This scenario plays out more often than most people realize. According to LIMRA's 2024 Insurance Barometer Study, 102 million Americans either lack life insurance or know they need more. Many of them have policies — they're just working with outdated ones.

Life insurance is not a "set it and forget it" product. A policy that fit your life five years ago may have serious gaps today. This guide explains what a policy review is, when to do one, and walks through a practical seven-step checklist covering every area that matters.

Key Takeaways

- Review your policy at minimum once per year — and immediately after any major life event

- Your checklist should cover coverage amount, beneficiaries, policy type, riders, premiums, and insurer financial health

- Outdated beneficiaries, under-coverage, and expiring term policies are the most damaging mistakes from skipped reviews

- Term and permanent policies both require reviews, but what to look for differs

- A licensed advisor can identify coverage gaps and cost savings that policy documents alone won't reveal

What Is a Life Insurance Policy Review?

A life insurance policy review is a structured evaluation of your existing coverage to confirm it still matches your current financial situation, family responsibilities, and long-term goals.

The purpose is not to sell you something new. It is to ask one honest question: is what you have still doing the job it was meant to do?

There are two distinct types of reviews, and both matter:

- Annual check-in — Verify that beneficiaries are current, premiums are paid, and no riders have lapsed. Takes 30–60 minutes and should happen every year without exception.

- Needs reassessment — A deeper recalculation triggered by a major life change. This involves re-running your coverage numbers based on new debts, income, dependents, or health circumstances.

At Vellum Life Group, Eva Ikonomakos builds both types into her ongoing client relationships, included at no additional cost after a policy is placed. A policy written five years ago reflects five-year-old circumstances — regular reviews are what close that gap.

When Should You Review Your Life Insurance Policy?

Life Happens recommends reviewing your life insurance with a financial professional at least once a year. Tying it to a consistent date — your policy anniversary, open enrollment season, or the start of the year — makes it easier to build as a habit.

That said, an annual review is the minimum. Several categories of life changes should prompt an immediate out-of-cycle review:

| Life Change Category | Examples |

|---|---|

| Family | Marriage, divorce, new child, adoption, aging parent as dependent |

| Financial | New mortgage, debt payoff, major income increase or loss |

| Health | New diagnosis, quitting smoking, significant weight loss |

| Career | Job change, income change, new financial responsibilities |

The Gradual Change Problem

Not every coverage gap starts with a dramatic event. Gradual changes — a pay raise, a child approaching college age, elderly parents becoming financially dependent — can erode a policy's adequacy over time. A policy that covered your obligations at 35 may fall well short at 43 even if nothing significant changed in a given year.

Life Events That Should Trigger an Immediate Policy Review

Marriage and Divorce

Marriage often means a new financially dependent partner — coverage that made sense for a single person with no dependents now needs to account for shared income, shared debt, and a spouse who may rely entirely on your income.

Divorce creates a different but equally urgent problem. An ex-spouse who remains on a beneficiary designation can legally receive the death benefit — regardless of your intentions.

In Sveen v. Melin, the U.S. Supreme Court addressed exactly this scenario: Mark Sveen had not updated his beneficiary designation after divorcing in 2007, and competing claims followed his death in 2011. Some states have revocation-on-divorce statutes, but coverage issued in other states may not be protected. The only reliable fix is updating the designation directly.

New Children or Dependents

The arrival of a child — biological, adopted, or otherwise — fundamentally changes the financial obligation your policy must cover. A rough estimate of added coverage need should include:

- Income replacement for the years until that child is financially independent

- Anticipated education costs

- Childcare or caregiving expenses if a surviving parent would need support

Taking on an aging parent as a dependent requires the same calculation. If your policy hasn't been updated since that responsibility began, the gap between what you have and what you need is worth closing now.

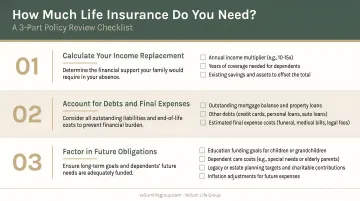

Major Financial Shifts

Coverage needs move in both directions. Two common scenarios to check against your current policy:

- Increased debt (a new mortgage, personal loan): your death benefit should cover what a surviving spouse can't carry alone

- Reduced obligations (paid-off debt, financial independence): you may be paying premiums on more coverage than your situation still requires

Health Changes

Improved health — quitting smoking, meaningful weight loss, a resolved medical condition — can qualify you for reclassification at lower premiums. One carrier example: tobacco users pay an average of 75% more than non-smokers, roughly $2,000 more annually. Some carriers will reconsider rates after two smoke-free years.

A new serious diagnosis doesn't affect your existing in-force policy, but it makes reviewing your current riders and any conversion options especially urgent before coverage gaps emerge.

Career and Business Changes

For individuals with estate plans or complex financial arrangements, a personal policy review should consider all outstanding obligations and how coverage aligns with current goals — as values, responsibilities, and structures can shift over time.

Your Life Insurance Policy Review Checklist

Work through each of these items once a year — or immediately after a triggering life event.

Step 1: Verify Your Coverage Amount

Start with the most fundamental question: does your death benefit still cover what it needs to?

A practical calculation includes:

- Outstanding debts — mortgage balance, auto loans, student loans, credit cards

- Income replacement — number of years dependents need support × annual income

- Future costs — college funding, eldercare, final expenses

As a starting point, Life Happens suggests 10 to 15 times gross income, adding approximately $100,000 per child for education costs. NAIC notes that some experts use 5 to 8 times income, but recommend calculating based on your specific obligations rather than any single rule of thumb.

For term policies: confirm the policy won't expire before your dependents are self-sufficient. A 20-year term taken out when your child was two expires when they're 22 — fine if your obligations end there, but a real gap if they don't.

For permanent policies: check whether the death benefit has kept pace with your financial growth. If the policy has a cash value component, request an in-force illustration to see current values versus original projections.

Step 2: Review Your Beneficiary Designations

This is the single most legally consequential item on the checklist. A will alone does not control where life insurance proceeds go — the beneficiary designation on the policy controls the payout, subject to applicable state law.

Verify the following:

- Primary beneficiary — reflects your current relationship status, including any changes from marriage or divorce

- Contingent beneficiary — named and current (what happens if the primary beneficiary predeceases you?)

- Minor children — the NAIC's Life Insurance Buyer's Guide advises against naming a minor child directly, because insurance companies will not pay a minor. If minor children need to be protected, use a trust or custodian arrangement

Update this annually. It takes minutes and prevents the kind of dispute that ends up in court.

Step 3: Examine Policy Type and Term Status

For term policies:

- Check the expiration date — does coverage extend until your mortgage is paid off and children are independent?

- Look for a conversion option — most term policies allow conversion to a permanent policy without new medical underwriting, but there is a deadline. Once that window closes, it cannot be reopened

- Note that lapse rates spike significantly near the end of level-term periods, often because policyholders forget to act before rates reset

For permanent policies:

- Request an in-force illustration from your carrier — this shows current cash value, projected values, and whether the policy is at risk of lapsing based on actual performance

- If the policy has an investment component (variable universal life, for example), check whether poor market performance has eroded the cash value below what's needed to sustain coverage

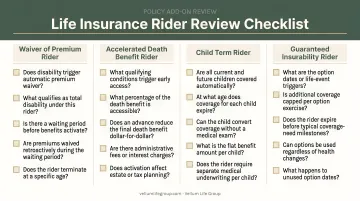

Step 4: Assess Riders and Add-On Coverage

Riders are amendments that expand or restrict what your policy covers. Review each one you have — and consider what you're missing.

| Rider | What to Check |

|---|---|

| Waiver of Premium | Still active? Still needed given current disability coverage? |

| Accelerated Death Benefit | Does a new health situation make this more relevant now? |

| Guaranteed Insurability | Has the option window to add coverage without underwriting passed? |

| Critical Illness | Does it cover the specific conditions most relevant to your health history? |

Flag anything that overlaps with existing coverage — and anything you've lost. A disability income rider may duplicate group benefits you now have, or it may be more essential than ever if that group coverage is gone.

Step 5: Check Premium Costs and Insurer Health

Once you've reviewed your coverage and riders, the final step is cost and carrier stability — two factors that directly affect whether your policy delivers when it needs to.

Premium competitiveness: If your health has improved since you were originally underwritten, you may qualify for better rates — through reclassification with your current carrier or by applying elsewhere. Do not cancel an existing policy before a new one is confirmed and active.

Insurer financial stability: Look up your carrier's rating through AM Best. Their scale for financially secure insurers runs from B+ (Good) up through A++ (Superior). A-rated carriers (A-, A, A+, A++) fall in the Excellent to Superior range. Vellum Life Group works exclusively with A-rated carriers, so clients always know their coverage is backed by financially sound insurers.

What if an insurer fails? Life and health guaranty associations exist in all 50 states and the District of Columbia. They provide a backstop when an insurer becomes insolvent — but coverage limits apply, typically $300,000 in death benefits under the NAIC model act (actual limits vary by state). The stronger your carrier's rating, the less likely you'll ever need that backstop.

Common Policy Review Mistakes to Avoid

Never Reviewing at All

The NAIC found that 31% of policyholders had reviewed their policies more than a year ago — and that's among those who had reviewed at all. Many others have never looked at the policy since they bought it.

The compounding result: an outdated beneficiary, an expiring term, and a death benefit half of what the family actually needs — discovered only when it's too late to fix any of them.

Replacing a Policy Based Only on Price

Reducing premiums is a legitimate goal during a review. But replacing a policy purely for cost — without verifying continuous coverage and comparable benefits — can backfire badly. Replacement triggers consequences many policyholders don't anticipate:

- New underwriting applies: if your health has changed, you may not qualify for the same rate class

- The contestability period resets: typically two years, during which the insurer can contest a claim

- Start-up costs restart: California's Department of Insurance specifically warns about this, noting a one-to-two year window before the new policy fully clears

The rule: never cancel existing coverage until a replacement policy is issued and active.

Skipping Professional Guidance

A self-review can catch obvious issues — an outdated beneficiary, a lapsed rider. What it cannot do is compare your current policy against what's available across 15+ carriers today.

A licensed advisor can check whether your coverage is still competitive, whether a health improvement qualifies you for better terms, and whether riders you didn't know existed would close gaps in your current protection. Vellum Life Group offers a free, no-obligation consultation for exactly this — comparing your existing policy against today's market at no cost to you.

Frequently Asked Questions

What is a life insurance policy review?

A life insurance policy review is a structured evaluation of your existing coverage to confirm the death benefit, beneficiary designations, policy type, and riders still align with your current financial situation and life circumstances. The goal is confirmation — making sure what you have still does what you need it to do.

How do medical conditions or medications affect my ability to get life insurance?

A new medical condition diagnosed after your policy was issued does not affect your existing in-force coverage. However, it can affect eligibility or rates if you apply for new or additional coverage — which is exactly why reviewing existing riders like accelerated death benefits should happen before any lapse or cancellation.

How often should you review your life insurance policy?

Annual reviews are the baseline. Beyond that, any major life event warrants a closer look — marriage, divorce, a new child, a significant income change, a new debt obligation, or a meaningful health change in either direction.

What happens if I never review my life insurance policy?

An outdated beneficiary designation could send the payout to the wrong person. A term policy could expire unnoticed, leaving dependents unprotected. Years of income growth and new obligations can also create gaps that leave a surviving family unable to maintain their standard of living.

Can I change my life insurance policy after a major life event?

Beneficiary changes can typically be made at any time. Increasing coverage or adding riders may require new underwriting. Acting sooner matters. Health changes over time, and coverage that's available today may not be available after a new diagnosis.

What should I look for when reviewing my life insurance beneficiaries?

Confirm primary beneficiaries reflect current relationships, especially after marriage or divorce. Make sure contingent beneficiaries are named. If children are minors, do not list them directly — use a trust or custodian arrangement to ensure the proceeds are properly managed on their behalf.