The legal ownership structure of a life insurance company — mutual vs. stock — shapes how the insurer prices policies, manages reserves, handles claims, and uses profits. These aren't abstract governance details. For a permanent life insurance policy that must hold its value for 20 or 30 years, ownership structure is one of the more consequential factors most buyers never think to ask about.

This article breaks down the practical, policyholder-level benefits of mutual life insurance companies — what they are, how they work in practice, and when they matter most.

Key Takeaways

- Policyholders own mutual life insurance companies — not outside shareholders

- Without public markets to answer to, mutual insurers focus on long-term financial strength over quarterly earnings

- Strong performance can return to policyholders as dividends or premium credits, not investor payouts

- Over 60% of U.S. mutual insurers have operated for more than 100 years, with a median age of 120 years

- For permanent life insurance, this ownership structure matters most — the relationship spans decades

What Is a Mutual Life Insurance Company?

A mutual life insurance company is a private insurer owned by its policyholders. It does not issue stock to outside investors. When you hold a policy with a mutual insurer, you're also considered a member of the company — with certain governance rights — rather than simply a customer of it.

According to the ACLI Life Insurers Fact Book 2025, 106 mutual life insurers operated in the U.S. in 2024, compared to 530 stock life insurers. Mutual companies held approximately $8.48 trillion in life insurance in force — roughly 40% of the U.S. total.

Mutual insurers have historically concentrated in life insurance, where the long-term nature of policies makes the alignment between owners and policyholders particularly well-suited.

Without shareholders to answer to, a mutual company is structured to optimize for one thing: serving policyholders over the long term, rather than maximizing investor returns.

Key Benefits of Mutual Life Insurance Companies

The benefits below aren't theoretical. They're rooted in how the mutual ownership model shapes real operational decisions: pricing, reserves, investment strategy, and how profits are used.

Benefit 1: Decisions Favor Policyholders, Not Shareholders

In a stock insurer, management must serve two sets of interests that often pull in opposite directions. Shareholders want profit maximization; policyholders want fair premiums and reliable claims payments. In a mutual insurer, those interests are unified — because policyholders are the owners.

This plays out in practice in several ways:

- Pricing strategy: Mutual insurers can set premiums aimed at accurately reflecting long-term risk rather than inflating margins to hit quarterly earnings targets

- Claims reserves: Without shareholder pressure, management has less incentive to slash reserves or underinvest in claims-handling to boost short-term profitability

- Customer service: Decisions about staffing, service quality, and claims processes aren't weighed against dividend obligations to outside investors

The alignment isn't incidental — it's structural. The Armstrong Investigation of 1905, described by EBSCO Research Starters as a New York State inquiry into insurance industry misconduct, arose directly from public outrage at practices that prioritized insurer profitability over policyholder interests. The mutual structure inherently discourages many of those same conflicts.

The stakes are highest for long-duration policies — whole life, universal life, or any permanent coverage where the relationship spans decades and small incentive misalignments compound into large ones.

Benefit 2: Long-Term Financial Stability Over Short-Term Pressure

Mutual life insurance companies are not publicly traded. That single fact removes one of the most powerful forces pushing corporate management toward short-term thinking: quarterly earnings reports and the market reactions that follow them.

Without that pressure, mutual insurer management can:

- Build and maintain larger surplus reserves

- Adopt conservative investment strategies that prioritize stability over yield

- Absorb market volatility or unexpectedly high claims periods without the reactive cost-cutting a stock insurer might pursue to protect share price

The longevity data tells its own story. According to NAMIC, more than 60% of currently operating U.S. mutual insurance companies are over 100 years old, with a median age of 120 years. Few industries can point to that kind of structural durability.

Major mutual insurers also tend to carry the highest possible financial strength ratings. Northwestern Mutual holds A++, AAA, Aa1, and AA+ from AM Best, Fitch, Moody's, and S&P — the highest available designations from all four major agencies, for 35 consecutive years. New York Life enters 2026 with the same distinction.

For families purchasing permanent life insurance to fund estate planning, income replacement, or generational wealth transfer, an insurer's financial stability isn't a background consideration — it's the whole point.

Benefit 3: Profits Stay in the Policyholder Ecosystem

When a mutual life insurer collects more in premiums than it pays out in claims and expenses, those surplus funds belong to the policyholders — not outside investors.

The board may distribute that surplus as policyholder dividends, apply it as premium credits, or reinvest it in reserves that strengthen each policy's long-term value.

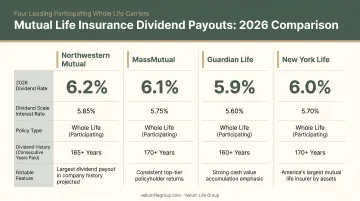

Policyholder dividends are not guaranteed. They depend on financial results and board decisions. But the track records of well-established mutual insurers are hard to ignore:

| Mutual Insurer | 2026 Dividend Payout | Consecutive Years |

|---|---|---|

| Northwestern Mutual | $9.2 billion | 155 years |

| MassMutual | $2.9 billion | 158 years |

| New York Life | $2.78 billion | 172 years |

| Guardian Life | $1.7 billion | 158+ years |

When dividends are issued, they can meaningfully reduce the net cost of a whole life policy over time or compound within the policy's cash value — a benefit that flows entirely to the policyholder. In a stock insurer, that same surplus flows to investors who may never hold a policy.

For whole life policyholders using coverage as a financial planning tool, this is where the mutual structure pays off most directly — through cash value that grows on their behalf, not a shareholder's.

What Happens When You Overlook Company Structure

Choosing life insurance based only on premium price, without considering ownership structure, can create subtle but compounding disadvantages over time.

A stock insurer under shareholder pressure may:

- Cut costs in ways that eventually affect claims service quality

- Raise rates more aggressively when profitable competitors enter the market

- Reduce policy features or benefits to improve profitability metrics

Demutualization — the process by which a mutual insurer converts to stock ownership — illustrates the risk. When MetLife demutualized in 2000 and Prudential in 2001, policyholders received one-time stock grants or cash payments.

What they gave up was ownership in a company structurally obligated to serve their long-term interests. The American Academy of Actuaries notes that the process distributes policyholder equity — but once complete, the company's orientation shifts toward investor returns.

That said, stock insurers aren't universally inferior. Many are financially strong, well-managed, and serve policyholders well. But ownership structure creates a different set of structural incentives — and for permanent life insurance, where the relationship must hold for decades, those incentives shape every decision the company makes on your behalf.

How to Get the Most Value from a Mutual Life Insurance Policy

Mutual life insurance companies deliver their strongest advantages through permanent products — whole life and universal life — where the combination of policyholder ownership, dividend participation, and cash value accumulation compounds over decades. Term life from a mutual insurer still carries the structural benefit of policyholder alignment, but the financial upside from dividends and cash value is most pronounced in permanent coverage.

Getting the most from the mutual model also means selecting the right company. Look for:

- Ratings of A or better from AM Best, Moody's, or S&P — a baseline indicator of claims-paying stability

- Decades of operating history, which reflects the structural discipline that defines well-run mutuals

- An uninterrupted dividend payment record spanning 20+ years, showing the insurer prioritizes long-term policyholder value

Working with an independent advisor — rather than a captive agent tied to a single carrier — lets you compare both mutual and stock insurers side by side. Eva Ikonomakos at Vellum Life Group works with 10+ A-rated carriers, including Mutual of Omaha, Foresters Financial, Royal Neighbors of America, and Kansas City Life, and can walk families and individuals through exactly this kind of structural comparison during a free, no-obligation consultation.

Conclusion

The core advantage of mutual life insurance companies is straightforward: when policyholders are also owners, the company's decisions — on pricing, claims, reserves, and profits — are structurally oriented toward serving those policyholders rather than external investors.

These structural benefits compound over time. Long-term financial stability, dividend eligibility, and freedom from shareholder pressure matter most in permanent life insurance — policies that must hold their value for decades. Comparing premiums is a starting point, but understanding whose interests the company is built to serve is what separates a good decision from the right one.

For families and individuals prioritizing long-term security over short-term pricing, the mutual structure is worth factoring into the decision. An independent advisor can help you compare mutual and stock carriers side by side — so you choose coverage built around your needs, not a company's quarterly targets.

Frequently Asked Questions

What are the benefits of mutual life insurance companies?

Mutual life insurance companies are owned by policyholders rather than outside shareholders, which means profits may return to policyholders as dividends or premium credits. The company's long-term decisions on pricing, claims, and reserves are built around policyholder interests, not investor returns.

How is a mutual life insurance company different from a stock life insurance company?

Stock insurers are publicly traded or investor-owned and optimize for shareholder returns. Mutual insurers are owned by policyholders and can prioritize long-term financial strength and policyholder value. The difference affects pricing strategy, how profits are used, and how the company responds to financial pressure.

Are dividends from mutual life insurance companies guaranteed?

Policyholder dividends are not guaranteed — they depend on the company's financial performance and board decisions. However, many established mutual insurers have paid dividends without interruption for over 150 years. When issued, dividends can reduce the net cost of a whole life policy or compound within its cash value.

Are premiums lower with mutual life insurance companies?

Mutual insurers are not automatically cheaper than stock insurers — premiums depend on age, health, coverage type, and the insurer's cost structure. That said, mutual insurers tend to price for long-term risk accuracy rather than maximum profit, and dividends can effectively reduce net coverage costs over time.

What is demutualization and how does it affect policyholders?

Demutualization is when a mutual insurer converts to stock ownership. Existing policyholders typically receive a one-time stock grant or cash payment, but the company's focus may shift toward shareholder returns — affecting future pricing, dividends, and policyholder service.

How do I know if a life insurance company is a mutual company?

Many mutual life insurers include the word "mutual" in their name, but the most reliable confirmation is the company's annual report or corporate structure filing. An independent insurance advisor can also verify ownership structure and explain what it means for your specific policy.