Limited payment whole life insurance was designed to solve exactly this problem. You pay premiums for a defined number of years, and then you stop — permanently. Your coverage stays in force for the rest of your life.

This guide covers what limited payment whole life insurance is, how it works, the different policy structures available, the real benefits and drawbacks, what it typically costs, and who it makes the most sense for. By the end, you'll have a clear, jargon-free answer to whether this type of policy belongs in your financial plan.

Key Takeaways

- Pay premiums for a set number of years (typically 7, 10, 15, or 20 years), then stop — coverage lasts your entire lifetime

- Annual premiums are higher than traditional whole life, but they end completely, often before retirement

- Cash value grows tax-deferred and can be accessed through policy loans or withdrawals

- Premium amounts depend on your age, health, coverage amount, and chosen payment period

- Works best for higher earners who want premiums fully paid off before retirement

What Is Limited Payment Whole Life Insurance?

Limited payment whole life insurance is a type of permanent life insurance where you pay premiums for a defined number of years — not forever. Once that payment period ends, the policy is considered "paid up." Your death benefit and cash value remain fully intact for the rest of your life, with no further premiums required.

As the NAIC notes, these policies typically build cash value faster than ordinary whole life and require higher premiums in exchange for that compressed timeline.

How It Differs from Traditional Whole Life

Standard whole life insurance spreads premium payments across your entire lifetime. Limited payment whole life front-loads those same payments into a shorter window — the coverage itself is identical once the policy is fully paid up.

The contrast with term life is just as important. Term life pays a death benefit only if you die during the coverage term — when the term ends, so does the coverage. Limited pay whole life works differently: the payment period ends, but the coverage never does.

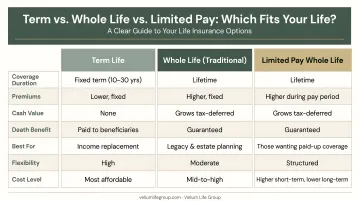

Here's a quick side-by-side of how all three compare:

| Policy Type | Payment Period | Coverage Duration | Cash Value |

|---|---|---|---|

| Term Life | Duration of term | Term only (expires) | None |

| Traditional Whole Life | Lifetime | Permanent | Yes, slower growth |

| Limited Payment Whole Life | Fixed years (10, 20, etc.) | Permanent | Yes, faster growth |

A Practical Example

Consider a 40-year-old who buys a 10-pay policy. They pay premiums each year until age 50. After that, no more payments are due — ever. The death benefit and cash value remain fully in force for the rest of their life.

The structure is similar to choosing a 15-year mortgage over a 30-year mortgage. You pay more annually, but you finish paying far sooner — and your total outlay over a lifetime may actually be less.

Key characteristics of a limited payment whole life policy:

- Premiums are fixed and guaranteed not to increase

- Coverage is permanent — it doesn't expire after the payment period

- Cash value accumulates faster than traditional whole life

- The policy cannot lapse once fully paid up, as long as no loans are outstanding

Types of Limited Payment Whole Life Insurance Policies

The most common payment structures are 7-pay, 10-pay, 15-pay, 20-pay, and paid-up-at-65. Each suits a different financial profile — here's how they compare at a glance:

| Payment Period | Premium Level | Best For |

|---|---|---|

| 7-Pay | Highest | High earners wanting fastest paid-up status |

| 10-Pay | High | Mid-career professionals with strong cash flow |

| 15-Pay | Moderate-High | Balancing affordability with earlier paid-up status |

| 20-Pay | Moderate | Those wanting lower annual payments over a longer horizon |

| Paid-Up at 65 | Variable | Workers who want premiums to stop exactly at retirement |

The 7-Pay Policy and MEC Rules

Seven years is the shortest funding window that keeps a policy from being classified as a Modified Endowment Contract (MEC) under IRC Section 7702A. A single-premium policy — where you pay everything at once — is automatically classified as a MEC. More on why that matters in the drawbacks section.

The Paid-Up-at-65 Option

This structure aligns premium payments with your working years. Payments stop entirely at age 65, which is when most people transition to retirement income. For anyone budgeting around a fixed retirement income, the alignment is straightforward. Premiums are calculated based on your age at enrollment, so starting earlier keeps the annual cost lower while still hitting that same finish line.

Benefits of Limited Payment Whole Life Insurance

Permanent Coverage Without Lifelong Payments

Once the payment period ends, the policy stays in force for life — no further premiums, no renewal requirements. Your beneficiaries receive a guaranteed death benefit whenever you pass, giving your family financial certainty without ongoing cost.

Faster Cash Value Accumulation

Because premiums are higher and concentrated into fewer years, cash value builds more rapidly compared to a traditional whole life policy with the same death benefit. That larger cash value pool can be borrowed against or withdrawn for retirement income, emergencies, or other major financial needs down the road.

Tax Advantages

Limited payment whole life policies carry three distinct tax benefits:

- Tax-deferred growth — cash value grows without annual income tax on the gains, per MassMutual's whole life policy documentation

- Tax-free policy loans — for non-MEC policies, loans against cash value are generally not taxable events while the policy remains in force

- Income-tax-free death benefit — per IRS guidance under IRC Section 101(a), life insurance proceeds received by beneficiaries are generally not includable in gross income

Note: Tax treatment depends on individual circumstances. Consult a qualified tax advisor for guidance specific to your situation.

Potential for Dividends

Policies from mutual insurance companies may pay annual dividends — though these are never guaranteed. When they are paid, you can reinvest them as paid-up additions, which increases both the cash value and the death benefit.

No Premium Obligations in Retirement

By finishing payments during your peak earning years, you eliminate a recurring expense before transitioning to a fixed retirement income. Fewer financial obligations in retirement means more flexibility when you need it most.

Drawbacks of Limited Payment Whole Life Insurance

Higher Annual Premiums

Compressing a lifetime of premiums into 10, 15, or 20 years means each annual payment runs considerably higher than a traditional whole life equivalent. Before committing, ask yourself honestly whether those payments are sustainable through the full payment period — not just year one.

Modified Endowment Contract Risk

If too much money is paid into the policy within a set timeframe — as measured by the IRS 7-pay test — the policy can lose its favorable tax treatment. Once classified as a MEC:

- Cash value withdrawals and loans are taxed as ordinary income (gains-first)

- Taxable distributions before age 59½ may trigger an additional 10% penalty

- This treatment is governed by IRC Section 72

A knowledgeable advisor can structure premium payments to stay below MEC thresholds. This is not an obscure edge case — it's a real risk with limited pay policies, and it deserves attention during the planning stage.

Opportunity Cost

Beyond the MEC risk, the higher premium commitment has a second cost: opportunity cost. Dollars flowing into this policy aren't available for stocks, bonds, retirement accounts, or real estate. The cash value growth inside a whole life policy is guaranteed and tax-advantaged — but it operates differently from market-based returns. Whether that trade-off works in your favor comes down to your goals, risk tolerance, and how this policy fits within your broader financial plan.

How Much Does Limited Payment Whole Life Insurance Cost?

There's no single answer — premiums vary based on several factors. What matters is understanding what drives the number.

Key pricing factors:

- Age at purchase — younger buyers pay lower premiums; costs increase with age

- Health status — better health generally means lower premiums; conditions like smoking or chronic illness raise costs

- Death benefit amount — more coverage means higher premiums

- Payment period — shorter periods (7-pay vs. 20-pay) mean higher annual premiums for the same coverage

Gender also plays a role. According to CDC data from 2024, U.S. life expectancy at birth is 76.5 years for males and 81.4 years for females. Insurers factor these statistical differences into pricing, which means women often pay lower premiums than men for the same coverage.

Western & Southern describes a 10-pay scenario where $5,000 per year for 10 years totals $50,000 in premiums — one data point, not a market benchmark. Actual premiums depend on your specific age, health, and coverage needs.

Premiums for the same coverage can vary widely from carrier to carrier. Working with an independent advisor like Vellum Life Group — which shops across 15+ A-rated carrier partners — lets you compare real options and find pricing that reflects your actual health profile.

Who Is Limited Payment Whole Life Insurance Right For?

Strong Candidates

- Pre-retirees in peak earning years who can handle higher short-term premiums and want coverage fully paid off before retirement

- High-income earners seeking permanent coverage without an indefinite payment obligation

- Parents purchasing policies for children — premiums can be completed before the child reaches adulthood, leaving them with a paid-up permanent policy and decades of cash value growth ahead

When It May Not Be the Right Fit

| Situation | Better Option |

|---|---|

| Tight current cash flow | Term life insurance |

| Temporary coverage needs (mortgage, education years) | Term life insurance |

| Uncertain income stability | Traditional whole life or universal life |

| Need maximum death benefit per dollar of premium | Term life insurance |

Term life offers lower premiums and works well for covering specific financial obligations over a defined period. Limited pay whole life is better suited for permanent legacy goals, estate planning, or long-term wealth building — where the coverage needs to last a lifetime, not just a term.

The Value of Personalized Guidance

Because the right payment period and policy structure hinge on your income, health, retirement timeline, and goals, this decision benefits from someone who can run the actual numbers across carriers — not just explain the concept.

Vellum Life Group founder Eva Ikonomakos offers free consultations to help you evaluate whether limited payment whole life fits your situation. With access to 15+ A-rated carriers, she can compare structures side-by-side and identify the most competitively priced option for your health profile and budget.

Frequently Asked Questions

Can I get limited pay whole life insurance if I have a pre-existing condition such as cirrhosis, Parkinson's, or lupus?

Eligibility depends on the severity and stability of the condition and the specific carrier's underwriting guidelines. Some conditions result in higher premiums or a rated policy; others may disqualify applicants from fully underwritten policies. Simplified issue or guaranteed issue options may still be available. An independent advisor can compare multiple carriers to find the best available option for your situation.

What is the difference between limited payment whole life and traditional whole life insurance?

The core difference is the premium timeline. Limited payment whole life front-loads premiums into a set number of years (such as 10 or 20), while traditional whole life spreads lower payments across a lifetime. Both provide permanent coverage and cash value growth — limited pay simply eliminates premium obligations earlier.

Does limited payment whole life insurance build cash value?

Yes. These policies build cash value on a tax-deferred basis. Because premiums are higher and concentrated into fewer years, cash value typically grows faster in the early years compared to a traditional whole life policy with the same death benefit.

What happens if I can't afford my premiums during the payment period?

Most policies offer options such as an automatic premium loan (using cash value to cover the payment), a reduced paid-up conversion, or extended term insurance. These provisions vary by carrier and policy — review them with an advisor before a lapse occurs.

Is limited payment whole life insurance a good choice for retirement planning?

It can complement a retirement plan well — premiums end before or at retirement, and accumulated cash value can be accessed through policy loans, with tax-deferred growth and a tax-free death benefit for heirs. It works best alongside other retirement savings, not as a replacement for them.

Can I borrow against a limited pay whole life insurance policy?

Yes. Policyholders can borrow against the cash value at any time for any purpose, without credit approval. Unpaid loan balances accrue interest and will reduce the death benefit paid to beneficiaries if not repaid before death.