Burial insurance — also called final expense insurance — exists specifically to prevent that scenario. It's a small whole life policy designed to cover end-of-life costs, and it's one of the simplest financial protections a Minnesota family can put in place.

This guide covers how burial insurance works, the two main policy types available in Minnesota, what coverage costs, what funerals actually cost here, and the state laws that protect you as a consumer.

Key Takeaways

- Burial insurance is permanent whole life coverage with no medical exam, fixed premiums, and death benefits typically between $2,000 and $50,000

- A traditional Minnesota burial averages over $8,700 — burial insurance keeps that bill off your family's plate

- Two policy types to know: simplified issue (health questions asked, no waiting period) and guaranteed issue (no health questions, 2-year waiting period)

- A 65-year-old woman can pay roughly $41–$50/month for $10,000 in coverage; men pay slightly more

- Minnesota law guarantees a 10-day free look period and protects your family's right to choose any licensed funeral provider

What Is Burial Insurance and How Does It Work?

Burial insurance is permanent whole life insurance with a death benefit typically between $2,000 and $50,000. Premiums never increase, the policy never expires, and unlike term insurance — which ends after a set period — coverage stays active for the insured's entire life as long as premiums are paid.

The Payout

When the insured passes away, the named beneficiary receives a tax-free lump sum payment. There are no restrictions on how the money gets used. The family can apply it toward:

- Funeral and burial costs

- Outstanding medical bills or hospice expenses

- Credit card debt or small loans

- Probate fees or other final expenses

The beneficiary decides how to allocate the funds based on what the family actually needs at that moment.

Applying Is Simple

No medical exam is required. Most applications involve either a short health questionnaire or no health questions at all. Many policies are approved the same day or within a few business days.

Key facts about the application process:

- No medical exam required

- Short health questionnaire or no health questions at all

- Same-day or within-a-few-business-days approval common

- Coverage begins quickly, with no waiting period on many plans

Cash Value: A Built-In Benefit

As a whole life policy, burial insurance also builds cash value over time. Policyholders can borrow against this value during their lifetime if needed, though doing so may reduce the death benefit if the loan isn't repaid.

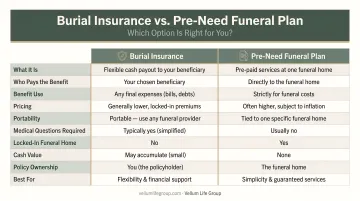

Burial Insurance vs. Pre-Need Funeral Plans

These are not the same product, and the distinction matters.

| Feature | Burial Insurance | Pre-Need Funeral Plan |

|---|---|---|

| Who receives the payout | Named beneficiary | Specific funeral home |

| Flexibility | Full — any expense | Locked to pre-selected services |

| Portability | Follows the beneficiary | Tied to one funeral provider |

| Regulated by | Insurance law | Funeral home contracts |

Under Minnesota Statute 72A.325, no insurer or agent may designate a specific funeral home as the required beneficiary in a way that removes the family's right to choose their provider. Burial insurance, paid directly to the beneficiary, keeps that freedom intact.

Types of Burial Insurance Available in Minnesota

Simplified Issue Burial Insurance

Simplified issue policies ask a short series of health questions during the application process. If your answers meet the carrier's underwriting criteria, coverage begins immediately — no waiting period.

This is the right starting point for most Minnesota residents. Applicants in reasonably good health can expect lower premiums, full coverage from day one, and approval often within 24 hours. You'll typically qualify if you haven't had recent hospitalizations, a recent cancer diagnosis, or a terminal illness.

Conditions that may result in a declined application or modified benefit offer include:

- Active hospice care

- End-stage renal disease

- Recent heart attack or stroke

In those cases, guaranteed issue becomes the practical option.

Guaranteed Issue Burial Insurance

Guaranteed issue policies accept every eligible applicant. No health questions, no medical exam, no possibility of being turned down based on health status.

The trade-off is a 2-year waiting period for natural-cause deaths. If the insured passes away from natural causes within the first two years, the beneficiary receives a refund of all premiums paid plus 10% interest — not the full death benefit. Accidental death is typically covered in full from day one.

This option is well-suited for Minnesota residents living with serious pre-existing conditions:

- COPD or advanced emphysema

- Recent heart attack or stroke

- Kidney disease requiring dialysis

- Active cancer treatment

One practical note: guaranteed issue policies cost more per dollar of coverage than simplified issue, because the insurer accepts higher-risk applicants without screening. Always try simplified issue first. Many applicants with manageable health histories qualify for better coverage at a meaningfully lower premium.

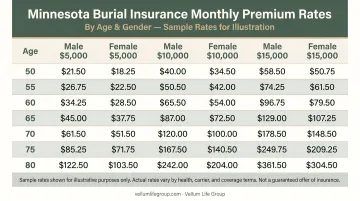

How Much Does Burial Insurance Cost in Minnesota?

Several factors drive your premium: age at application, gender, tobacco use, coverage amount, and policy type. Age carries the most weight — the younger you apply, the lower your fixed rate stays for the life of the policy.

Sample Monthly Rate Estimates

The table below shows estimated monthly premiums for non-tobacco applicants based on United of Omaha's published rate benchmarks (simplified issue, level benefit). These are illustrative figures — actual rates vary by carrier and individual health profile.

| Age | Female $5K | Female $10K | Female $25K | Male $5K | Male $10K | Male $25K |

|---|---|---|---|---|---|---|

| 50 | ~$13 | ~$23 | ~$53 | ~$15 | ~$27 | ~$64 |

| 60 | ~$17 | ~$31 | ~$72 | ~$22 | ~$40 | ~$96 |

| 70 | ~$26 | ~$50 | ~$120 | ~$36 | ~$69 | ~$168 |

| 80 | ~$48 | ~$92 | ~$226 | ~$64 | ~$124 | ~$306 |

Source: United of Omaha Living Promise rate guide (benchmark figures). Individual quotes may differ.

Age 65 Benchmark

For a 65-year-old non-tobacco female, $10,000 in simplified issue coverage runs approximately $41–$50/month depending on the carrier. Males at the same age typically land in the $54–$66/month range, per MoneyGeek's 2026 final expense cost analysis.

Guaranteed issue policies at the same age and coverage amount cost more — sometimes $90–$100/month or higher — because the carrier takes on unknown health risk without seeing your medical history. Comparing quotes across multiple carriers is the clearest path to finding a rate that fits your budget.

What Do Funerals Cost in Minnesota?

Understanding actual funeral costs helps you decide how much coverage to buy. The NFDA reports a 2023 national median of $8,300 for a traditional burial with viewing, and $6,280 for a funeral with cremation. Minnesota costs track closely with national figures.

Minnesota Funeral Cost Ranges

| Service Type | Estimated Cost |

|---|---|

| Traditional burial with service | ~$7,200–$8,755 |

| Direct burial (no service) | ~$4,400–$5,900 |

| Cremation with service | ~$6,700+ |

| Direct cremation | ~$2,955 |

Figures based on NFDA national benchmarks and Minnesota provider pricing (Roberts Family Funerals GPL, effective January 2025). Costs vary by provider and location.

Funeral costs have risen consistently. BLS data shows funeral expenses have climbed at roughly 3–4% annually in recent years, consistently outpacing general inflation. A policy purchased today needs to cover higher costs 10 to 20 years from now. Buy slightly more coverage than current figures suggest — the gap compounds faster than most people expect.

That flexibility in coverage amount matters for another reason too: burial insurance pays out as cash, so it covers more than just the funeral. Outstanding medical bills, hospice costs, small debts, and probate fees can all be covered — something pre-paid funeral plans can't do, since they lock every dollar to pre-selected services at a single funeral home.

Minnesota Burial Insurance Laws and Consumer Rights

Minnesota law gives burial insurance buyers specific rights worth understanding before you sign anything.

10-Day Free Look Period

Under Minnesota Statute 72A.52, you have a minimum of 10 days after receiving a new policy to review it and cancel for a full premium refund. If you're replacing an existing policy, that window extends to 30 days. If the required cancellation notice is missing from the policy documents, you can cancel within one year of purchase.

Freedom of Choice in Funeral Arrangements

Minnesota Statute 72A.325 prohibits insurers, agents, and other insurance professionals from steering families toward a specific funeral home or cemetery. Your burial insurance benefit goes to your named beneficiary, who can use it at any funeral provider they choose.

In practice, this means:

- No insurer can tie your policy to a particular funeral home

- Your beneficiary keeps full control over where and how funds are spent

FTC Funeral Rule

The federal FTC Funeral Rule applies to all covered funeral providers in Minnesota. Key protections include:

- Funeral homes must provide an itemized General Price List to anyone who asks — in person or by phone

- Consumers cannot be forced into package deals; you pay only for what you want

- Funeral homes cannot refuse to handle a casket or urn purchased elsewhere, and cannot charge a handling surcharge for outside items

Ask for that itemized price list upfront — it's your right, and it makes comparison shopping straightforward.

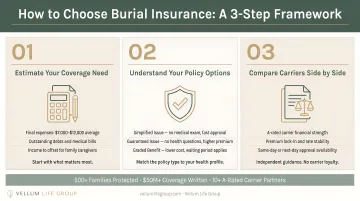

How to Choose the Right Burial Insurance Policy in Minnesota

A Simple Decision Framework

- Estimate your coverage need — Start with Minnesota funeral costs ($7,000–$9,000 for a traditional burial), then add any outstanding debts or medical bills you want covered

- Assess your health — If you can answer health questions favorably, start with simplified issue; if you have serious pre-existing conditions, go straight to guaranteed issue

- Compare across carriers — Rates vary significantly between insurers for the same age, gender, and coverage amount; shopping multiple carriers consistently turns up better pricing and terms

A Word on Direct-to-Consumer Policies

Products sold directly through a single carrier — such as Colonial Penn's guaranteed acceptance whole life — can be significantly more expensive. Forbes reported Colonial Penn's average cost for a $10,000 guaranteed acceptance policy at age 60 at $95/month. An independent broker shopping across 15+ carriers can often find comparable or better coverage for less.

Not all direct-to-consumer products are poor value, but the only way to know is to compare. That's exactly where an independent advisor earns their place.

Working with an Independent Advisor

Eva Ikonomakos at Vellum Life Group is a licensed advisor serving Minnesota residents, with access to 15+ A-rated carriers including Mutual of Omaha, Transamerica, American Amicable, and Americo. Working with an independent advisor means:

- Comparing rates across multiple carriers in a single conversation

- Matching your health history to the most favorable underwriting criteria

- Getting same-day or next-day approval on many policies

- Ongoing support: annual policy reviews and claims assistance for beneficiaries

The process is transparent and free, with no pressure and no obligation.

To get started with a free consultation: 917-363-3554 or info@vellumlifegroup.com

Frequently Asked Questions

How much is a $10,000 burial policy?

For a healthy 65-year-old non-tobacco female, a $10,000 simplified issue policy runs approximately $41–$50/month. Men the same age typically pay $54–$66/month. Rates drop at younger ages and rise for guaranteed issue policies, so comparing carriers is worth doing before you commit.

How does burial insurance work in Minnesota?

Burial insurance is a whole life policy that pays a tax-free cash benefit to your named beneficiary when you pass away. Premiums are fixed for life, coverage never expires, and the beneficiary can use the money for any purpose — funeral costs, medical bills, or other expenses — with no medical exam required to apply.

Is there a waiting period for burial insurance in Minnesota?

Simplified issue policies generally have no waiting period if you pass the health questions. Guaranteed issue policies always include a 2-year waiting period — natural-cause deaths during that window result in a refund of premiums plus interest rather than the full death benefit. Accidental deaths are typically covered in full from day one.

What is the difference between burial insurance and pre-need funeral insurance?

Burial insurance pays a flexible cash benefit to your named beneficiary, who can use it for any expense. Pre-need funeral insurance is purchased through a funeral home and the payout goes directly to that funeral home for pre-selected services.

Can I get burial insurance in Minnesota if I have health problems?

Yes. Guaranteed issue burial insurance accepts all eligible applicants regardless of health status — no health questions, no possibility of denial. Some conditions may also qualify under simplified issue policies depending on the carrier. An independent broker can match your health history to the most favorable underwriting criteria.

How much does a funeral cost in Minnesota?

A traditional burial service in Minnesota typically costs $7,200–$8,755 or more, while direct cremation averages around $2,955. Cremation with a full service runs closer to $6,700. These figures help determine how much burial insurance coverage makes sense for your situation.