That distinction matters because 42% of U.S. adults — roughly 102 million people — need new or additional life insurance, according to LIMRA's 2024 data. Families often end up underinsured not because they skipped coverage, but because they chose a cheaper structure without understanding the trade-offs.

This article breaks down each approach — definitions, a direct cost comparison, and a situational guide — so you can determine what actually makes sense for your household.

Key Takeaways

- "Family life insurance" is not a single product; it's a planning label for individual policies, riders, or joint coverage

- Individual term life policies typically deliver the best value per dollar for healthy adults

- Spouse riders cost less upfront but often provide significantly less coverage than a standalone policy

- The cheapest option and the best-value option are frequently not the same thing

- Comparing quotes across multiple carriers is the only reliable way to find your household's lowest rate

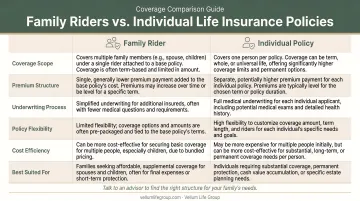

Family vs. Individual Life Insurance: Quick Comparison

| Factor | Family Coverage (Riders/Joint) | Individual Policies for Each Person |

|---|---|---|

| Monthly Cost | Lower single premium | Higher combined premium |

| Coverage Flexibility | Limited; tied to primary policy | Full flexibility per person |

| Portability | Rider ends with primary policy | Owned by insured; portable |

| Underwriting | Based on primary insured | Each person assessed separately |

| Coverage Amount | Often capped or limited | Up to full face value per person |

| Best For | Tight budgets; estate planning | Income replacement; long-term security |

"Family life insurance" is not a standardized product. Structure and cost vary by insurer, rider type, and each family member's health profile. The figures above reflect general patterns — your actual quotes will depend on your specific situation.

What Is "Family Life Insurance"?

"Family life insurance" is a consumer term, not a regulated product category. The Insurance Information Institute classifies life insurance by product type — term, whole, universal, variable — not by family versus individual use. In practice, "family coverage" refers to any combination of:

- Spouse term riders added to a primary policy

- Child riders covering eligible children under one add-on premium

- Joint life policies (first-to-die or second-to-die)

- Employer group plans bundling basic coverage for a household

Each option works differently — here's what to know before assuming any of them covers your family adequately.

Spouse Term Riders

A spouse rider attaches to the primary insured's policy and pays a benefit if the spouse dies while the rider is active. The appeal is simplicity — one application, one insurer. The trade-off is that the rider typically expires when the primary policy ends or the spouse reaches a specified age, and coverage amounts are often modest compared to what a standalone individual policy provides.

No industry-wide standard for rider caps exists across carriers, so coverage limits vary. Before assuming a spouse rider provides adequate protection, verify the actual death benefit — it may be far less than your spouse's income replacement need.

Child Riders

A child rider covers all eligible children under a single flat add-on premium. According to Policygenius, a $10,000 child rider can cost as little as $4.20/month, with death benefits typically ranging from $500 to $100,000.

Child riders are rarely a primary reason to buy life insurance. They're most useful for covering final expenses or locking in a child's future insurability — coverage can often be converted to a permanent policy later in life, sometimes up to 5x the original amount.

Joint Life Insurance

Joint policies cover two people under one contract:

- First-to-die: Pays the death benefit when the first spouse dies — useful for income replacement or debt payoff

- Second-to-die (survivorship): Pays only after both spouses die — primarily used for estate planning, inheritance taxes, or special-needs planning

Most couples today choose separate individual policies. Joint policies serve a narrower purpose — estate planning, special-needs trusts, or situations where two insureds together are more cost-effective than two standalone applications.

What Is Individual Life Insurance?

Individual life insurance is a standalone policy underwritten for one specific person. It's the most common form of life insurance in the U.S., with **45.6% of households owning at least one term life policy** as of 2022, per ACLI data.

Each applicant is assessed on their own age, health, lifestyle, and desired coverage amount. A healthy non-smoking 35-year-old qualifies for their own rate with no connection to a spouse's health profile. That separation matters most when two spouses have different health histories.

Those differences in underwriting also show up in price — and the gap between policy types is just as significant.

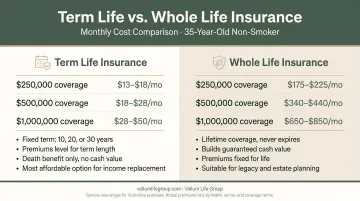

Term vs. Permanent: Cost Reality

The two most common types families use:

- Term life: Fixed premiums for a set period (10, 20, or 30 years); lowest cost; most used for income replacement

- Permanent life (whole or universal): Higher premiums; builds cash value; used for lifelong coverage or legacy planning

According to MoneyGeek's 2026 rate data, here's what a healthy 35-year-old non-smoker pays:

| Policy Type | Female | Male |

|---|---|---|

| $500K 20-year term | $37/month | $47/month |

| $500K whole life | $380/month | $451/month |

For most families focused on income replacement during working years, term life delivers the most protection per dollar.

Portability: A Key Advantage

Individual policies are owned by the insured. They don't end when you change plans, go through a divorce, or outlive a spouse's policy. Group life plans and spouse riders don't offer that security — group coverage typically disappears when the group plan lapses.

That's worth keeping in mind when comparing policy structures. Vellum Life Group offers term coverage in 10, 20, and 30-year increments, and many policies are approved the same day or within a few days based on health profile and carrier.

Family vs. Individual Life Insurance: Which Costs Less?

For most healthy couples, two individual term policies cost more per month than a primary policy with a spouse rider — but they also deliver significantly more protection. Whether that tradeoff makes sense depends on your coverage needs and health profile.

The Real Cost Comparison

Using MoneyGeek's verified age-35 rates, here's what two common structures actually cost for a healthy non-smoking couple:

| Structure | Monthly Premium | Combined Death Benefit |

|---|---|---|

| Two individual $500K 20-year term policies | ~$84/month total ($37 + $47) | $1,000,000 |

| One primary policy + spouse rider | Lower single premium | Limited (rider amount varies by carrier) |

The combined premium for two individual policies is $84/month, a source-backed figure. Spouse rider pricing varies too much by carrier to cite a standard number, but the coverage delivered is meaningfully less than two full $500K policies.

The "Hidden Cost" of Riders

A lower monthly premium can mask a coverage gap. If a spouse rider provides $150,000 in coverage but the spouse's actual income replacement need is $400,000+, the family is underinsured — paying for coverage that wouldn't maintain their lifestyle.

This matters because, per LIMRA, 47% of parents with minor children say they don't have enough coverage, compared to 41% of the general population. Choosing a cheaper structure is one reason why.

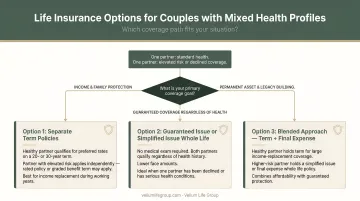

When Health Differences Change the Math

If one spouse has a significant health condition, the situation gets more nuanced:

- An individual policy for the healthier spouse proceeds through standard underwriting at their own favorable rate — the other spouse's condition doesn't affect it

- A rider on the primary policy typically prices coverage at a flat rate or may restrict coverage based on the rider applicant's health

- A separate individual policy for the higher-risk spouse may require working with carriers that specialize in higher-risk applicants

This is where working with an independent advisor matters. At Vellum Life Group, Eva Ikonomakos works with 15+ A-rated carriers, including some that specialize in higher-risk applicants, so families with mixed health profiles can often find better options than a one-size-fits-all rider would provide.

The Cost Rule of Thumb

For most two-adult households where both spouses are in good health: two individual term life policies will cost more in total monthly premium but deliver substantially more protection per dollar. Before choosing based on premium alone, run the numbers on total coverage delivered — that's where the real comparison lives.

Situational Recommendations: Which Approach Is Right for You?

Choose Individual Policies If...

- Both adults are in good health and qualify for standard or preferred underwriting

- Each spouse has financial dependents or contributes meaningfully to household finances

- Long-term coverage security matters — you want coverage that survives job changes, divorce, or a spouse's death

- You're concerned about what happens to a rider if the primary policyholder dies first

Consider a Rider or Joint Approach If...

- Budget is very tight and some coverage is better than none while you build toward separate policies

- One spouse's health makes individual underwriting prohibitive or cost-prohibitive

- The primary goal is estate planning or legacy transfer, not income replacement after the first death

Not Sure Which Fits Your Household?

An independent advisor can run both structures side by side across multiple carriers — so you see exactly what each option costs and covers before committing. At Vellum Life Group, Eva Ikonomakos does exactly that: comparing individual and joint approaches to find the right coverage at the lowest total cost for your household. The consultation is free and no-obligation.

Conclusion

"Which is cheaper?" depends on how you define value. A rider or joint policy may carry a lower monthly premium. But for most families, individual term policies deliver more coverage, more portability, and more long-term security per dollar spent.

For a growing family, the right structure means a surviving spouse can maintain their lifestyle, keep the house, and fund their children's education — without financial strain.

Use the comparison framework here as a starting point. If you want a second set of eyes on your options, Vellum Life Group offers free, no-obligation consultations — and works with 15+ A-rated carriers to find coverage that fits your family's actual budget and goals.

Frequently Asked Questions

Is family life insurance worth it?

Life insurance for your family is worth it when you have financial dependents. Whether you use individual policies, riders, or a combination depends on each family member's health, your budget, and the coverage amount each person actually needs.

How much does a $100,000 life insurance policy cost per month?

A $100,000 20-year term policy is among the most affordable coverage available. According to MoneyGeek, a healthy 35-year-old non-smoker pays roughly $14/month (female) or $16/month (male). By age 45, those rates rise to approximately $21–$26/month.

Can I get life insurance with a pre-existing medical condition?

Yes, in many cases. A pre-existing condition doesn't automatically disqualify you — some carriers specialize in higher-risk applicants. Because rates and approval odds vary significantly by carrier, working with an independent advisor like Vellum Life Group — who can compare options across multiple carriers — gives you the best shot at affordable coverage.

Is it cheaper to add a spouse rider or buy a separate life insurance policy?

A spouse rider typically costs less monthly, but delivers less coverage. For a healthy spouse who needs $300,000 or more in protection, a separate individual term policy usually provides better value — even at a higher premium — because the coverage amount is meaningfully larger.

What type of life insurance is best for a family with young children?

Individual term policies for each income-earning or caregiving parent work best, sized to cover income replacement, mortgage payoff, and future education costs. Choose a term length that runs until your youngest child is likely financially independent — typically 20 or 30 years.

Can one life insurance policy cover an entire family?

No single policy covers an entire family the way a health plan does. A primary policy with spouse and child riders comes closest to that model, but still provides less coverage depth than separate individual policies for each adult. Riders serve a supplementary role, not a replacement for standalone coverage.