Introduction

When you're a single parent, every financial decision lands on your shoulders alone. No backup income, no second earner to lean on. Your plan either protects your children or it doesn't.

That reality makes life insurance one of the most consequential decisions a single parent can make. Yet according to LIMRA and Life Happens' 2023 Insurance Barometer, 59% of single mothers said they need more life insurance — representing 5 million households without adequate coverage.

For most of those households, cost concerns and not knowing where to start are the main reasons for delay. This guide addresses both directly. You'll learn what type of policy fits your situation, how much coverage to buy, and how to structure it so your children are protected in practice, not just on paper.

Key Takeaways

- Single parents carry the full financial load — one income, no backup if something goes wrong

- Term life insurance offers meaningful coverage at a price a single income can handle

- Coverage should include mortgage debt, childcare, and education costs — not income alone

- Minor children cannot legally receive life insurance proceeds directly — a trust or adult trustee is required

- Buying coverage younger secures lower rates that hold even if your health changes later

Why Single Parents Need Life Insurance More Than Anyone

In a two-parent household, losing one income is devastating. In a single-parent household, there's no second income to absorb the blow. Housing, groceries, childcare, school costs, healthcare — one person funds all of it. Without a plan, none of it continues.

That financial exposure is more common than most people realize. U.S. Census Bureau 2023 data shows roughly 20 million children — about 27% of all children under 18 — live with one parent. That's a massive share of American families operating without a financial safety net.

What a Single Parent's Income Actually Covers

A single parent's paycheck typically funds:

- Rent or mortgage payments

- Full childcare costs (national average: $11,582 per year, per Child Care Aware of America)

- Groceries, transportation, and healthcare

- School supplies, activities, and clothing

- Emergency expenses with no other household income to draw from

Life insurance replaces all of this. It doesn't just replace a salary — it covers every cost involved in raising your child to adulthood.

Different Paths, Same Protection Goal

Single parents arrive at their situation differently — widowhood, divorce, or choosing parenthood alone. The insurance considerations differ slightly by path:

- Recently divorced: You may need to replace a joint policy or update a former spouse who's still named as beneficiary

- Widowed: Existing coverage may be inadequate now that you're the sole provider; review coverage amounts

- Never married: Starting from zero — coverage is an immediate priority

The path varies, but the coverage need doesn't. The right policy keeps your children financially stable — on your terms, not anyone else's.

Term vs. Permanent: What Type of Life Insurance Works Best

The core question is simple — how long do you need coverage? For most single parents, the answer is: until the youngest child is financially independent. That timeline points directly to term life insurance.

Term Life: The Right Starting Point for Most Single Parents

Term life insurance covers you for a set period — typically 10, 20, or 30 years — and pays a death benefit if you pass away during that window. It does one thing extremely well: it provides maximum coverage at the lowest cost.

The price difference compared to permanent insurance is significant. Based on 2024 Policygenius data, a $500,000 20-year term policy averages around $26/month for a healthy applicant. A whole life policy with equivalent coverage runs approximately $440/month — nearly 17 times more expensive. On a single income, that gap matters.

Choosing the right term length:

- Align the term with the year your youngest child reaches financial independence (typically 18–22)

- If you have a mortgage, consider matching the payoff timeline

- Parents with young children often benefit from 20- or 30-year terms; a parent of teenagers may find a 10- or 15-year term sufficient

When Permanent Life Insurance Makes Sense

Permanent coverage (whole or universal life) is worth considering in specific circumstances:

- A child with a lifelong disability who will require ongoing financial support into adulthood

- Substantial estate planning goals, such as leaving a structured inheritance or funding a special needs trust

For the average single parent focused on protecting dependents through childhood, the higher premiums of permanent policies rarely make sense on a single income. For most single parents, term life is the right starting point — and often the most financially sound one.

Policy Add-Ons Worth Knowing About

Two riders stand out for single parents:

- Disability income rider: Replaces a portion of your income (typically 50–70%) if illness or injury prevents you from working — protecting your family while you're still alive

- Critical illness rider: Provides a lump-sum payout if you're diagnosed with cancer, heart attack, stroke, or other covered conditions

These address the financial risk of serious illness, not just death. For a single parent with no backup income, a serious diagnosis without coverage can be just as financially devastating as death. When exploring term policies, ask about which carriers include these riders — availability and cost vary significantly between them.

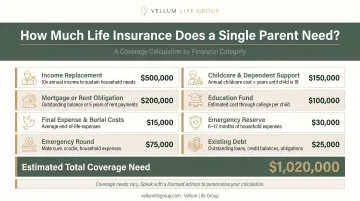

How Much Coverage Does a Single Parent Actually Need?

Life Happens recommends 10 to 15 times gross annual income as a starting estimate. For single parents, treat that as a floor. With no second income to supplement, undercovering leaves real gaps.

Building Your Coverage Calculation

Add up each of these categories:

| Category | What to Include |

|---|---|

| Income replacement | Annual income × years until youngest child is independent |

| Mortgage or rent | Outstanding balance or years of rent remaining |

| Other debts | Car loans, personal loans, credit cards |

| Childcare | Annual cost × remaining dependent years |

| Education | Estimated college costs ($11,950–$45,000/year depending on school type) |

| Final expenses | National median funeral cost: $8,300 |

Then subtract existing savings and any current life insurance you already carry. The gap is your target coverage number.

Balancing Coverage With a Single-Income Budget

Full coverage isn't always immediately affordable — and some coverage is always better than none. Practical strategies:

- Start with what you can afford and add a second policy as income grows

- Choose a shorter initial term to lower premiums, then reassess when circumstances change

- Shop multiple carriers through an independent advisor — quotes vary more than most people expect

That last point matters more than it might seem. Vellum Life Group works with 15+ A-rated carriers, so a single parent sees real pricing across the market — not just what one company offers. Many policies are also approved the same day or within a few days, which means coverage can be in place before the week is out.

Beneficiaries, Guardians, and the Estate Basics You Can't Skip

Life insurance doesn't protect your children automatically. It protects them only if you've set up the legal structure correctly. Three pieces must work together: a beneficiary designation, a guardian appointment, and a will.

The Minor Beneficiary Problem

Minors cannot legally receive life insurance proceeds directly. If you name a minor child as your beneficiary, the payout gets tied up in court — a judge appoints a guardian of the estate, the process takes time and money, and control over those funds may not go to the person you'd have chosen.

There are two cleaner options:

- Name a trusted adult to manage the funds on the child's behalf until adulthood

- Establish a revocable living trust and name the trust as beneficiary — this lets you specify exactly when and how your child accesses the money (at 25 rather than 18, for example)

Always name a contingent beneficiary in case the primary beneficiary can't accept the payout.

Coordinating With Your Will

Once your beneficiary structure is in place, your will needs to align with it — because these two documents serve different functions:

- Will: Determines who raises your child (legal guardian designation)

- Life insurance: Determines how your child is financially supported

The NAIC confirms that a will does not override a life insurance beneficiary designation. If your ex-spouse is still named as beneficiary on your policy, they receive the proceeds regardless of what your will says.

Review both documents after any major life change: remarriage, additional children, income change, or a child reaching adulthood. According to AARP, only about 4 in 10 American adults have a will or living trust — which means most single parents are leaving this critical piece unaddressed.

How Vellum Life Group Helps Single Parents Get This Right

Choosing the right coverage amount, comparing carriers, and structuring your beneficiary correctly is genuinely complex — especially without a partner to pressure-test your thinking. Vellum Life Group, founded by Eva Ikonomakos, is built specifically for this kind of one-on-one guidance.

Eva brings over 15 years of experience across financial services, healthcare, and international business. She's helped protect 500+ families and placed more than $50 million in coverage — with a process designed to be pressure-free and clear of jargon. For single parents, that combination of clarity and access to multiple carriers means you're not guessing — you're comparing real options on your terms.

What working with Vellum looks like in practice:

- Free initial call focused on your situation — dependents, income, debts, goals — before any carrier is mentioned

- Side-by-side access to 15+ A-rated carriers including Mutual of Omaha, Transamerica, Corebridge Financial, and Ameritas, so you see real market rates, not a single company's pitch

- Same-day or next-few-days approvals on many policies; medical exam cases typically wrap in 2–4 weeks

- Ongoing support after the policy is placed: annual reviews, beneficiary updates, coverage adjustments as your income grows or your children age out of dependency

Single parents' lives shift in ways that matter to coverage: new jobs, remarriage, a child turning 18. Vellum builds annual check-ins into the relationship so your policy stays current without you having to track it down yourself.

To get started with a free, no-obligation consultation, contact Eva at 917-363-3554 or info@vellumlifegroup.com.

Frequently Asked Questions

Why do single parents need life insurance?

Single parents are both the sole income source and primary caregiver for their children — there is no financial backup if they pass away unexpectedly. Life insurance ensures children can maintain housing, childcare, and daily needs even without that income.

How much life insurance does a single parent need?

Life Happens recommends starting at 10–15 times gross annual income, but single parents should also factor in outstanding mortgage debt, remaining childcare costs, and projected education expenses. Subtract existing savings to find the actual coverage gap.

Who should I name as beneficiary if my children are minors?

Minors cannot directly receive life insurance payouts — courts will intervene and appoint an estate guardian. Name a trusted adult or a revocable trust as beneficiary to ensure funds are managed on your child's behalf until they reach adulthood.

Will life insurance pay out for cirrhosis?

A death resulting from cirrhosis can be a covered claim under most policies, but the severity of the condition at application affects both eligibility and premium rate. Full disclosure during underwriting is essential. Working with an advisor who shops multiple carriers gives you the best chance of finding coverage at a reasonable rate.

Does Lexapro affect life insurance?

Taking Lexapro or other antidepressants does not automatically disqualify you. Insurers assess the underlying condition, treatment stability, and history — many applicants on SSRIs qualify for standard or slightly higher rates, particularly when the condition is well-managed.

Can I get life insurance with lupus?

The Lupus Foundation of America confirms that coverage is possible, though premiums and eligibility depend on disease severity, organ involvement, and current treatment status. Working with an advisor who has access to multiple carriers, including those that specialize in higher-risk applicants, expands your options considerably.