This guide addresses two distinct planning challenges. First, how parents should insure themselves so their child is cared for after they're gone. Second, whether insuring the child is also worth considering — because some parents will outlive them.

Key Takeaways

- Permanent life insurance (whole life, universal life, or survivorship) is generally a better fit than term for special needs families

- Never name a special needs child as beneficiary directly — doing so can disqualify them from Medicaid or SSI

- A special needs trust should typically be named as the life insurance beneficiary

- Consider insuring the child early — coverage is more affordable now and insurability may narrow with age

- Act early — health changes and age both increase costs and reduce options

The Unique Financial Planning Challenge for Special Needs Families

Standard advice tells parents to match insurance coverage to temporary financial obligations — a mortgage, college tuition, income replacement for a decade or two. When those obligations end, so does the need. That logic breaks down completely when a child's disability means they'll need financial and personal support for life.

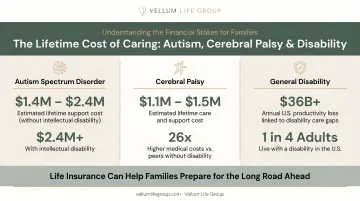

A study indexed by the NIH estimated the lifetime cost of supporting a person with autism spectrum disorder at $2.4 million with an intellectual disability, and approximately $1.4 million without. The CDC's cost-of-illness analysis placed average lifetime care costs for cerebral palsy at nearly $1 million per person. These figures cover housing, medical care, therapies, and personal support. None of them account for inflation.

What makes those numbers harder to meet is that caregiving itself erodes the financial resources parents need to cover them. A 2025 peer-reviewed study found that child disability reduces mothers' employment rates by 9% and annual earnings by 12%, with effects persisting for at least a decade. Many parents also draw down retirement savings and reduce Social Security credits while serving as primary caregivers.

This creates a compounding vulnerability:

- The child requires financial support that doesn't end at age 18 or 22

- The caregiving years reduce the parent's own savings, earnings, and retirement security

- A parent's death without permanent coverage can unravel decades of careful planning

Securing permanent coverage while a parent is still healthy and insurable is one of the most direct ways to close that gap before it opens.

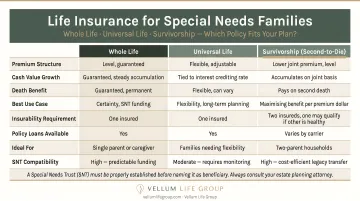

Which Life Insurance Policy Type Is Right for Parents of Special Needs Children

Term life insurance is affordable and straightforward, but it has a fundamental flaw for this situation: it ends. When a 20-year term expires, there's no death benefit remaining. If the parent's health has declined in the interim, getting new coverage may be difficult, expensive, or impossible. For a family whose child will need support at age 45, 55, or 65, that gap matters.

Permanent Life Insurance: The Preferred Foundation

| Policy Type | How It Works | Best For |

|---|---|---|

| Whole Life | Fixed premiums, guaranteed death benefit, tax-deferred cash value that can be borrowed against | Parents who want predictability and a straightforward structure |

| Universal Life | Flexible premiums and adjustable death benefit; requires more active management to keep in force | Parents with fluctuating income or shifting care cost projections |

Survivorship (Second-to-Die) Life Insurance: A Cost-Effective Option for Two-Parent Households

Survivorship policies cover two people under one policy and pay the death benefit only when the second parent dies. For special needs planning, this timing often aligns well — the funds are needed most after both parents are gone.

Key advantages include:

- Costs less than carrying two separate permanent policies

- Opens underwriting options when one spouse has a health condition that would make individual coverage expensive

- Consolidates planning into a single policy with one beneficiary designation and one trustee relationship

Parents can also hold both term and permanent coverage simultaneously. A term policy might cover a mortgage or other temporary obligations, while whole life provides the permanent protection the child needs regardless of when the parent dies. An independent advisor can help determine what combination fits a specific stage of life.

Why Naming Your Special Needs Child as Beneficiary Can Backfire

This is one of the most consequential mistakes in special needs financial planning — and it's easy to make without knowing it.

Most means-tested government programs, including Medicaid and Supplemental Security Income (SSI), have strict asset limits. SSA sets the countable resource limit at $2,000 for an individual. If a life insurance death benefit pays directly to the child and pushes their assets above that threshold, they can lose Medicaid coverage and SSI payments — often the very programs funding their daily care.

Beyond the SSI resource limit, there are two additional risks parents often overlook:

- Medicaid estate recovery: State programs are required to seek repayment of certain benefits after an enrollee's death. A large lump-sum payout can trigger complex repayment dynamics that vary significantly by state.

- Informal family arrangements: Some parents leave proceeds to a sibling or relative, assuming they'll use it for the child. Once the money is legally in someone else's name, there's no obligation to spend it on the child — and that person's own financial difficulties, divorce, or death puts those funds at risk.

There's also a critical timing window to plan around. At age 18, SSI eligibility is reassessed based on the adult child's own income and assets — not the parents'. The $2,000 resource limit applies directly to them from that point forward. Beneficiary structure needs to be in place before that milestone, not after.

How a Special Needs Trust Protects Your Child's Benefits and Future

A special needs trust (also called a supplemental needs trust) is a legal entity that holds and distributes assets for a person with disabilities. Because the trust — not the child — legally owns the assets, those assets don't count against the individual's Medicaid or SSI eligibility.

How It Works with Life Insurance

Parents name the special needs trust as the beneficiary of their life insurance policy. When the parent dies, the death benefit flows into the trust rather than directly to the child. A trustee then manages and distributes those funds according to the parent's written instructions — covering expenses that government benefits don't, like transportation, recreation, technology, and additional therapies.

The Special Needs Alliance notes that a third-party special needs trust — one funded by parents rather than the beneficiary's own assets — typically carries no Medicaid payback provision. Remaining assets after the beneficiary's death can pass to whoever the parent designates.

Choosing a Trustee

The trustee manages everything after the parent is gone. Options include:

- A trusted sibling or other family member who understands the child's needs

- A professional fiduciary or corporate trustee for families without a clear personal option

- A combination, where a family member serves as co-trustee alongside a professional

Whoever you choose must be financially responsible, genuinely familiar with your child's day-to-day needs, and realistically likely to outlive them — this isn't a role for the most convenient option.

Coordination with ABLE Accounts and Extended Family

A special needs trust can also coordinate with ABLE accounts — tax-advantaged savings accounts for people with disabilities. The IRS sets the 2025 ABLE contribution limit at $19,000, and ABLE balances up to $100,000 don't count as resources for SSI purposes. A trustee can contribute trust funds to the beneficiary's ABLE account for more accessible spending on day-to-day expenses.

That same structure should extend to your extended family. Grandparents and relatives need to know to direct any gifts or inheritances to the trust — not to the child directly. Even well-intentioned gifts can trigger benefit disqualification without this safeguard.

Setting up a special needs trust requires an attorney with specific experience in disability and benefits law. The Special Needs Alliance provides a directory to find qualified attorneys by state. Don't delay buying life insurance while the trust is being established. Coverage can be purchased now with a family member named as interim beneficiary, then updated to the trust once it's finalized.

Should You Also Get Life Insurance on Your Special Needs Child?

Most special needs planning focuses on what happens to the child when a parent dies. But some parents will outlive their child — and that scenario carries its own financial reality.

A 2002 study found that parents experienced an immediate income drop of as much as 72% following the death of a disabled or chronically ill child, largely due to lost government benefit income. Beyond the income loss: funeral expenses, years of depleted retirement savings from caregiving, and the practical disruption that grief brings.

Life insurance on the child can help offset these consequences.

Two Ways to Insure the Child

Standalone child life insurance policy: The parent owns the policy, not the child. This matters: if the child owns the policy, the cash value counts as their asset for SSI and Medicaid purposes. Parent ownership keeps it outside the child's resource calculation.

Child coverage rider on a parent's policy: Typically more affordable than a standalone policy. Many carriers allow the rider to convert to a standalone permanent policy when the child reaches adulthood, with no new medical underwriting required. That conversion feature matters most for children with conditions that might make individual coverage harder to obtain later.

Underwriting Reality

Insurers evaluate children with special needs based on diagnosis, functional level, and health history. Outcomes vary significantly:

- Mild to moderate conditions may qualify for standard rates

- More complex diagnoses may result in rated premiums (higher cost) or graded death benefits

- Some severe conditions may result in postponement or denial

Not every diagnosis leads to denial. Working with an advisor who understands disability underwriting — and who can present the child's situation accurately and in the most favorable context — often determines the outcome.

How to Calculate Your Coverage Need and Find the Right Policy

Coverage calculation for special needs families involves more variables than a standard income-replacement estimate. The key inputs:

- Projected lifetime care costs — housing, medical care, therapies, personal support

- Government benefits the child will likely qualify for — Medicaid, SSI, waiver programs

- Existing assets and savings that will be available

- How long coverage needs to last — potentially the child's entire lifetime

The gap between projected care costs and available resources is the number you're trying to cover. That gap, funded through a special needs trust, is what the death benefit needs to fill.

For a general cost benchmark: Policygenius reported that a $1 million whole life policy for a healthy 35-year-old nonsmoker runs approximately $801/month for women and $920/month for men. Term coverage costs far less — a 20-year, $1 million term policy can start around $35/month for a healthy applicant in their 30s — but the tradeoffs for this situation are real.

Knowing those numbers makes the next step clear: don't wait. Two things parents should act on now:

- Buy coverage sooner — premiums rise with age, and any health change can reduce insurability or significantly increase what you'll pay.

- Set up the trust structure — the trust can be named as beneficiary once it's established, but coverage can and should be purchased before the trust is finalized.

At Vellum Life Group, founder Eva Ikonomakos works with 15+ A-rated carriers to help families identify the right policy structure, work through underwriting for more complex situations, and revisit coverage as circumstances change over time.

Frequently Asked Questions

Can you get life insurance on a special needs child?

Yes, in many cases. Eligibility depends on the child's specific diagnosis, functional level, and health history. Some conditions qualify for standard rates; others result in rated premiums or graded death benefits where full coverage phases in over a few years. Working with an advisor experienced in disability underwriting improves the chances of finding workable coverage.

How much does a $1,000,000 life insurance policy cost per month?

It varies widely based on age, health, tobacco use, and policy type. A healthy 35-year-old might pay roughly $35–$55/month for a 20-year term policy, while a $1 million whole life policy at the same age runs approximately $800–$920/month. Comparing quotes across multiple carriers is worth the effort, since pricing can vary significantly for the same coverage amount.

How long can disabled children stay on parents' health insurance?

Under the ACA, dependent children can remain on a parent's health plan until age 26. Many states and group plans allow disabled adult children to stay beyond 26 if the disability began before that age, though this varies by state and plan. Life insurance is a separate planning layer that addresses long-term financial security after a parent's death.

Should I name my special needs child as the beneficiary of my life insurance?

Generally not, if the child receives or may receive Medicaid or SSI. A direct lump-sum payout could push their assets above the $2,000 SSI resource limit and trigger loss of benefits. A special needs trust should typically be named as beneficiary instead.

What is a special needs trust and how does it work with life insurance?

A special needs trust holds assets for a person with disabilities without those assets counting against government benefit eligibility. Parents name the trust as the life insurance beneficiary, so when the parent dies, the death benefit flows into the trust and the trustee distributes funds per the parent's instructions.

What happens to my special needs child's government benefits when they turn 18?

At 18, the SSA reassesses SSI eligibility using adult disability criteria, and the $2,000 asset limit applies to the child's own income and assets directly. A properly structured special needs trust in place before this transition protects both benefit eligibility and the child's long-term financial security.