For couples with significant assets, the real cost of wealth transfer often doesn't appear until both spouses are gone. That's when estate taxes come due, settlement costs accumulate, and heirs face a hard choice: sell the property, farmland, or the investment portfolio — or find another way to fund what's owed.

Survivorship life insurance exists precisely for that moment. This article explains how it works, the specific estate planning advantages it creates, where it falls short, and how to structure it so those advantages actually hold.

Key Takeaways

- Survivorship life insurance covers two lives under one policy and pays out only after both insureds have passed — designed for wealth transfer, not income replacement

- The death benefit covers estate taxes and settlement costs without forcing heirs to sell illiquid assets under pressure

- ILIT ownership removes the death benefit from the taxable estate and controls distribution to heirs

- Premiums are generally lower than two separate individual permanent policies covering the same two lives

- Correct structure determines the policy's value: ownership, trust design, and beneficiary designations must all work together

What Is Survivorship Life Insurance?

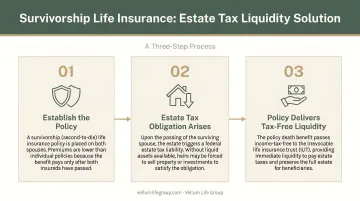

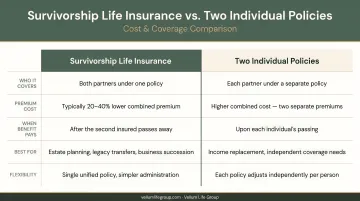

Survivorship life insurance — commonly called second-to-die insurance — is a single permanent life insurance policy that covers two people, typically spouses, and pays one death benefit only after both have died. New York Life describes it as joint life insurance where one policy covers two people with proceeds payable after both pass.

This policy is built for a specific purpose — and it's not income replacement. When the first spouse dies, the policy pays nothing. The surviving spouse receives no proceeds and no mortgage coverage; individual policies handle those needs.

The survivorship policy's purpose is narrower: deliver a lump sum at the moment estate transfer costs come due, which is after the second death.

Estate-planning survivorship policies are generally issued as permanent life insurance. MassMutual notes that these policies are commonly issued as whole life, universal life, or variable universal life. Coverage spans two full lifetimes, and long-term cash value accumulation is often part of the strategy — which is why term coverage rarely fits this application.

Key Estate Planning Advantages of Survivorship Life Insurance

The advantages here are practical and measurable. Each one solves a specific, predictable problem that arises when wealth moves across generations.

Advantage 1: Providing Liquidity for Estate Taxes and Settlement Costs

Without liquid assets available, large estates create a painful timing problem for heirs.

The IRS sets the 2026 federal estate tax basic exclusion amount at $15,000,000 per individual. For married couples, a surviving spouse can preserve the deceased spouse's unused exclusion through a portability election, creating a combined planning amount of up to $30,000,000. Estates that exceed those thresholds face a 40% marginal federal estate tax rate on the excess, and Form 706 is generally due within nine months of death.

Nine months sounds like breathing room. For families whose wealth is tied up in real estate, farmland, or a concentrated investment portfolio, it often isn't.

When heirs need to raise cash quickly to meet a tax deadline, forced asset sales are the default. Academic research on estate settlement sales found that real estate sold under time pressure averaged an 8.9% discount versus comparable properties — a loss that compounds on top of the tax bill itself.

Survivorship life insurance resolves this directly:

- The death benefit arrives as a lump sum after the second death — exactly when estate tax liability is calculated and due

- Proceeds cover taxes and settlement costs without requiring the sale of any core estate asset

- Heirs avoid both the tax obligation and the secondary loss from selling under pressure

This advantage matters most for estates that exceed or are approaching the federal exemption threshold, and for families whose primary wealth is held in real estate, farmland, or assets that cannot be easily liquidated.

Advantage 2: Preserving Wealth and Equalizing Inheritances Among Heirs

Dividing an estate fairly is straightforward when most assets are liquid. It becomes genuinely difficult when one heir inherits the family farm or property and another inherits significantly less simply because the estate lacked distributable cash.

A LegalShield study reported by InvestmentNews found that 58% of respondents experienced family disputes and assets falling under court control due to inadequate estate planning. Illiquid family assets add another layer of complexity, and studies consistently find that only a fraction of families with complex estates have a robust succession plan in place.

Survivorship life insurance creates a practical solution: structure the policy so that the heir who receives the property or illiquid asset gets it intact, while other heirs receive an equivalent cash payout from the death benefit. The estate transfers without forced division or buyouts, and the distribution is equitable even when the underlying assets aren't divisible.

Additional applications worth noting:

- Special needs planning: Survivorship proceeds can fund a special needs trust (SNT) for a disabled child, providing financial support after both parents are gone without disqualifying the child from SSI or Medicaid benefits — as long as the trust is properly drafted to avoid giving the beneficiary withdrawal rights over trust assets

- Blended families: The policy can be structured to ensure children from prior relationships receive their intended share alongside children from the current marriage

- Business succession: One heir takes operational control; other heirs receive equivalent value in cash

Families with illiquid assets, non-divisible property, or a child with long-term care needs will find this the most actionable advantage of survivorship coverage.

Advantage 3: Cost-Efficient Coverage Structured for Long-Term Estate Goals

Because a survivorship policy covers two lives and defers the payout until the second death, the insurer is pricing risk across a longer combined life expectancy. Protective confirms that survivorship coverage is often less expensive than two separate individual policies, and MassMutual notes that it can provide a larger benefit for the same premium.

Two additional cost-related advantages:

- Health disparities between spouses: If one spouse has a condition that would make individual coverage difficult or prohibitively expensive, a survivorship policy may still be obtainable based on the healthier spouse's profile. Protective notes that someone disqualified from an individual policy due to a medical condition may still qualify for survivorship coverage — a meaningful access advantage many couples overlook

- Adjustable structure over time: Universal life survivorship policies allow premiums and death benefit amounts to be modified as the estate grows or planning priorities shift

Any premium savings can be redirected to fund an ILIT, increase the death benefit, or reinforce other estate planning vehicles — extending the value of the same dollar in multiple directions.

When a Survivorship Life Insurance Policy Falls Short

Survivorship life insurance is built for a specific job: funding an estate transfer after both spouses are gone. Outside that context, it leaves real gaps — and a few common planning mistakes can quietly erase its core benefits.

Here are the limitations worth knowing before you structure a policy:

1. It pays nothing at the first death. The surviving spouse receives no benefit when their partner dies. If they need income replacement, mortgage coverage, or help with ongoing expenses, those needs require individual policies. Survivorship coverage and individual coverage solve different problems — most estate plans need both.

2. Wrong ownership structure pulls the death benefit into the taxable estate. Under IRC Section 2042, life insurance proceeds are included in the gross estate if the decedent held incidents of ownership at death. A policy owned personally by the insured couple may cancel out the very tax benefit it was purchased to provide. Transferring an existing policy to an ILIT triggers a three-year lookback rule under IRC Section 2035, so ownership must be structured correctly from day one.

3. Divorce leaves the policy in limbo. A joint survivorship policy does not automatically dissolve when a marriage ends, both parties may remain bound by its terms, with open questions about who pays premiums and who receives proceeds. Ownership, beneficiary designations, and premium responsibility all need legal review as part of any divorce process.

4. Waiting too long to buy raises costs and limits options. Purchasing at older ages significantly increases premiums and can make coverage harder to qualify for, which shrinks flexibility when you most need it in estate planning.

How to Structure a Survivorship Policy for Maximum Estate Planning Value

The policy's tax and distribution advantages depend almost entirely on how it is owned and structured. A survivorship policy owned directly by the insured couple can be effective at creating liquidity — but the death benefit may land inside the taxable estate, where it reduces rather than solves the estate tax problem.

ILIT Ownership: The Standard Structure

An irrevocable life insurance trust (ILIT) owns the policy, pays the premiums, and receives the death benefit, keeping proceeds outside the taxable estate and controlling how distributions reach heirs. The FPA Journal notes that the grantor should not pay premiums directly to the insurer; instead, the ILIT trustee pays premiums using gifts made to the trust. Those gifts typically use Crummey withdrawal rights so they qualify as present-interest gifts for annual gift tax exclusion purposes.

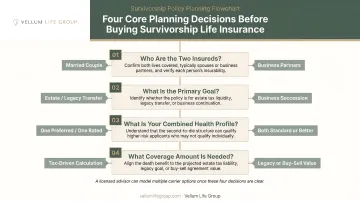

Core Decisions Before Purchasing

When integrating a survivorship policy into an estate plan, these decisions need answers before a policy is placed:

- Identify the primary purpose — estate tax coverage, inheritance equalization, special needs trust funding, or charitable giving

- Determine ownership structure — personal ownership vs. ILIT, with the tax consequences of each understood

- Select policy type — whole life for premium certainty and guaranteed cash value; universal life for flexible premiums and adjustable death benefit

- Set the coverage amount — based on projected estate tax liability, equalization gap, or special needs funding requirement

Plan for Change

These decisions aren't one-time choices. A 2025 CFP Board survey found that 88% of CFP professionals said clients' financial objectives faced substantial risks from expiring TCJA provisions, with 53% identifying legacy planning as a primary concern.

The current IRS basic exclusion amount is $15,000,000 for 2026. As an estate grows, family circumstances shift, and tax law evolves, coverage needs, ownership structures, and trust arrangements may all need revisiting.

Working with an independent advisor like Vellum Life Group gives families access to multiple A-rated carriers, making it easier to compare policy structures, premium profiles, and underwriting options and find the right fit as circumstances change.

Conclusion

Survivorship life insurance solves one problem well: it delivers liquidity at the moment it is needed most, after both spouses are gone, to protect what the family spent decades building. Whether the estate planning goal is covering federal estate taxes, equalizing inheritances among heirs, or funding a special needs trust, the policy provides a predictable, tax-efficient source of cash when the estate's other assets cannot easily be converted.

That value compounds when the policy is structured correctly and reviewed as circumstances evolve. The key structural elements are:

- ILIT ownership to keep the death benefit outside the taxable estate

- Coordinated beneficiary designations aligned with the overall estate plan

- The right policy type matched to the estate's current stage and long-term goals

Families exploring whether a survivorship policy fits their estate plan can reach out to Vellum Life Group for a no-pressure consultation and access to coverage options across 15+ carrier partners.

Frequently Asked Questions

How are survivorship life insurance policies helpful in estate planning?

Survivorship policies pay a lump-sum death benefit after both spouses pass, giving heirs funds to cover estate taxes and final costs without being forced to sell property or other illiquid assets. The proceeds arrive precisely when estate transfer costs come due — it's a liquidity tool, not an income replacement tool.

What type of life insurance is best for estate planning?

Survivorship (second-to-die) permanent life insurance is typically most effective for estate transfer goals, while individual permanent policies address income replacement and surviving spouse support. The right choice depends on whether the primary goal is protecting the surviving spouse financially or transferring wealth intact to the next generation.

Can you get a survivorship life insurance policy if one spouse has health issues?

Survivorship policies are often more accessible when one spouse has health challenges, because the insurer evaluates combined risk across two lives rather than one. This makes it possible to obtain coverage in situations where an individual policy for the less healthy spouse would be difficult or expensive to qualify for.

Is the death benefit from a survivorship life insurance policy subject to estate or income tax?

Death benefits are generally received free of federal income tax under IRC Section 101(a)(1). However, if the insured individuals own the policy, proceeds may be included in the taxable estate under IRC Section 2042. Holding the policy inside an ILIT is the standard approach for keeping the death benefit outside the taxable estate.

What is an ILIT and why does it matter for a survivorship policy?

An irrevocable life insurance trust (ILIT) owns the policy and receives the death benefit, keeping proceeds outside the taxable estate and controlling how distributions reach beneficiaries. Without ILIT ownership, the death benefit can be pulled back into the estate, which undermines much of the policy's estate planning value.

What happens to a survivorship life insurance policy if the couple divorces?

Divorce does not automatically terminate a survivorship policy, and both individuals may remain bound by its terms — including premium payments. Ownership, premium responsibility, and beneficiary designations must be reviewed and restructured as part of the divorce process, ideally with guidance from both legal counsel and an insurance advisor.