Pre-existing conditions do make the process harder and more expensive. There's no point pretending otherwise. But "harder" doesn't mean impossible, and the right policy type combined with the right carrier can still deliver meaningful coverage for final expenses, legacy goals, or protecting a surviving spouse.

The scale of this challenge is worth acknowledging: according to the CDC, 93% of U.S. adults aged 65 and older reported at least one chronic condition in 2023, and nearly 79% reported two or more. This isn't a fringe situation — it's the norm. The life insurance industry knows it, and the policy options available today reflect that reality.

Key Takeaways

- Pre-existing conditions don't automatically disqualify seniors from life insurance coverage

- Policy options depend on condition type, severity, and how consistently it's being managed

- Guaranteed issue and final expense insurance offer coverage access even when other options are unavailable

- Premiums lock in at purchase and stay fixed even if health declines after the policy is issued

- Shopping multiple carriers matters: the same applicant can qualify at very different rates and terms

What Counts as a Pre-Existing Condition for Senior Life Insurance?

In life insurance underwriting, a pre-existing condition is any chronic, ongoing, or recurring medical issue that was diagnosed or treated before you applied. The distinction matters: a broken arm that healed five years ago is not a pre-existing condition. Ongoing heart disease, managed or not, is.

Common conditions that come up during senior underwriting include:

- Heart disease and coronary artery disease

- Type 2 diabetes

- COPD and other respiratory conditions

- High blood pressure (hypertension)

- History of cancer

- History of stroke

- Obesity

- Kidney disease

- Depression and anxiety

That list covers a lot of ground — and most seniors with a managed condition still have viable options.

The Difference Between "Present" and "Disqualifying"

Insurers don't just see a diagnosis and stamp "denied." They evaluate manageability, treatment adherence, and stability. A 68-year-old with well-controlled Type 2 diabetes who sees their physician regularly, maintains stable lab values, and follows their medication regimen is assessed very differently from someone with the same diagnosis who hasn't seen a doctor in two years.

Having a condition on file typically means a higher premium or a lower rate class — not an automatic rejection. Insurers reserve outright denial for severe, progressive, or untreated cases where the risk can't be priced.

Types of Life Insurance Available to Seniors With Pre-Existing Conditions

The right policy depends on your health profile, coverage goals, and budget. More health restrictions generally mean fewer options — but at least one option almost always remains. Here's how the main policy types stack up.

Guaranteed Issue Life Insurance

Guaranteed issue (also called guaranteed acceptance) life insurance requires no medical exam and no health questions. Approval is guaranteed for anyone within the eligible age range — typically 50 to 85 for most carriers. Mutual of Omaha, for example, offers guaranteed whole life coverage for ages 45–85, with coverage from $2,000 to $25,000.

This makes it the most accessible option for seniors with serious, multiple, or poorly controlled conditions.

Trade-offs to understand:

- Coverage amounts are generally capped at $5,000–$25,000

- Premiums are higher relative to the benefit than other policy types

- Most policies include a graded death benefit clause: if the insured dies within the first 2–3 years, beneficiaries receive only a return of premiums paid (sometimes with interest), not the full face amount

The graded benefit is a real limitation, but for seniors who can't qualify elsewhere, guaranteed issue still serves its core purpose.

Final Expense Insurance

Final expense insurance — sometimes called burial insurance — is a small whole life policy built specifically to cover end-of-life costs: funeral expenses, outstanding medical bills, and remaining debts. The national median funeral cost with burial was $8,300 in 2023, and cremation averaged $6,280, meaning even a modest policy can cover the full cost without depleting a family's savings.

Key characteristics:

- Coverage typically ranges from $5,000 to $50,000

- Permanent coverage — it doesn't expire

- Builds a small cash value over time

- Available as guaranteed issue or simplified issue, depending on health

LIMRA data from 2025 shows that 1.06 million final expense policies were sold in 2024 — up 10% year over year. That growth reflects how many families are actively choosing this route to protect against end-of-life costs.

Simplified Issue Life Insurance

Simplified issue skips the medical exam but does ask a short series of health questions. Applicants can be declined based on answers, but the approval bar is much lower than fully underwritten policies — making this a solid middle ground for seniors with mild-to-moderate conditions.

Advantages over guaranteed issue:

- Higher coverage limits available

- Faster approval — sometimes same day or within a few days

- Lower premiums than guaranteed issue for the same face amount

Whole Life and Term Life (Fully Underwritten)

For seniors whose health allows it, fully underwritten whole life insurance sits at the top of the spectrum: the broadest coverage, the most competitive premiums, and the strongest long-term value. Seniors with well-managed conditions — controlled hypertension, diabetes without complications — often still qualify. They'll typically land in a standard or substandard rate class with higher but permanently fixed premiums (a higher-risk tier that reflects elevated health factors, not a disqualification).

Term life is possible for some seniors in their 60s, but availability shrinks significantly after 70. For most seniors focused on legacy planning or final expenses, permanent coverage is the better fit.

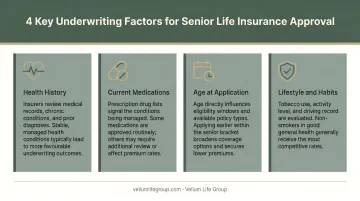

Key Factors That Determine Eligibility and Premiums

Knowing what underwriters look for lets you present the strongest possible application — and avoid surprises at approval time.

Type and Severity of the Condition

Conditions range from mild and manageable (controlled hypertension) to severe and progressive (terminal illness, advanced heart failure). The more severe and less treatable the condition, the more it limits available policy types and drives up premiums — or triggers a denial.

How Well the Condition Is Managed

Treatment adherence is one of the biggest underwriting factors. Seniors who can demonstrate:

- Regular physician visits

- Stable lab results over time

- Consistent use of prescribed medications

- An active treatment plan

...are evaluated far more favorably than those with the same diagnosis who haven't managed it consistently. Nationwide's underwriting guidance indicates that Type 2 diabetes or hypertension applicants generally need at least six months of stable control to qualify for standard rate classes.

Age at Application

Age compounds the effect of any pre-existing condition. A 62-year-old with diabetes is assessed very differently from a 78-year-old with the same diagnosis. This is the core reason to apply sooner rather than later — even if health isn't perfect, more policy types remain available at younger ages, and premiums will be lower.

Lifestyle Factors

Smoking status, BMI, and physical activity all intersect with chronic conditions during underwriting. Smoking is particularly consequential — smokers pay an average of 218% more than non-smokers for life insurance. For a senior who also has a chronic condition, smoking can close off most non-guaranteed issue options entirely. Demonstrating a tobacco-free history of five or more years can meaningfully improve your premium tier and expand the policy types available to you.

The Rate Class System

All the factors above — condition severity, management history, age, and lifestyle — feed into a single outcome: your rate class. Insurers assign applicants to tiers ranging from Preferred Plus and Preferred down to Standard and Substandard (table-rated). Seniors with pre-existing conditions typically land in Standard or Substandard.

What makes this actionable: every insurer's classification system is different. The same applicant can receive meaningfully different quotes from different carriers. Comparing multiple insurers isn't just helpful — it often determines whether you find an affordable policy at all.

How to Improve Your Chances of Getting Approved

Gather Your Medical Records Before Applying

Documentation is your strongest asset. Medical records showing a stable condition, consistent medication use, normal-range lab results, and regular check-ups all reduce the perceived risk an insurer is taking on. Many carriers — including Pacific Life — require applicants over 65 to have had a physician visit within 12 months of applying and to provide an Attending Physician Statement. Pull these records before you start the process.

Be Completely Accurate on Your Application

Misrepresenting or omitting health information can void a policy at the time of claim. The Texas Department of Insurance confirms that during the two-year contestable period, if an insurer finds that an applicant gave wrong information or omitted something material, it can deny payment. Accurate disclosures protect the policy's value for your beneficiaries when they need it most.

Compare Multiple Insurers Before Accepting Any Quote or Denial

A denial from one carrier is not a verdict on your insurability. Underwriting guidelines differ significantly from company to company, and a condition that disqualifies you at one insurer may be accepted at another with different risk tolerances.

Applying to carriers on your own creates repeated reviews of your health history. Working with an independent advisor like Vellum Life Group means someone shops multiple carriers on your behalf — without that repeated exposure to your records.

After a Denial: What to Do Next

- Explore guaranteed issue policies immediately — they cannot decline based on health

- Apply to other carriers, since criteria vary widely

- Consider reapplying after allowing more time to pass since a diagnosis, or after demonstrating improved management

- Consult an independent advisor who can identify which carriers are most likely to approve your specific profile

How Vellum Life Group Helps Seniors With Pre-Existing Conditions

Navigating life insurance with a complex health history is difficult — and doing it alone, carrier by carrier, is both time-consuming and strategically inefficient.

Eva Ikonomakos, founder of Vellum Life Group, brings over 15 years of experience across financial services, healthcare, and international business. That combination gives her a grounded perspective when helping seniors work through applications where health history is a central factor.

Vellum partners with 15+ A-rated carriers — including Mutual of Omaha, Corebridge Financial, Transamerica, and Americo — some of which focus on higher-risk applicants. Rather than requiring seniors to apply one-by-one and trigger repeated scrutiny of their health history, Eva compares underwriting standards across carriers to match each client with the insurer most likely to approve them at the most competitive rate.

Working with Vellum also means:

- Free initial consultation with no obligation

- 24-hour response time on all inquiries

- Annual policy reviews as health or coverage needs change

- Claims assistance when it matters most

To get started, you can reach Eva at 917-363-3554, at info@vellumlifegroup.com, or by booking a 30-minute consultation at calendly.com/eva-ikonomakos/30min.

Frequently Asked Questions

Is it hard to get life insurance with pre-existing conditions?

It can be more challenging and more expensive, but not impossible. Most seniors with pre-existing conditions qualify for at least one policy type — often guaranteed issue or final expense coverage. Working with a multi-carrier advisor simplifies the search considerably and helps you avoid applying to carriers unlikely to approve your profile.

How much is a $500,000 life insurance policy for a 70-year-old man?

Costs vary significantly by health rating and carrier. For a 70-year-old male, NerdWallet's 2026 data shows whole life premiums at roughly $1,273/month (non-smoker, standard health) or around $2,355/month for a smoker. Many 70-year-olds opt for smaller final expense policies instead, as large face-value coverage becomes substantially more expensive at this age.

What type of life insurance is easiest to get for seniors with pre-existing conditions?

Guaranteed issue life insurance. It requires no medical exam, no health questions, and approves all applicants within the eligible age range (typically 50–85). Coverage amounts are limited — generally $5,000 to $25,000 — but access is essentially universal.

Can I get life insurance if I have diabetes or heart disease?

Yes. Both conditions are among the most common in senior underwriting and do not automatically disqualify applicants. Well-managed Type 2 diabetes or stable heart disease may still qualify for simplified issue or fully underwritten policies. More severe or poorly controlled cases typically route to guaranteed issue coverage.

Will my premiums increase if my health gets worse after I buy a policy?

No. Life insurance premiums lock in at purchase and do not increase if your health deteriorates after the policy is issued. This is a strong reason to apply early, especially with a progressive condition.

What should I do if I'm denied life insurance because of a health condition?

Start by exploring guaranteed issue policies — they cannot decline based on health. Then apply to different carriers, since underwriting criteria differ meaningfully across companies. An independent advisor can match your profile to the right carrier without requiring you to apply repeatedly on your own.