This scenario plays out more often than most policyholders expect, and it's entirely preventable. TAMRA — the Technical and Miscellaneous Revenue Act of 1988 — is the federal law that governs how quickly you can fund a life insurance policy before it loses its most valuable tax advantages. For anyone using an IUL as a retirement or wealth-building tool, understanding TAMRA isn't optional.

This article covers what TAMRA requires, how the 7-Pay Test works, what MEC status actually costs you, and how to keep your policy on the right side of the rules.

Key Takeaways

- The 7-Pay Test limits how quickly you can fund an IUL during its first seven policy years.

- Exceeding that limit — even once, even in year one — permanently reclassifies the policy as a Modified Endowment Contract (MEC).

- A MEC loses tax-free loan access and FIFO distribution treatment, which are the core tax advantages of a well-structured IUL.

- TAMRA compliance preserves tax-deferred growth, tax-free policy loans, and an income-tax-free death benefit.

- Proper policy design from day one, with consistent funding oversight by your advisor, is the only reliable way to stay compliant.

What Is TAMRA and Why Does It Apply to IULs?

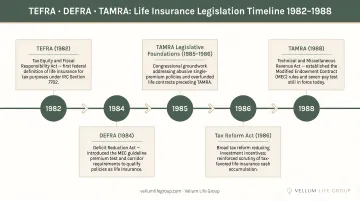

Before TAMRA, flexible universal life insurance had a feature Congress decided was too good to leave unregulated. Because universal life policies allow variable premium payments, high-net-worth individuals could deposit large sums early, let the cash value grow tax-deferred, and access funds through tax-free loans. The death benefit was almost incidental — these policies functioned more like tax-advantaged investment accounts than life insurance.

Congress addressed this in stages:

| Law | Year | What It Did |

|---|---|---|

| TEFRA (Tax Equity and Fiscal Responsibility Act) | 1982 | Set initial guidelines for flexible-premium life insurance to qualify for tax treatment as life insurance |

| DEFRA (Deficit Reduction Act) | 1984 | Enacted IRC §7702, defining what qualifies as a life insurance contract for federal tax purposes |

| TAMRA (Technical and Miscellaneous Revenue Act) | 1988 | Enacted IRC §7702A, introducing the 7-Pay Test and MEC classification for overfunded policies |

TAMRA didn't rewrite the earlier rules. It added a final layer targeting one specific problem: policies being overfunded too quickly to exploit tax advantages.

Why IULs Are Directly Affected

An Indexed Universal Life policy is a universal life insurance policy — one whose interest credits are linked to an external index rather than a fixed rate. Under IRC §7702A, the 7-Pay Test applies to any contract that qualifies as life insurance under IRC §7702, which includes every IUL.

The index-linked growth feature doesn't change that analysis. The same premium flexibility that makes IULs attractive for retirement planning is precisely what TAMRA was designed to regulate.

How the 7-Pay Test Works

The 7-Pay Test, defined under IRC §7702A(b), caps the cumulative premiums that can be paid into a life insurance policy during its first seven contract years. The cap equals the amount that would fully pay up the policy's guaranteed benefits over seven level annual payments — no more, no less.

Three points most policyholders misunderstand about this test:

- It's not a fixed dollar amount. The 7-Pay limit is calculated based on your age, the death benefit amount, and the specific policy terms. Two policies with identical premiums but different death benefits will have different limits.

- It's cumulative, not annual. The test measures the running total of premiums paid against the cumulative limit at any point in time. A single large payment in year one can fail the test immediately if it exceeds the cumulative limit for that moment.

- It can restart. Under IRC §7702A(c)(2)(A) and (c)(3)(A), certain material changes — most commonly a reduction in the death benefit — cause the test to be applied as if the contract had originally been issued at the reduced benefit level. A previously compliant policy can be pushed into MEC territory by a seemingly routine policy change.

The Correction Window

If a premium payment would trigger MEC status, it isn't automatically permanent at the moment of payment. Under IRC §7702A(e)(1)(B), premiums returned by the insurance company — with interest — within 60 days after the end of the contract year are treated as reducing premiums paid for 7-Pay Test purposes.

Carriers also have access to IRS correction procedures under Rev. Proc. 2001-42 for inadvertent, non-egregious MEC failures. Inadvertent is the operative word here — habitual overfunding doesn't qualify for correction relief.

What Happens When an IUL Fails the 7-Pay Test: MEC Status Explained

Once a policy fails the 7-Pay Test, it's reclassified as a Modified Endowment Contract under IRC §7702A(a). The policy remains valid life insurance — but the tax treatment of distributions changes in ways that matter.

The FIFO-to-LIFO Shift

This is the most consequential change. With a standard, compliant IUL:

- Withdrawals up to your cost basis (what you've paid in) come out tax-free first — FIFO (First In, First Out) treatment under IRC §72(e)(5)(A).

With a MEC:

- Gains are treated as coming out first under IRC §72(e)(10) — LIFO (Last In, First Out), meaning distributions are taxed as ordinary income until all gains have been distributed.

Loans and the 10% Penalty

In a MEC, loans, assignments, and pledges are all treated as taxable distributions under IRC §72(e)(10). That's a significant departure from the standard IUL, where IRC §72(e)(5)(C) explicitly excludes policy loans from taxable treatment.

The gap widens further for younger policyholders. Anyone under age 59½ faces an additional 10% penalty tax on the taxable portion under IRC §72(v)(1) — the same structure that applies to early IRA or 401(k) withdrawals.

What a MEC Still Keeps

A MEC isn't worthless. It retains several benefits worth noting:

- Cash value still grows tax-deferred

- The death benefit is still paid income-tax-free to beneficiaries under IRC §101(a)(1)

- The policy remains eligible for a 1035 exchange to another life insurance contract — but under IRC §7702A(a)(2), the new contract will also be classified as a MEC

MEC status is permanent. Once triggered and past the correction window, that classification sticks.

Tax Benefits You Preserve by Staying TAMRA-Compliant

Staying below the 7-Pay limit protects three tax advantages that make a properly structured IUL one of the most efficient vehicles for long-term wealth accumulation and income planning.

Three benefits hinge on §7702 compliance:

- Tax-deferred growth: Index-linked credits accumulate without annual taxation. No 1099 each year, no capital gains drag on compounding returns.

- Tax-free policy loans: Cash value accessed through loans isn't treated as taxable income. That means supplementing retirement income without pushing into a higher bracket or triggering Medicare premium surcharges.

- Income-tax-free death benefit: Under IRC §101(a)(1), proceeds paid to beneficiaries are excluded from gross income — delivering both protection and legacy value in a single contract.

Common Ways Policyholders Accidentally Trigger MEC Status

Most MEC triggers aren't the result of bad intentions — they're the result of incomplete information at the time a decision is made.

Three scenarios account for the majority of accidental MEC violations:

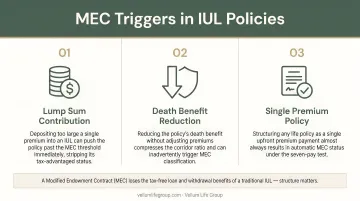

Large lump-sum payments early in the policy. A policyholder receives a bonus, an inheritance, or a large windfall and decides to accelerate IUL contributions. Without checking against the cumulative 7-Pay limit first, a single deposit can push the policy into MEC territory.

Reducing the death benefit. Under IRC §7702A(c)(2)(A), reducing benefits during the 7-Pay testing period triggers a recalculation — as if the policy had always carried the lower death benefit. Premiums that were compliant at the higher benefit level may suddenly exceed the limit. This catches many policyholders off guard, particularly those who reduce coverage to lower insurance costs as they age.

Single-premium life insurance. These policies are always MECs by design — the entire premium is paid at once, so the 7-Pay limit is exceeded immediately. This isn't a problem if the buyer understands it going in, but it's a clear reminder that policy structure needs to be defined before issuance, because the MEC classification cannot be undone once it takes effect.

How to Keep Your IUL Compliant: Working With the Right Advisor

TAMRA compliance isn't something you can address retroactively. It starts at policy design.

The death benefit must be sized correctly relative to planned premium contributions. This isn't arbitrary — the 7-Pay limit is calculated from the death benefit amount, so a policy with a larger death benefit accommodates more premium before hitting the MEC threshold. Premiums are typically structured across multiple years with this ceiling in mind.

Ongoing monitoring matters just as much as initial design. Life events that seem unrelated to insurance — receiving an inheritance, a change in income, or a large financial windfall — can create pressure to fund the policy more aggressively. Before any payment is made, the cumulative 7-Pay position should be checked.

This is the kind of work Eva Ikonomakos at Vellum Life Group focuses on. Working with multiple A-rated carriers, Eva structures IULs correctly from day one. She stays engaged throughout the policy's life to catch situations where a well-intentioned premium payment could trigger permanent MEC reclassification.

The annual review process serves as a practical compliance checkpoint — not a formality, but a scheduled opportunity to verify the policy's 7-Pay position before any funding decisions are made.

Frequently Asked Questions

What is TAMRA in life insurance?

TAMRA (Technical and Miscellaneous Revenue Act of 1988) is the federal law that enacted IRC §7702A, introducing the 7-Pay Test for life insurance policies. Premiums that exceed the cumulative 7-Pay limit during a policy's first seven years cause it to be reclassified as a Modified Endowment Contract, which loses key tax advantages on distributions and loans.

What is the best IUL life insurance policy?

There's no single "best" IUL — the right policy depends on your age, goals, and funding capacity. What matters most is a structure from an A-rated carrier designed to stay TAMRA-compliant and maximize cash value growth. An experienced independent advisor can compare options across carriers to find the right fit.

Can MEC status be reversed once triggered?

No. Under IRC §7702A(a)(2), MEC status is permanent. If the correction window (60 days after the contract year ends) has passed, the policy remains a MEC for its entire life — and a 1035 exchange into a new policy carries the MEC classification to the new contract.

Does the 7-Pay Test reset if I make changes to my policy?

Yes, in certain cases. Under IRC §7702A(c)(3)(A), a material change — including reducing the death benefit — causes the policy to be treated as a new contract on the date of the change. Previously compliant policies can be reclassified based on premiums already paid. Any policy change should be reviewed with an advisor before it's made.

What are the tax consequences of taking money out of a MEC?

Distributions from a MEC — including loans — are taxed on a LIFO basis under IRC §72(e)(10), meaning gains come out first as ordinary income. Policyholders under age 59½ also face a 10% additional tax under IRC §72(v)(1), similar to an early distribution from an IRA.

How is a TAMRA-compliant IUL different from a 401(k) for retirement savings?

A compliant IUL provides tax-free access through policy loans at any age, has no IRS contribution limits tied to earned income, and includes a death benefit. By contrast, a 401(k) caps 2026 elective deferrals at $24,500, distributions are generally fully taxable, and required minimum distributions begin at age 73.