Here's the reassurance upfront: family history is one factor in underwriting, not the deciding one. Your own health, age, and lifestyle carry more weight. Having a parent who had a heart attack does not automatically push you into a higher rate class — the details matter enormously.

This article covers which conditions flag underwriters, how family history is actually evaluated, what it could realistically cost you, and what to do if you want the most favorable rate possible.

Key Takeaways

- Family history signals genetic risk, but your personal health profile carries more weight in underwriting

- Age of diagnosis, number of relatives affected, and how closely related they are all shape how much weight underwriters apply

- Family history rarely causes outright denial — it more often moves applicants to a different rate class with a higher premium

- Underwriting guidelines differ widely by carrier — comparing multiple carriers can meaningfully lower your premium

Why Life Insurance Companies Ask About Your Family History

Life insurance underwriting is fundamentally a mortality-risk calculation. According to the NAIC, insurers use application data, medical records, lab results, and other sources to classify risk accurately — and family history feeds directly into that model.

Hereditary conditions signal which illnesses you're statistically more likely to develop — giving underwriters direct input for their risk models. As the ACLI explains, this risk classification process is designed to price policies in line with actual risk and prevent lower-risk policyholders from subsidizing higher-risk ones.

In practice, three things shape how family history is applied:

- Patterns matter more than isolated incidents — one diagnosis in a single family member carries far less weight than the same condition appearing across multiple generations.

- Risk classification affects pricing, not just eligibility. A higher perceived risk typically moves an applicant from a preferred rate class to standard or substandard, which means a higher monthly premium.

- Family history is one input among many. The ACLI explicitly notes that genetic or hereditary information is not necessarily more important than other health or lifestyle factors in your medical record.

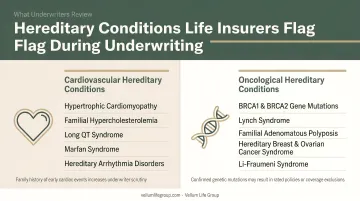

Which Health Conditions in Your Family History Can Affect Your Premiums

Underwriters focus on conditions with a meaningful genetic or hereditary component — not every illness a family member has ever had.

Conditions Most Commonly Flagged

These are the conditions insurers most frequently ask about, with strong support across major carriers and consumer-facing sources:

- Heart disease — including heart attack and cardiomyopathy

- Cancer — breast, colon, lung, ovarian, and prostate are the most cited types

- Type 2 diabetes

- Kidney disease

- Stroke

Additional Hereditary Conditions That May Be Reviewed

Depending on the carrier, underwriters may also consider:

- Alzheimer's disease

- Huntington's disease

- ALS (amyotrophic lateral sclerosis)

- Sickle cell anemia

- Epilepsy and cystic fibrosis (carrier-specific)

- Parkinson's disease and multiple sclerosis (varies by carrier)

What Generally Won't Affect Your Premiums

- Accidental injuries with no hereditary component

- Gender-irrelevant conditions (a female applicant whose father had prostate cancer will generally not see her premiums affected)

- Conditions diagnosed late in life with no broader family pattern

Knowing which conditions matter is only part of the picture — whose history gets reviewed matters just as much.

Which Relatives Count

Most insurers focus on biological parents and full siblings. Some carriers ask about grandparents, but the primary weight is placed on first-degree relatives — particularly for conditions diagnosed at a younger age.

How Underwriters Evaluate Your Family Medical History

Not all family health history is weighted the same. Four specific factors determine how much influence it has on your premium — and understanding them can help you anticipate what underwriters will see.

Age of Diagnosis

Age of diagnosis carries more underwriting weight than almost anything else. An early diagnosis — typically before age 60 — is treated far more seriously than one that occurs late in life. Legal & General America's underwriting field guide, for example, uses cardiovascular death before age 60 as a threshold for preferred-class eligibility. A parent who had a heart attack at 48 is treated very differently from one diagnosed with heart disease at 76.

Pattern vs. Isolated Event

One sibling with cancer reads differently than a parent, sibling, and grandparent all diagnosed with the same condition. Underwriters look for clustering of the same or related conditions across generations. A single occurrence in the family is far less concerning than a multi-generational pattern.

Gender Relevance

Underwriters apply gender filters. A female applicant whose father had prostate cancer will typically not see her premiums affected, since the condition is sex-specific. The same logic applies to other gender-linked conditions.

Your Current Health Can Counterbalance Family History

If a parent developed Type 2 diabetes linked to obesity, but you maintain a healthy weight with clean lab results, the underwriter may factor in that family history less heavily. Your personal health profile remains the dominant factor — which means strong controllable markers like BMI, blood pressure, and glucose levels can genuinely improve your rate class.

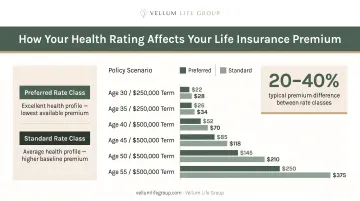

How Much More Could You Pay?

The impact of family history on premiums is expressed through rate classes: preferred plus, preferred, standard plus, standard, and substandard (table-rated). A concerning family history may move an applicant down one or two classes.

To illustrate what that shift costs, NerdWallet's 2026 rate data for a $500,000, 20-year term policy shows the following for nonsmoking applicants at age 40:

| Applicant | Preferred | Standard | Annual Difference |

|---|---|---|---|

| 40-year-old woman | $336/year | $433/year | +$97/year (~29%) |

| 40-year-old man | $405/year | $530/year | +$125/year (~31%) |

Family history alone doesn't drive these differences — any underwriting factor that moves someone from Preferred to Standard produces a similar shift. That said, these numbers give a realistic sense of what's at stake when your rate class changes.

Three things that often surprise applicants:

- The premium impact tends to be more significant for younger applicants. Older applicants (especially over 60) are assessed more heavily on their own current health record, which is now more informative than family history.

- Family history alone rarely leads to denial. Denial is more common when family history combines with personal health issues, high-risk lifestyle factors, or multiple hereditary conditions showing early patterns.

- Substandard (table-rated) policies use a letter or number system to indicate the percentage above the standard premium an applicant would pay — so even if you land outside the standard tier, coverage is still typically available.

What If You Don't Know Your Family's Medical History?

Being adopted, estranged from biological family, or simply lacking medical records is a common situation. Insurers handle it consistently: if you genuinely don't know, they will typically note the gap in your profile without penalizing you for it. In practice, unknown biological family history is not held against adopted applicants — the gap is acknowledged, not penalized.

That said, being unaware of family history is entirely different from knowingly omitting it. According to the Texas Department of Insurance, if an insured dies during the two-year contestable period and the insurer discovers undisclosed or inaccurate information, it may deny the death benefit claim. That denial falls on your beneficiaries, not you.

Practical guidance:

- Always be upfront with your advisor if you lack family history information — do not guess or fabricate answers

- If you're still in contact with biological relatives, gathering this information before applying pays off — not just for your application, but for your own preventative health planning

- If you have no access to biological family history, say exactly that on the application

How to Get the Best Life Insurance Rates Despite Your Family History

Shop Across Multiple Carriers

For applicants with complex family health backgrounds, shopping across multiple carriers is the single most impactful move you can make. Underwriting guidelines vary significantly across insurers — one carrier may offer Preferred Plus for a family history of heart disease while another declines the same applicant profile entirely. Because no two carriers evaluate family history the same way, the carrier you apply with matters as much as your health profile itself.

Strengthen Your Personal Health Markers

Since your personal health profile carries more underwriting weight than family history, documenting strong health indicators before you apply can improve outcomes. Underwriters respond favorably to:

- Healthy BMI

- Normal blood pressure

- Clean lab results (cholesterol, blood glucose)

- Non-smoker status

- Regular preventative care and checkups

Work With an Independent Advisor

Working with an independent advisor like Eva Ikonomakos at Vellum Life Group makes a concrete difference here. Rather than being locked into one carrier's assessment of your family history, Eva can match your application to the carrier whose underwriting guidelines best fit your specific profile.

Key advantages of working with an independent advisor:

- Access to 10+ A-rated carriers rather than a single insurer's guidelines

- Carrier matching based on your unique health and family history profile

- Options from carriers that specialize in higher-risk applicants

This means better outcomes are often available than a single-carrier experience would suggest.

Book a free consultation to explore your options at calendly.com/eva-ikonomakos/30min or reach Eva directly at 917-363-3554.

Frequently Asked Questions

Does life insurance ask about family history?

Yes. Most medically underwritten life insurance policies ask whether parents or siblings have been diagnosed with conditions like cancer, heart disease, diabetes, or kidney disease — typically focusing on diagnoses before age 60 or 70. The exact questions vary by carrier and product.

Does life insurance cover Parkinson's disease in your family history?

A family history of Parkinson's may be reviewed during underwriting but won't automatically disqualify you. If you've been personally diagnosed, your own health profile takes precedence — and options like guaranteed-issue or final expense coverage may still be available.

Which family members' medical history do life insurers consider?

Most insurers focus on biological parents and full siblings, with some carriers also asking about grandparents. Underwriting weight is heaviest when conditions were diagnosed before age 60.

Will a family history of cancer automatically raise my premiums?

Not automatically. The type of cancer, age at diagnosis, number of relatives affected, and your own health all factor in. One late-life diagnosis in a parent carries far less weight than multiple early-onset cases across immediate family.

Can I be denied life insurance based solely on family history?

Denial based on family history alone is rare. Family history more commonly affects your rate class and premium rather than your eligibility — particularly when your personal health profile is otherwise strong.

How far back does family medical history need to go?

Most applications ask only about immediate family — parents and siblings. Extended family and multiple generations back are generally not required. The focus is on first-degree biological relatives and conditions with known hereditary components.