](https://file-host.link/website/vellumlifegroup-yscwum/assets/refined-images/1781692583232000_f388af92d23d4b428e6acb45c10654f6/360.webp)

According to LIMRA's 2024 Life Insurance Fact Sheet, 102 million American adults say they need life insurance or need more of it — and 72% overestimate what basic term coverage actually costs. The right independent agent closes that gap. The wrong one just adds to it.

This article walks you through exactly what to look for, what questions to ask, and which warning signs to take seriously.

Key Takeaways

- An independent agent represents multiple carriers and shops coverage across all of them (unlike a captive agent, who can only sell one company's products)

- Verify any agent's license through the NIPR National Producer Number lookup before sharing personal or health information

- Strong agents partner with A-rated carriers, explain compensation openly, and stay available long after the policy is issued

- Limited carrier access, high-pressure sales tactics, and evasiveness about credentials are clear red flags

What Is an Independent Life Insurance Agent?

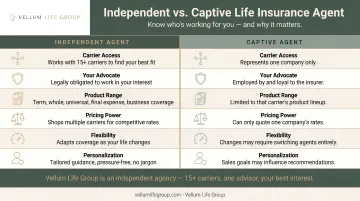

An independent life insurance agent is a licensed professional who represents multiple insurance carriers, compares policies across them, and recommends coverage based on your individual needs — not on the interests of any single company. They are appointed by multiple insurers, which means they can genuinely shop the market on your behalf.

A captive agent, by contrast, is contracted with one insurer and can only sell that company's products. Captive agents may know their carrier's offerings well, but they cannot compare rates or coverage structures across the broader market. For someone with a specific health history, a tight budget, or a complex coverage goal, that limitation matters.

Independent agents accounted for 54% of individual life insurance new annualized premium in 2022, according to ACLI's Fact Book — making them the dominant distribution channel in individual life insurance sales.

How Compensation Works

Independent agents earn a commission from the carrier whose policy is placed. That commission does not typically add to your premium — the carrier builds it into their pricing structure. The key question is whether your agent discloses this arrangement openly and whether their carrier portfolio is broad enough that commission incentives don't steer you toward the wrong product.

A straightforward question covers both concerns: "Are you paid by commission or fee, and would your compensation change if I chose a different carrier?"

What to Look For When Choosing an Independent Life Insurance Agent

Selecting the right agent goes beyond confirming they have a license. These are the qualities that separate an agent who truly serves your interests from one who simply sells you something.

Verified Licensing and Credentials

Every agent who sells life insurance must hold a valid life insurance producer license in your state. Verify this yourself before sharing any personal or health information — it takes under two minutes.

- Go to NIPR's NPN lookup tool and enter the agent's National Producer Number

- Cross-reference with your state's Department of Insurance website

- Confirm the license is active and covers life insurance as a line of authority

Professional designations like the CLU (Chartered Life Underwriter) or ChFC (Chartered Financial Consultant) signal additional investment in expertise, particularly around estate planning and complex coverage structures. They supplement — but never replace — a valid state license.

Carrier Access and Diversity

How many carriers an agent works with directly shapes what they can offer you. An agent appointed with only one or two carriers can't realistically shop the market — which means limited rate options, fewer accommodations for health conditions, and a narrower range of policy types.

Ask:

- How many carriers are you appointed with?

- Do they hold strong financial strength ratings from AM Best? (A or A- means Excellent; A+ and A++ mean Superior)

- Did you actively compare those carriers for my situation, or do you tend to favor one?

The goal is not a specific number of carriers — it's evidence that the agent genuinely shopped the market and can explain why they recommended one option over the others they had access to.

Specialization in Life Insurance and Legacy Planning

Life insurance involves nuanced decisions: policy type (term, whole, universal, final expense), coverage amount, beneficiary structure, and in many cases, estate or legacy considerations. These decisions benefit from an agent whose primary focus is life insurance — not someone who treats it as a side product alongside auto, home, and health coverage.

Ask whether the agent has specific experience with your situation:

- Families with young children needing income replacement

- Individuals seeking legacy or estate planning coverage

- Applicants with pre-existing health conditions

- Legacy or estate planning needs

An agent who works in this space daily will know which carriers are more flexible on health history, which policy structures fit your income goals, and where the real tradeoffs are — before you're deep into underwriting.

Transparency Around Compensation and Process

A trustworthy agent explains upfront:

- How they are paid and by whom

- What the underwriting process involves and how long it typically takes

- Which factors affect your premium (age, health status, coverage amount, policy type)

- What the policy terms actually mean in plain language

Evasiveness on any of these points is a warning sign. Clients who don't fully understand their coverage risk being underinsured, overpaying, or holding a policy that doesn't serve their actual needs.

Long-Term Support and Ongoing Service

A life insurance policy isn't a one-time transaction. Marriage, new children, a health change, or new financial responsibilities — these all affect whether your existing coverage is still adequate.

The NAIC recommends reviewing your life insurance coverage every few years — or whenever a major life event changes your financial picture.

Look for agents who:

- Conduct annual or periodic policy reviews

- Reach out proactively when life changes warrant a reassessment

- Provide guidance through the claims process, not just at the point of sale

Ongoing service is where independent agents earn their value — because your coverage needs to grow with you, not stay frozen on the day you signed.

Red Flags to Watch Out For

Some behaviors indicate an agent is not working in your best interest. Watch for these warning signs:

- Pushes one policy without presenting alternatives — a genuinely independent agent can show you what they compared and why they chose what they recommended

- Rushes the application process or discourages questions about policy details

- Claims to have "the best rates" without comparative evidence — broad carrier access should come with proof of comparison, not just a claim

- Won't provide their NPN or license number — any licensed producer should offer this without hesitation

- Pressures policy replacement without written explanation — NAIC's Replacement Model Regulation warns that replacing a life policy can restart contestability periods, trigger surrender charges, and increase premiums due to your current age

Verify licensure every time. Use your state's Department of Insurance website or the NIPR lookup tool — and don't proceed with any agent who hesitates to share their credentials.

How Vellum Life Group Can Help

Vellum Life Group was founded by Eva Ikonomakos, who brings over 15 years of experience across financial services, healthcare, and international business. Her healthcare background helps her navigate medical underwriting with clarity; her financial services foundation informs her legacy and coverage planning guidance. She built Vellum Life Group specifically to offer the kind of thoughtful, personalized support that most insurance experiences don't provide.

Here's how Vellum delivers on each criterion covered in this guide:

- Appointed with 15+ A-rated carriers — including Mutual of Omaha, Transamerica, Corebridge Financial, Ameritas, and Foresters Financial — and actively shops across them to find the best fit for each client's health profile and goals

- Runs a pressure-free, jargon-free process paced to your comfort, walking you through every step until you feel fully confident in your decision

- Provides ongoing support after every policy is placed: annual reviews, life-change reassessments, beneficiary updates, and claims assistance

- Responds to all new inquiries within 24 hours

Vellum Life Group has protected 500+ families and written more than $50 million in coverage, and is licensed to serve clients nationwide. Eva's NPN (21474735) is publicly verifiable through the NIPR database.

A free, no-obligation consultation is available at any time — reach Eva at 917-363-3554, info@vellumlifegroup.com, or by booking directly at calendly.com/eva-ikonomakos/30min.

Frequently Asked Questions

What does an independent life insurance agent do?

An independent agent represents multiple insurance carriers, compares policies across them, and recommends coverage tailored to your health profile, budget, and financial goals. Unlike a captive agent tied to one company, they work in your interest rather than any single insurer's.

Can you get life insurance if you have a serious medical condition?

Many people with serious medical conditions can qualify for life insurance, though eligibility and rates vary significantly by carrier. An independent agent's access to multiple carriers is especially valuable here — some carriers specialize in or are more flexible with higher-risk applicants, and an experienced agent knows where to place your application.

What is the difference between an independent and a captive life insurance agent?

A captive agent is contracted with a single insurance company and can only sell that company's products. An independent agent works with multiple carriers and can compare options across the market to find the policy that genuinely fits your situation.

How is an independent life insurance agent paid?

Independent agents earn a commission from the carrier whose policy is placed. This commission is built into the carrier's pricing and doesn't add to your premium. A trustworthy agent will disclose this arrangement openly and answer follow-up questions without hesitation.

How many insurance carriers should a good independent agent work with?

There's no fixed rule, but access to 8 or more A-rated carriers generally means better ability to shop competitively across health profiles and coverage needs. What matters just as much: can the agent show you which carriers they compared and explain why they recommended one over another?

Do I need an independent agent, or can I buy coverage directly?

Buying directly from a carrier is possible, but it limits you to that company's products and pricing. An independent agent compares options across the market, guides you through underwriting, and provides ongoing support — none of which a direct purchase typically includes, especially if your health history or coverage needs are complex.