This guide breaks down both definitions clearly: how each type works, who each is designed for, what it costs, and how to decide whether either one makes sense for your situation.

Key Takeaways

- "Modified whole life" describes two distinct products: one adjusts premiums over time, the other restricts the early death benefit

- Modified premium whole life suits healthier applicants who expect income to grow over time

- Modified benefit whole life is typically designed for applicants with serious pre-existing conditions

- Both types cost more over time than standard whole life alternatives

- Many applicants with common health conditions can still qualify for immediate-coverage plans with no waiting period

What Is Modified Whole Life Insurance?

Modified whole life insurance is a permanent policy where either the premium structure or the death benefit structure differs from the standard model. A standard whole life policy has fixed premiums from day one and pays the full death benefit immediately upon death. A "modified" version changes one of those two elements — but both versions still offer lifelong coverage and build cash value over time.

The confusion arises because the word "modified" gets applied to both scenarios in the market. Some carriers use it to mean lower early premiums. Others use it to mean a restricted early death benefit. Knowing which type you're looking at changes everything about how you evaluate the policy.

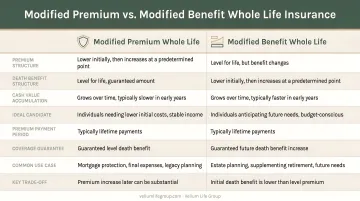

Modified Premium Whole Life

With modified premium whole life, you pay lower introductory premiums for a set period — typically 2 to 10 years, depending on the carrier — after which premiums increase permanently to a higher fixed rate for the rest of your life. The death benefit stays constant throughout — only the premium changes over time.

This product requires standard medical underwriting (a health assessment process). The insurer accepts lower early premiums because it has evaluated your health risk and is confident in a low probability of early claim. It's a real product with a legitimate use case, but it's narrower than many consumers assume.

Modified Benefit Whole Life (Graded Benefit)

Modified benefit whole life — also called graded benefit whole life or guaranteed issue whole life — works differently. Premiums are fixed from day one. What changes is what your beneficiaries receive if you die during the first 2 to 3 years.

During this waiting period, a natural-cause death typically pays beneficiaries only a return of premiums paid plus interest (commonly 10%), not the full face amount. After the waiting period ends, the full benefit applies for any cause of death.

Insurers offer this structure specifically because they accept applicants with serious health conditions — often with no medical exam and no health questions. The waiting period is how the insurer manages that risk. The Insurance Compact requires policies using this structure to disclose it prominently, with a cover-page notice stating "This policy has a limited graded death benefit."

Modified Premium vs. Modified Benefit: Two Very Different Policies

Here's the structural difference at a glance:

| Feature | Modified Premium | Modified Benefit (Graded) |

|---|---|---|

| What changes | Your premium amount | Your beneficiaries' early payout |

| Coverage timing | Immediate and full | Restricted for 2-3 years |

| Premiums | Fixed after introductory period | Fixed from day one |

| Underwriting required | Yes — health questions apply | No or minimal |

| Designed for | Healthier applicants, budget constraints | Applicants with serious conditions |

| Coverage limits | Standard whole life amounts | Typically $25,000 or under |

Terminology Is Inconsistent — Always Ask

Carrier naming conventions create real confusion for buyers. Mutual of Omaha labels its product a "Graded Benefit Plan." Corebridge calls a comparable product "Guaranteed Issue Whole Life." AAA uses the hybrid phrase "Guaranteed Issue Graded Benefit Whole Life." When an advisor or insurer uses the word "modified," always ask: does the premium change, or does the early death benefit change? The answer determines which type of policy you're actually buying.

Modified Premium Is Not the Same as Limited Pay

This is a common mix-up. With limited pay whole life, premiums stop entirely after a set number of years (say, 20 years), and coverage continues for life with no further payments. With modified premium whole life, premiums never stop — they only increase after the introductory period. Accepting a modified premium policy thinking it works like limited pay is a costly misunderstanding.

Cash Value Implications

That premium timing also affects what builds inside the policy over time.

Modified premium policies accumulate cash value more slowly during the lower-premium introductory period — less money flowing in means slower growth. Modified benefit policies can build cash value comparably to other guaranteed-issue products, but those policies generally carry lower face amounts, which limits total cash value potential from the start.

Pros and Cons of Modified Whole Life Insurance

Advantages

Both types share some genuine benefits:

- Lifelong coverage that never expires, regardless of health changes

- Fixed premiums after any adjustment period — no surprises later

- Death benefit that won't decrease (after the waiting period, for modified benefit plans)

- Tax-deferred cash value growth accessible through policy loans

Additional advantages by type:

- Modified premium policies offer lower initial costs, making permanent coverage accessible when budget is tight today

- Modified benefit policies provide guaranteed or near-guaranteed acceptance for people who cannot qualify for standard underwriting, making them the only viable option for many high-risk applicants

Disadvantages

Modified premium whole life:

- Premiums increase significantly after the introductory period; if income doesn't grow as expected, the policy could lapse

- Cash value grows more slowly in early years and may never fully match a comparable fixed-premium policy

- Total lifetime cost may exceed what a standard whole life policy would have cost

Modified benefit whole life:

- The 2- to 3-year waiting period means beneficiaries may receive far less than the full benefit if the insured dies early

- Coverage limits are small — Corebridge caps coverage at $5,000–$25,000, Mutual of Omaha's graded plan at $2,000–$20,000, and most carriers follow similar limits

- Premiums are higher per dollar of coverage than standard plans, because the insurer assumes higher risk with little to no underwriting

Worth knowing before you decide: Neither type is automatically the right choice. Many applicants — even those with several health conditions — can qualify for a standard whole life or final expense policy with immediate coverage and lower long-term cost. Comparing your options across both modified and standard plans before committing can save you money over the life of the policy.

How Much Does Modified Whole Life Insurance Cost?

What Drives the Price

Two types of plans drive pricing differently:

- Graded/guaranteed issue plans: Premiums are based solely on age and gender. There's no health underwriting, so a healthy 60-year-old pays the same rate as a high-risk 60-year-old.

- Modified premium plans: Early premiums are noticeably lower than standard whole life — but post-adjustment premiums typically exceed what a standard policy would have cost from day one. Lower early premiums aren't a discount; they shift cost to later years.

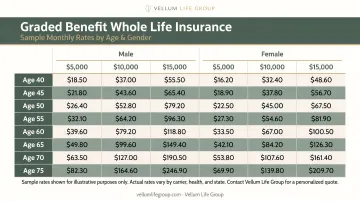

Sample Monthly Rates: Graded Benefit Whole Life

The table below uses illustrative figures from Insurance Geek's 2026 Gerber guaranteed issue rate data and 2025 AIG/Corebridge data. Confirm current rates with a licensed advisor before making any decisions.

| Age | Gender | $10,000 Coverage | $15,000 Coverage | $25,000 Coverage |

|---|---|---|---|---|

| 50 | Female | $34 | $51 | $85 |

| 50 | Male | $44 | $66 | $109 |

| 60 | Female | $51 | $76 | $126 |

| 60 | Male | $64 | $95 | $158 |

| 70 | Female | $76 | $113 | $187 |

| 70 | Male | $99 | $148 | $247 |

| 80 | Female | $190 | — | $513 |

| 80 | Male | $206 | — | $519 |

Note: Age-80 $15,000 rates were not available in retrieved sources. Gerber age-80 rates were also not found in the 2026 table.

Before committing to any modified plan, request a side-by-side illustration comparing lifetime premiums against a standard whole life policy. In many cases, the total lifetime cost of a modified premium plan exceeds what you'd pay under a standard policy — a gap that only becomes visible when you look at the full picture.

Who Should (and Shouldn't) Consider Modified Whole Life Insurance

Right Candidate: Modified Benefit (Graded) Plans

A graded benefit plan makes sense for someone who has been declined for standard coverage, or who has a condition that makes standard underwriting impossible. Conditions that commonly lead to this outcome include:

- Active or recently treated cancer

- Alzheimer's disease or dementia

- Hospice, nursing home, or institutional care status

- End-stage renal disease or active dialysis

- Active substance abuse within the past two to three years

For these individuals, a graded benefit plan may be the only available option. That makes it the right call — waiting period included.

Right Candidate: Modified Premium Whole Life

This is a niche product. It suits younger applicants — typically under 45 — who are confident their income will rise substantially in the coming years. A resident physician, early-career attorney, or someone early in their career might reasonably choose lower early premiums now and absorb the premium increase later. A good rule of thumb: if you can't project a meaningful income increase within five to seven years, the math rarely works in your favor.

Who Should NOT Buy a Modified Plan

Anyone who can qualify for standard whole life or final expense coverage with immediate coverage should explore that path first.

Many common health conditions do not automatically disqualify an applicant from standard underwriting:

- Well-controlled type 2 diabetes

- High blood pressure managed with medication

- History of heart disease (depending on timing and severity)

- Anxiety or depression managed with medication (including SSRIs like Lexapro)

- Lupus or other autoimmune conditions, depending on stability

The key is working with an independent advisor who has access to multiple carriers and can match your health profile to the most favorable underwriting available. An independent advisor with access to 10 or more carriers can often find immediate coverage for applicants with pre-existing conditions — carriers that a single-company agent would never surface.

Practical Decision Framework

If you've been quoted a modified plan, ask:

- Can any carrier in your panel offer me immediate coverage given my health history?

- If not, review the graded benefit terms: confirm the exact waiting period length and the payout structure during that window

- Calculate the total premiums paid at 10, 15, and 20 years against the coverage amount to evaluate long-term value

Those three questions will tell you most of what you need to know.

Frequently Asked Questions

What is the difference between graded benefit whole life and modified whole life?

"Graded benefit" and "modified benefit" whole life often describe the same product — a policy that restricts the early death benefit during a waiting period before full coverage activates. "Modified premium" whole life, by contrast, refers to lower introductory premiums that increase permanently after a set period. The terms are used inconsistently across the market, so always confirm with the insurer which structure applies.

Can I get modified whole life insurance if I have lupus or take medications like Lexapro?

Lupus and Lexapro (escitalopram) are typically not automatic disqualifiers for standard underwriting. Underwriters evaluate severity, stability, organ involvement, treatment history, and other risk factors — not just the diagnosis or medication name. A modified benefit plan is generally only required for the most severe or unmanaged conditions; working with an independent advisor who can shop multiple carriers is the most reliable way to find out where you stand.

Does modified whole life insurance build cash value?

Yes — both types build cash value over time, as standard whole life does. Modified premium policies accumulate cash value more slowly during the introductory period because lower premiums mean less money flowing in. Modified benefit policies carry lower coverage limits, which caps total cash value regardless of how fast it grows.

Is modified whole life insurance worth it?

It depends entirely on your health and financial situation. For someone who genuinely cannot qualify for anything else, a modified benefit plan is worth having — it provides coverage that would otherwise be unavailable. For someone who can qualify for standard coverage, a modified plan is rarely the better choice due to higher lifetime costs or limited early benefits.

Can a modified whole life policy lapse, and what happens if it does?

Yes. Like any life insurance policy, a modified whole life plan lapses if premiums go unpaid. Some policies include an automatic premium loan provision that uses available cash value to cover missed premiums temporarily — but this only applies if the policy includes that provision and has sufficient cash value. If the policy lapses, coverage ends and any surrender value may be returned to the policyholder.

Can I convert a modified premium whole life policy to a standard whole life policy?

Conversion options vary significantly by carrier and are not universally available. Some insurers allow an exchange to a different policy structure, but this is not a standard feature. Ask about conversion rights before purchasing — this matters most if your financial situation changes down the road.