Pick the wrong one and you might spend decades overpaying for guarantees you didn't need — or find yourself with a policy that quietly erodes because it was never funded properly. Neither outcome is acceptable when your family's financial security is on the line.

This guide breaks down both policy types in plain terms: how they work, what they cost, who each one fits best, and a practical framework for making the right call.

Key Takeaways

- Both whole life and universal life are permanent policies — they don't expire and they build cash value, unlike term insurance.

- Whole life offers fixed premiums, a guaranteed death benefit, and predictable cash value growth.

- Universal life offers flexible premiums and an adjustable death benefit — but carries lapse risk if underfunded.

- Universal life typically costs less initially; whole life costs more but delivers stronger guarantees.

- Your best fit depends on whether you prioritize predictability and guarantees, or flexibility and lower starting premiums.

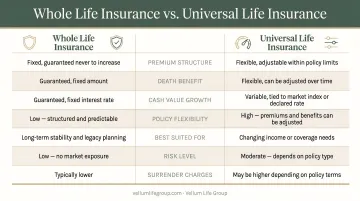

Whole Life vs. Universal Life Insurance: Quick Comparison

| Feature | Whole Life | Universal Life |

|---|---|---|

| Premium Structure | Fixed — never changes | Flexible — adjust within limits |

| Death Benefit | Guaranteed, level | Adjustable (up or down) |

| Cash Value Growth | Guaranteed rate (e.g., 2.00%–3.75% per MassMutual) | Declared rate with a minimum floor (typically 2%) |

| Cost | Higher premiums | Lower initial premiums |

| Management Required | Minimal — no monitoring needed once issued | Active monitoring needed |

| Risk Level | Low — fully guaranteed | Moderate — can lapse if underfunded |

Both policy types serve the same core purpose: lifetime protection with a savings component that grows tax-deferred. Where they diverge is in structure, guarantees, and the level of engagement they demand from you.

This comparison covers standard whole life and traditional (current-interest) universal life. Universal life also comes in indexed (IUL) and variable (VUL) forms — those are addressed in the universal life section below.

What Is Whole Life Insurance?

Whole life is a permanent policy built on guarantees. The premium is fixed at issue, the death benefit is locked in, and the cash value grows at a guaranteed rate set by the insurer, regardless of market conditions or interest rate changes in any given year.

Guardian confirms this in their product materials: whole life offers guaranteed level premiums, a guaranteed death benefit, and guaranteed cash value growth, scheduled to equal the face amount at age 100 or 121 (subject to policy terms).

How the Cash Value Works

Cash value in a whole life policy grows tax-deferred at a fixed rate. MassMutual's whole life series, for example, carries guaranteed interest rates ranging from 2.00% to 3.75% depending on the policy.

A few things to know:

- You can borrow against cash value through a policy loan with no credit check or approval process

- Cash value cannot fall below the guaranteed floor, protecting your accumulation

- Policy loans reduce the death benefit until repaid, so they should be used deliberately

- Overfunding the policy can trigger Modified Endowment Contract (MEC) rules under IRC Section 7702A, changing how distributions are taxed

The Dividend Advantage

Some whole life policies issued by mutual insurers pay annual dividends. These aren't guaranteed, but many mutual insurers have paid them consistently for decades. In 2026, MassMutual announced a dividend interest rate of 6.60% and Guardian announced 6.25%. New York Life announced a record $2.78 billion 2026 dividend payout, marking its 172nd consecutive annual dividend.

Policyholders can typically use dividends to:

- Reduce out-of-pocket premiums

- Accumulate additional cash value

- Purchase paid-up additions (more coverage)

Who Benefits Most from Whole Life Insurance

The ideal whole life buyer wants certainty, not flexibility. Specific fits include:

- Parents of lifelong dependents who need coverage that will never lapse, regardless of health changes — common for families with special needs children

- Estate planning clients who require a known, reliable death benefit to cover estate taxes, equalize inheritance, or transfer wealth

- Estate planners using life insurance where a guaranteed, predictable payout is non-negotiable

- Anyone who wants autopilot protection with no annual reviews, no funding calculations, and no risk of underfunding

The 2026 federal estate tax basic exclusion amount is $15 million per IRS guidance. For estates approaching that threshold, a properly structured whole life policy held in an irrevocable life insurance trust (ILIT) can keep proceeds out of the taxable estate entirely — a meaningful advantage that requires the certainty only whole life provides.

What Is Universal Life Insurance?

Universal life (UL) is a permanent policy that trades some of whole life's guarantees for flexibility. You can adjust your premium payments within limits, modify your death benefit over time, and tailor your coverage to match your life as it changes.

The cash value grows based on an interest rate declared by the insurer, subject to a guaranteed minimum floor. Both Guardian and Mutual of Omaha, for example, guarantee their UL products will never credit less than 2% annually.

How Premium Flexibility Works — and Where the Risk Lives

The flexibility mechanism works like this: your premium payments go into the cash value account, from which the insurer deducts the monthly cost of insurance (COI). You can:

- Pay more than the minimum to build cash value faster

- Pay only the minimum needed to cover the COI

- Skip payments entirely if the cash value is large enough to cover the COI

That last option is where things get dangerous. If cash value depletes — due to low interest credits, rising COI charges as you age, or simply underfunding over time — the policy lapses. Research from SOA/LIMRA found an overall UL lapse rate of 5.3% across all policy years studied, compared to a 2.9% annual lapse rate for whole life policies.

Maryland's insurance regulator warns explicitly: if you don't adjust your death benefit or increase payments when interest rates fall or COI rises, your policy will lapse when cash value can no longer cover insurance costs.

Adjustable Death Benefit

That lapse risk connects directly to one of UL's most useful tools: the adjustable death benefit. Unlike whole life, UL lets you increase or decrease your coverage over time. Reducing it — once your mortgage is paid off or your children are financially independent — lowers your COI and extends how long your cash value lasts. Increasing coverage typically requires new underwriting.

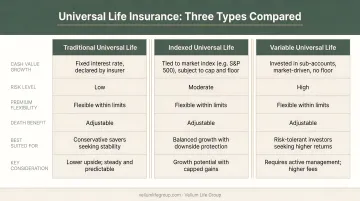

Types of Universal Life Insurance

Universal life comes in three main forms:

- Traditional/Current-Interest UL — The most common form. Cash value grows at an insurer-declared interest rate with a guaranteed minimum floor.

- Indexed UL (IUL) — Growth is tied to a market index like the S&P 500, with a cap on gains and a floor protecting against losses. Regulated as life insurance, not a security.

- Variable UL (VUL) — Cash value is invested directly in market sub-accounts, offering higher growth potential but also direct market risk. VUL products are treated as securities and are subject to federal securities oversight alongside insurance regulation.

Who Benefits Most from Universal Life Insurance

Universal life fits a different profile than whole life:

- Variable income earners (freelancers, commission-based professionals, and others with fluctuating income) who need the ability to reduce payments in lean years

- Growing families whose coverage needs will shrink over time as debts are paid off and children become independent

- Cost-conscious buyers who want permanent coverage but need lower initial premiums than whole life offers

- Financially engaged individuals comfortable reviewing their policy annually to confirm it's adequately funded

The trade-off is real: as you age, the monthly cost of insurance inside a UL policy rises. An underfunded policy that looks fine at 45 can be in trouble at 65. Annual reviews aren't optional — they're how you keep the policy alive.

Whole Life vs. Universal Life: Which Is Right for You?

There's no universally correct answer here. The right policy depends on your income stability, how much policy management you're willing to do, whether you prioritize guarantees or flexibility, and what you're ultimately trying to accomplish.

Choose Whole Life If…

- You want fixed premiums you can budget around for the next 30+ years without surprises

- Your primary goal is leaving a guaranteed inheritance or covering estate costs — you need to know the death benefit will be there, in a specific amount

- You have a lifelong dependent (such as a child with special needs) whose financial security depends on your policy never lapsing

- You'd rather your policy run on autopilot — no annual reviews, no funding calculations, no risk of underfunding

Choose Universal Life If…

- Your income fluctuates and you need the ability to reduce or skip premiums in tighter years

- Your life insurance needs will shrink over time as your mortgage disappears and your kids become independent

- You want the lowest initial premium available for permanent coverage

- You're comfortable reviewing your policy at least annually to confirm the cash value stays healthy

A Note on Working With an Advisor

The gap between the best and worst version of either policy type often comes down to the carrier, not the product category. Forbes Advisor notes that whole life is significantly more expensive than universal life because it provides fixed premiums, guaranteed death benefit, and guaranteed cash value growth — but costs vary considerably across insurers.

Vellum Life Group works with 10+ A-rated carriers — including Mutual of Omaha, Transamerica, Kansas City Life, Ameritas, and others — to compare options across the market rather than defaulting to a single carrier's product. Eva Ikonomakos offers free, no-obligation consultations and typically responds within 24 hours. If you're weighing these two options, a single conversation can clarify which fits your situation — and which carriers offer the most competitive terms for your age, health, and goals.

Conclusion

Neither whole life nor universal life is the better product in the abstract. Whole life suits people who need guaranteed, predictable protection they'll never have to think about again. Universal life suits those whose financial lives are still shifting and who are willing to stay engaged with their coverage over time. The right fit depends entirely on your actual circumstances, not on which product sounds more appealing in theory.

Choosing between these two products is one of the more consequential financial decisions you'll make for your family. Selecting the wrong policy type, an insufficient coverage amount, or a carrier that doesn't fit your situation can cost significantly more over decades and leave your family with less protection than you intended.

That's where working with an independent advisor makes a real difference. Vellum Life Group offers free, no-obligation consultations to help you think through exactly this decision. Schedule yours today and find the right policy from the right carrier for where you are right now, and where you're headed.

Frequently Asked Questions

What are the advantages and disadvantages of universal life insurance?

The main advantages are premium flexibility, an adjustable death benefit, and lower initial costs compared to whole life. The drawbacks are that the death benefit isn't guaranteed the way whole life's is, the policy can lapse if the cash value is depleted, and it requires regular monitoring — especially as the cost of insurance rises with age.

How much does a $1,000,000 whole life insurance policy cost per month?

Costs vary significantly by age, gender, and health. According to Aflac's 2026 data, a healthy nonsmoking 30-year-old pays approximately $815/month (male) or $783/month (female) for $1M in whole life coverage. By age 40, those figures rise to roughly $1,115 and $1,065 respectively. For a quote tailored to your age and health profile, an independent advisor like Vellum Life Group can compare rates across multiple carriers.

Can you switch from universal life to whole life insurance?

Yes — through a 1035 exchange under IRC Section 1035, you can transfer cash value from a UL policy to a whole life policy without triggering a taxable event, provided it's properly structured. New underwriting is typically required, and your insurability at the time of the exchange will affect the outcome.

Which is better for estate planning: whole life or universal life?

Whole life is generally the stronger estate planning tool. Its guaranteed death benefit gives beneficiaries and planners a fixed, reliable number — critical for inheritance equalization or covering estate tax obligations. Universal life's adjustable benefit introduces uncertainty that can complicate long-term plans.

Does universal life insurance build cash value like whole life?

Yes, but not in the same way. Universal life cash value growth depends on the insurer's declared interest rate, funding consistency, and rising insurance costs over time. Whole life's cash value grows on a guaranteed schedule regardless of those variables.

What happens if I stop paying premiums on a universal life policy?

If the cash value is large enough to cover the monthly cost of insurance, the policy can continue temporarily without premium payments. But if the cash value runs out — which becomes more likely as the cost of insurance rises with age — the policy will lapse and coverage ends. This is why regular policy reviews are essential for UL policyholders.