help you assess whether your current ownership structure creates unnecessary tax exposure before it becomes a problem.

Common Mistakes to Avoid During Your Policy Review

A policy review is only useful if it catches the right things. These three oversights come up most often — and carry the highest cost when missed:

Prioritizing premium over coverage. Cutting limits to reduce monthly costs can leave the family exposed at exactly the moment the policy was meant to help. Coverage adequacy comes before cost.

Skipping the beneficiary check. An outdated designation — naming an ex-spouse, a deceased person, or leaving the contingent blank — can send the death benefit somewhere unintended or into probate. It takes less than 10 minutes to verify.

Treating group coverage as a safety net. 26% of life insurance owners rely solely on group coverage. That coverage is typically one to three times salary, it's not portable, and it ends when the group plan lapses — leaving a real gap for anyone with a mortgage or dependents.

None of these take long to check. Each one can significantly change how well your policy actually performs when it matters.

When to Work With a Life Insurance Advisor

DIY reviews work for straightforward cases. Professional guidance adds the most value when:

- The policy is a permanent product (whole life, universal life) with cash value components

- A major life change has occurred and coverage needs are genuinely unclear

- You're approaching retirement and shifting from income replacement toward legacy planning

- The estate tax picture has become complex enough to warrant an ownership structure review

The key distinction: an independent advisor — unlike a single-carrier agent — can compare options across multiple companies without being limited to one product line. That matters most when your situation doesn't fit neatly into a single carrier's offerings.

Vellum Life Group's founder Eva Ikonomakos offers personalized annual reviews with access to 10+ A-rated carriers. She walks clients through their options without pushing a specific product — a straightforward process that has helped protect over 500 families and placed more than $50 million in coverage.

If you haven't reviewed your policy in the past year — or you've gone through any of the life events listed here — a no-obligation consultation is a practical next step. You can reach Eva at 917-363-3554, email info@vellumlifegroup.com, or book a free 30-minute session at calendly.com/eva-ikonomakos/30min.

Frequently Asked Questions

What are the life events that affect your life insurance needs?

Marriage, divorce, having or adopting a child, buying or paying off a home, changing jobs, retirement, and significant health changes all affect coverage needs. Any of these can leave an existing policy either inadequate or structurally misaligned with your current situation.

How often should you review your life insurance policy?

At minimum, once a year — and immediately after any major life event. Even when nothing dramatic has changed, an annual review confirms that beneficiary designations, coverage amounts, and premium payments are still accurate.

What happens if I don't update my life insurance beneficiaries?

The death benefit pays to whoever is named on the policy — not to whoever is named in your will. An outdated designation can direct proceeds to an ex-spouse, a deceased individual, or into probate. That outcome can't be reversed after the policyholder's death.

How does the 2026 estate tax exemption change affect life insurance?

The 2026 individual exemption is $15 million under the One Big Beautiful Bill. If you own your policy and your estate exceeds that threshold, the death benefit is still included in your taxable estate under IRC Section 2042 — potentially triggering up to 40% federal estate tax. Ask a tax advisor whether an ILIT ownership structure makes sense for your situation.

What are the 4 P's of life insurance?

The 4 P's refer to Premium (what you pay), Protection (the death benefit), Period (how long coverage lasts), and Policy (the contract terms and conditions). Together, they give you a clear framework for evaluating any policy.

Can you get life insurance if you have cirrhosis?

Cirrhosis is classified as a decline by many traditional underwriters — Banner Life's 2026 field guide lists it as a general decline. Depending on severity, simplified issue or guaranteed issue products may still be available. An independent advisor who can shop across multiple carriers gives you the best shot at finding coverage.