Introduction

Most term life insurance buyers face a straightforward trade-off: pay premiums for 20 or 30 years, stay protected the whole time, and walk away with nothing if they never file a claim. For many people, that feels like money down the drain.

Return of premium (ROP) life insurance changes that equation. If you outlive your policy term, you get every dollar back.

This guide covers everything you need to evaluate ROP coverage: how it works, what it actually costs, how it stacks up against standard term and whole life insurance, and — critically — who it makes sense for and who it doesn't.

Key Takeaways

- ROP life insurance refunds 100% of premiums paid if you outlive the full term — the death benefit is unchanged if you don't

- Refunded premiums are generally not taxable income under IRS cost-basis rules

- ROP policies typically cost 2x to 5x more than equivalent standard term coverage

- Early cancellation results in forfeiting the refund entirely

- Best suited for financially stable individuals who can commit to 20–30 years of higher premiums

What Is Return of Premium Life Insurance?

The NAIC defines return of premium as a term life feature that refunds part or all premiums paid if the policyholder outlives the term and no death benefit is paid. Unlike standard term life, where the coverage simply expires at the end of the period, an ROP policy hands your money back.

Two Ways ROP Is Structured

Insurers offer ROP in two forms:

- Standalone ROP term policy — the entire policy is built around the return feature; premiums are higher from the start

- ROP rider on a term or universal life policy: an add-on to a base policy that layers the refund benefit on top of existing coverage

Availability varies significantly by carrier and state. Some insurers offer both structures; others offer only one. It's worth comparing options across multiple carriers before you commit.

Death Benefit and Tax Treatment

The ROP feature doesn't touch the death benefit. If the insured dies during the term, beneficiaries receive the full payout — exactly as they would with a standard term policy.

On the tax side, IRS Publication 525 and Revenue Ruling 2009-13 establish that life insurance amounts received are included in gross income only to the extent they exceed the policyholder's investment in the contract. Since returned ROP premiums represent money already paid in — not a gain — they're generally not taxable. A tax professional can confirm how this applies to your specific situation.

ROP is not an investment. The policyholder receives back exactly what they paid — no interest, no growth. It's a cost-recovery feature, not a wealth-building tool.

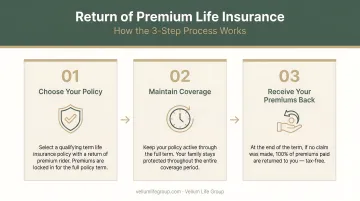

How Return of Premium Life Insurance Works

ROP policies follow a simple three-step structure:

- Pay premiums — monthly or annually, at a higher rate than a comparable standard term policy

- Keep the policy active for the full term (20 or 30 years is most common)

- Collect the refund — if you're alive at the end and never filed a death benefit claim, the insurer returns your premiums as a lump sum

What Happens If You Cancel Early

The refund only applies if you hold the policy to completion. According to Progressive, canceling before the term ends typically means forfeiting all premiums paid. Western & Southern confirms the same: early cancellation or lapse usually results in no refund, or only a small prorated amount.

Missing payments carry the same risk. To receive the full refund, the policy must remain active and paid through the entire term.

Term Length Options

ROP is most commonly available on 20- and 30-year terms. State Farm and Mutual of Omaha, for example, explicitly offer ROP on 20- and 30-year level-premium term products. Some carriers also offer 10-year ROP options, though these are less common. Check individual carrier offerings before assuming a specific term length is available.

Pros and Cons of Return of Premium Life Insurance

Pros of ROP Life Insurance

With standard term life insurance, you pay premiums for 20 or 30 years and walk away with nothing if you outlive the policy. ROP changes that — every dollar you paid comes back to you at the end of the term.

Additional advantages:

- Tax-free refund — returned premiums don't exceed cost basis, so no income tax on the refund (consult a tax professional for your situation)

- Disciplined savings — the premium structure enforces consistent payments, which appeals to people who struggle to save on their own

- Financial flexibility at term end — the lump sum can supplement retirement income, pay off a mortgage, or cover major expenses

Cons of ROP Life Insurance

Higher premiums are the core trade-off. According to NerdWallet, ROP policies can cost 3x to 5x more than standard term coverage. Forbes and Policygenius report a range of 2x to 3x. A ValuePenguin example puts it plainly: a $500,000, 20-year standard term runs around $500/year, while the same policy with ROP runs $1,500/year.

Over 20 years, that gap adds up to $20,000 in extra premiums — paid to receive a $30,000 refund. The math works on paper, but it ignores opportunity cost.

"Buy term and invest the difference" is a well-worn counterargument — and a valid one. Those extra premium dollars, invested over 20 to 30 years in a low-cost index fund or retirement account, could compound well beyond the guaranteed refund. The ROP payout earns no growth and loses real value to inflation over that time. For people comfortable with some investment risk, redirecting the difference often produces better long-term returns.

How Much Does Return of Premium Life Insurance Cost?

Several factors drive ROP premium pricing:

- Age — older applicants pay more; starting younger locks in lower rates

- Gender — women typically pay less than men for the same coverage

- Health status — preferred health classifications reduce premiums significantly

- Coverage amount — a $1 million policy costs more than a $500,000 policy

- Term length — 30-year terms cost more than 20-year terms

Benchmarks From Real Carrier Data

The figures below are drawn from verified carrier data and give a practical snapshot of where ROP pricing lands relative to other product types:

| Product | Profile | Annual Premium |

|---|---|---|

| Standard 20-year term | 30-year-old male, $500K coverage | ~$215/year |

| ROP 20-year term | 30-year-old male nonsmoker, excellent health, $500K | ~$865/year |

| ROP 20-year term | 40-year-old male nonsmoker, excellent health, $500K | ~$1,510/year |

| Whole life | 30-year-old male, $500K coverage | ~$3,662/year |

Sources: NerdWallet (2026) for standard term and whole life; NerdWallet (2026) for ROP figures from Cincinnati Life, rates valid Dec. 9, 2025.

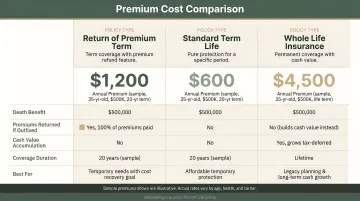

ROP falls in the middle of the cost spectrum: more expensive than standard term, but a fraction of whole life for the same coverage amount.

One important nuance on refund scope: some carriers, including Western & Southern, specify that the ROP rider refunds base policy premiums but may exclude premiums for substandard health ratings, other riders, or administrative fees. The refund is not always 100% of every dollar paid. Read the policy language carefully before assuming a full return.

ROP Life Insurance vs. Other Coverage Types

| Feature | Standard Term | ROP Term | Whole Life |

|---|---|---|---|

| Premium cost | Lowest | Mid-range | Highest |

| Coverage duration | Temporary | Temporary | Permanent |

| Refund at term end | None | Yes (if outlived) | N/A |

| Cash value | No | No | Yes |

| Death benefit | Yes | Yes | Yes |

The "Invest the Difference" Alternative

Some policyholders choose standard term and invest the monthly savings. A $500,000, 20-year standard term at $215/year versus ROP at $865/year leaves $650/year to invest. Over 20 years, that compounding can outperform the guaranteed refund — but only for those who invest consistently and can tolerate market risk.

ROP's advantage is certainty. The refund doesn't depend on market performance, discipline, or timing.

Universal Life ROP — A Different Structure

Some insurers offer ROP endorsements on universal life policies rather than term. Protective's Advantage Choice UL, for example, provides a no-cost ROP endorsement with access to 50% of premiums on the 20th policy anniversary and 100% on the 25th. This structure provides permanent coverage alongside exit points for refunds at defined milestones — a strong fit for anyone who wants lifelong coverage but also wants a defined off-ramp if circumstances change.

Who Should Consider Return of Premium Life Insurance?

The Ideal ROP Candidate

ROP works best for a specific profile:

- Financially stable — can reliably afford higher premiums for 20–30 years without risk of lapse

- Risk-averse — values guaranteed outcomes over potential investment gains

- Poor saver — benefits from the forced discipline of a structured premium commitment

- Coverage-dependent life stage — parents with young children, homeowners with long mortgages, or anyone who wants meaningful coverage now with a financial cushion later

Specific situations where ROP often makes sense:

- A 35-year-old parent who wants $500K in coverage through the child-rearing years and a lump sum available around retirement

- A homeowner who wants coverage aligned with a 30-year mortgage, knowing they'll receive a refund when the mortgage is paid off

- An individual who consistently fails to maintain separate savings or investment accounts

Who ROP Is NOT Right For

- Anyone on a tight budget who needs the most affordable coverage possible

- People with higher risk tolerance who are confident they'll invest the premium difference

- Anyone unlikely to sustain premium payments for the full term — early cancellation eliminates the refund

Getting the Comparison Right

ROP pricing and availability vary considerably across carriers. What one insurer offers at a competitive rate, another may price far higher — or not offer at all. Vellum Life Group works with 15+ A-rated carriers specifically so clients can compare ROP options side by side, rather than evaluating whatever a single carrier happens to offer.

Term length is just as important as carrier selection. Two quick benchmarks:

- Age 35, 20-year ROP: aligns naturally with peak earning and parenting years

- Age 50, 30-year ROP: changes both the math and the risk profile considerably

Getting both variables right — carrier and term — is where a comparison-based approach pays off.

Frequently Asked Questions

How much do you get back on a return of premium life insurance policy?

If you keep the policy active through the full term and never file a death benefit claim, you typically receive 100% of premiums paid as a lump sum. Some policies offer partial milestone refunds before term end; most don't. Early cancellation usually means no refund.

Is return of premium term life insurance worth it?

It depends on your priorities. For disciplined policyholders who value guaranteed premium recovery over investment growth, ROP can make sense. Those who can consistently invest the premium difference may come out ahead. Modeling both scenarios with an advisor gives you a clearer picture.

What happens if I cancel my return of premium policy early?

In most cases, you forfeit the refund entirely. Some policies offer a small prorated amount after several years, but this varies by carrier. Committing to the full term is essential; early cancellation is the single biggest risk of ROP.

Is the return of premium payout taxable?

Generally, no. Under IRS cost-basis rules, amounts received from a life insurance contract are taxable only to the extent they exceed premiums paid — so a straight premium refund carries no tax liability. Consult a tax professional for guidance on your specific circumstances.

How does return of premium life insurance compare to whole life insurance?

Both cost more than standard term, but for different reasons. Whole life provides permanent coverage and builds cash value over time. ROP term provides temporary coverage with a premium refund at the end. Whole life is generally the more expensive option and serves different long-term planning goals.

Can I add a return of premium rider to an existing life insurance policy?

This varies by carrier. Some insurers allow the rider to be added after issuance with additional underwriting; others require it to be elected at the time the policy is issued. Don't assume it can be added later — confirm with your carrier or advisor before your policy is finalized.