That's the appeal of VUL. It's powerful on paper. In practice, it's one of the most complex financial products you can own.

This guide breaks down how VUL works, what it costs, how it compares to other policy types, and how to honestly assess whether it fits your situation — or whether a simpler approach might serve you better.

Key Takeaways

- VUL is permanent life insurance — coverage stays in force for life, unlike term policies that expire

- Cash value is invested in market-based subaccounts, meaning it can grow significantly or lose value

- Premiums are flexible — you control the timing and amount within contract limits

- VUL suits people with high risk tolerance, long time horizons, and complex financial goals — not every policyholder

What Is Variable Universal Life (VUL) Insurance?

Variable universal life insurance is a type of permanent life insurance with two core functions: a death benefit paid to beneficiaries when the policyholder dies, and a cash value component that the policyholder can invest in market-linked subaccounts.

"Universal" refers to premium flexibility. Unlike whole life, which requires fixed scheduled payments, VUL allows policyholders to vary how much and when they pay — within minimum and maximum limits set by the insurer.

"Variable" refers to investment risk. Unlike standard universal life, where an insurer credits cash value at a set interest rate, VUL ties cash value directly to the performance of investment subaccounts the policyholder selects. There is no guaranteed return.

The Regulatory Dimension

VUL isn't regulated like a standard insurance product. Because of its investment component, FINRA classifies variable universal life as a security subject to both state insurance laws and federal securities regulations. Issuers must register policies under the Securities Act of 1933. Separate accounts holding investment assets must also register under the Investment Company Act of 1940.

This means any agent selling VUL must hold both a state insurance license and a FINRA securities registration — either a Series 6 or Series 7 credential.

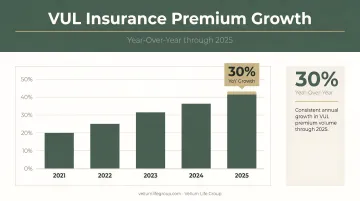

VUL new annualized premium reached $1.9 billion through the first nine months of 2025, up 30% year over year according to LIMRA — the strongest growth rate among permanent life insurance product categories tracked that period.

How Does VUL Insurance Work?

Every premium payment you make gets split two ways: a portion covers the cost of insurance (mortality charges, administrative fees), and the remainder flows into the policy's cash value. You then direct that cash value into investment subaccounts of your choosing.

Premiums and Payment Flexibility

Flexible premiums are one of VUL's defining features. You can pay more in strong income months and dial back during lean ones. Just stay within the policy's minimum and maximum limits.

A few important caveats:

- Paying the minimum keeps the policy active but may not build meaningful cash value

- Underfunding consistently — especially during market downturns — can erode cash value to the point where it can no longer cover ongoing insurance charges, triggering a lapse

- Policy lapse eliminates both the death benefit and any remaining cash value

- Overfunding too quickly can trigger Modified Endowment Contract (MEC) status under IRS Section 7702A, which changes how distributions are taxed (more on this in the Tax section)

Investment Subaccounts and Cash Value

Subaccounts function similarly to mutual funds inside the policy. Depending on the carrier, a single VUL policy might offer anywhere from a handful to over 100 options — stock funds, bond funds, index funds, and money market accounts among them.

You allocate across subaccounts based on your risk tolerance. How that allocation performs determines what happens next:

- If subaccounts perform well, cash value grows tax-deferred

- If subaccounts perform poorly, cash value declines — sometimes sharply

- Unlike whole life or standard universal life, there is no guaranteed minimum return on variable subaccounts

The investment risk sits entirely with the policyholder. As investor.gov notes, poor investment performance can reduce both cash value and the death benefit, and the policy may lapse if cash value becomes insufficient to cover ongoing charges.

VUL Insurance: Key Pros and Cons

VUL offers real advantages — but they come with equally real risks. Whether it works in your favor depends almost entirely on how the policy is structured and how markets perform over time.

Advantages of VUL Insurance

- Tax-deferred growth: Investment gains inside the policy accumulate without annual taxation. For a high-income earner, that compounding advantage over 20–30 years can be substantial. When structured correctly (and the policy isn't a MEC), loans against cash value are generally not treated as taxable income.

- Income tax-free death benefit: Under IRC Section 101(a), life insurance proceeds paid to a beneficiary at death are generally excluded from gross income. VUL also allows death benefit adjustments over time as needs change.

- Direct investment control: Policyholders choose how cash value is allocated across subaccounts — a level of control that whole life and standard universal life don't offer. In a sustained bull market, this can produce significantly higher cash value growth than fixed-rate alternatives.

Disadvantages of VUL Insurance

Market risk with no guaranteed floor Cash value can — and does — decline during poor market years. If losses are severe enough that cash value can't cover the policy's monthly charges, the policyholder must either inject additional premiums or watch the policy lapse, losing both the coverage and any remaining cash value.

High fees and complexity VUL policies carry multiple cost layers that compound over time:

- Mortality and expense (M&E) risk charges

- Administrative fees

- Subaccount management fees (expense ratios)

- Potential surrender charges — which in some policies can apply for up to 15 years

SEC-filed prospectuses from real VUL policies show underlying fund expense ratios ranging from 0.14% to 1.62% annually, on top of insurance-layer charges. These fees reduce net returns and require ongoing monitoring to ensure the policy performs as intended.

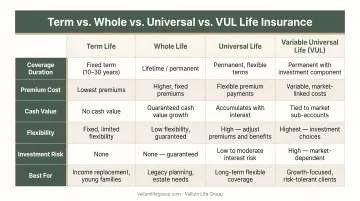

VUL vs. Other Life Insurance Types

VUL sits in a specific part of the life insurance landscape. Knowing where it fits helps clarify whether it's the right fit.

| Feature | Term Life | Whole Life | Universal Life (UL) | VUL |

|---|---|---|---|---|

| Coverage duration | Fixed term | Permanent | Permanent | Permanent |

| Premiums | Fixed | Fixed | Flexible | Flexible |

| Cash value | None | Guaranteed growth | Fixed/minimum rate | Market-linked |

| Investment control | None | None | None | Policyholder-directed |

| Return guarantee | N/A | Yes | Minimum floor | No |

| Complexity | Low | Medium | Medium | High |

VUL vs. Universal Life (UL) Both offer flexible premiums and adjustable death benefits. The difference is where cash value goes. UL credits cash value at a rate set or guaranteed by the insurer — typically tied to prevailing interest rates with a minimum floor. VUL removes that floor entirely and lets the market determine growth. Indexed universal life (IUL) sits between the two: growth is tied to a market index, but with a floor protecting against losses and a cap limiting upside.

VUL vs. Whole Life Whole life trades growth potential for certainty — fixed premiums, guaranteed death benefit, predictable (if modest) cash value accumulation. For someone who values knowing exactly what they'll get, whole life delivers that predictability where VUL cannot.

VUL vs. Term Term provides the lowest-cost death benefit with no cash value component. Someone who wants both insurance coverage and investment growth using term would need a separate investment account, which often proves more cost-efficient than VUL once you factor in fees.

Tax Benefits and Implications of VUL Insurance

Tax treatment is central to why VUL appeals to high earners. Three advantages drive most of the interest:

- Tax-deferred growth: Investment gains inside the policy aren't taxed annually, allowing compounding without an annual tax drag.

- Tax-free policy loans: Borrowing against cash value in a non-MEC policy that stays in force is generally not treated as taxable income.

- Income tax-free death benefit: Proceeds paid to beneficiaries under IRC Section 101(a) are excluded from gross income.

The Roth IRA Connection

High-income earners who exceed IRS income limits for Roth IRA contributions sometimes use VUL as a supplemental tax-advantaged vehicle. For 2025, Roth IRA contributions phase out between $150,000–$165,000 (single filers) and $236,000–$246,000 (married filing jointly), according to IRS Publication 590-A.

VUL carries no IRS income-based contribution limit comparable to the Roth IRA phaseout, and unlike qualified retirement plans, there are no required minimum distributions (RMDs). For someone blocked from Roth contributions who still wants tax-advantaged accumulation, VUL can fill that gap — though its fee structure means the comparison against other options matters.

The MEC Risk

Funding a VUL policy too aggressively in its early years can trigger Modified Endowment Contract (MEC) status under IRC Section 7702A. The IRS applies a "7-pay test": if cumulative premiums in the first 7 contract years exceed what would fully pay up the policy over 7 level annual payments, the contract becomes a MEC.

MEC status changes the tax treatment significantly.

The consequences:

- Distributions are taxed as income first (gains-out-first treatment under IRC 72(e)(10))

- Policy loans are treated as distributions

- Withdrawals before age 59½ may also incur a 10% additional tax

Crossing the 7-pay threshold is irreversible, so understanding exactly where that limit falls before making large early contributions is critical.

Is VUL Insurance Right for You?

VUL isn't a product most people need. But for the right profile, it can be genuinely valuable.

Who VUL Is Designed For

- Long time horizon — the fees only justify themselves over many years; investor.gov explicitly cautions that VUL is generally unsuitable as a short-term savings vehicle

- Higher risk tolerance — market-linked cash value means accepting real downside risk

- Need for permanent life insurance — if term coverage would suffice, VUL's added complexity rarely makes sense

- Already maximizing other accounts — VUL makes most sense after 401(k) and Roth IRA contributions are fully utilized

- High-income earners and estate planners — building legacy or wealth transfer strategies where a single tax-advantaged vehicle is attractive

Who Should Consider Alternatives

If any of these describe your situation, a simpler approach likely serves you better:

- You want guaranteed returns and predictable outcomes

- You're primarily focused on affordable death benefit coverage

- You have a short or medium time horizon (under 10 years)

- You're on a tight or variable income

For many people, term life insurance paired with a straightforward investment account delivers comparable outcomes at lower cost and complexity.

Working with the Right Advisor

Whichever direction you lean, VUL is a long-term commitment with real consequences if managed poorly — so the quality of advice matters. Vellum Life Group offers a free, no-pressure 30-minute consultation to help you think through whether VUL, or another permanent life insurance solution, actually fits your financial picture.

To get started:

- Book online: calendly.com/eva-ikonomakos/30min

- Call or text Eva: 917-363-3554

Frequently Asked Questions

Is variable universal life insurance a good product?

For the right person (high risk tolerance, long time horizon, complex financial needs), VUL can be a strong fit. For everyone else, the fees and complexity often outweigh the benefits. Its value depends entirely on individual goals and whether the growth potential justifies the costs.

What is the difference between universal life and variable universal life?

Universal life (UL) builds cash value at a rate set or guaranteed by the insurer, with a minimum floor; VUL directs that cash value into market-based subaccounts with no guaranteed return. VUL combines UL's flexible premiums with variable life's investment structure.

What happens to a VUL policy if the market crashes?

A significant market downturn can sharply reduce cash value. If cash value drops too low to cover the policy's ongoing insurance charges, the policyholder must pay additional premiums or risk the policy lapsing — which eliminates both the cash value and the death benefit entirely.

What are the typical fees in a VUL policy?

VUL carries multiple cost layers:

- Mortality and expense (M&E) charges

- Administrative fees

- Subaccount expense ratios

- Surrender charges (periods can run 10–15 years)

Based on SEC-filed prospectuses, underlying fund expense ratios range from roughly 0.14% to 1.62% annually, on top of insurance-layer charges.

Can you lose money with variable universal life insurance?

Yes. If the investment subaccounts you select perform poorly, your cash value declines. Unlike whole life or standard universal life, VUL provides no guaranteed minimum return on the variable investment portion.

Is VUL the same as an investment account?

No. VUL is a life insurance contract with an investment component, not a standalone investment vehicle. Insurance charges layered on top of subaccount expenses make it less efficient as a pure investment than a brokerage account or retirement plan — the tax advantages and death benefit are what set it apart.