Introduction

You're building a life together — a mortgage, maybe kids, shared finances — and at some point the question surfaces: do we both need life insurance? The answer is almost always yes. But the follow-up question trips couples up: should you get one policy together or two separate ones?

Joint term life insurance is one answer — but it's not as straightforward as it sounds. It's less widely available than most couples expect, and the tradeoffs are real enough to shift the decision entirely depending on your situation.

This guide covers everything couples need to know about joint term life insurance: what it actually is, how first-to-die and second-to-die structures work, how it stacks up against two separate policies, and what to weigh before committing to either path.

Key Takeaways

- Joint term life insurance covers two people under one policy, paying a single death benefit (not one per person)

- First-to-die policies suit income replacement; second-to-die policies are built for estate planning

- Joint term can cost less than two separate policies, but delivers less total coverage

- After a first-to-die payout, the surviving partner is left without any coverage

- Joint term life is hard to find — working with a multi-carrier broker matters here

- Many couples end up better served by two individual policies for flexibility and independent protection

What Is Joint Term Life Insurance?

Joint term life insurance is a single policy that covers two people — typically spouses or domestic partners — for a defined period, commonly 10, 20, or 30 years. When a qualifying death occurs, the policy pays one death benefit to the designated beneficiary, then the policy ends. One payout — not two.

This structure distinguishes joint term from two individual term policies, where each person has their own independent coverage. It also distinguishes it from permanent joint life insurance (whole life or universal life), which lasts a lifetime and builds cash value. Joint term is specifically about affordable, temporary coverage. According to Guardian, few carriers actually offer it.

Who Can Apply?

Eligibility isn't limited to married couples. Most carriers that offer joint policies will consider:

- Married couples

- Domestic partners — typically accepted with documentation

- Engaged couples — some carriers extend eligibility here

- Unmarried couples with shared finances — qualifying requires demonstrating insurable interest, such as a shared mortgage, joint debt, or financial dependency

The NAIC confirms that life insurance can be taken out by anyone able to prove an insurable interest — marital status alone isn't the deciding factor.

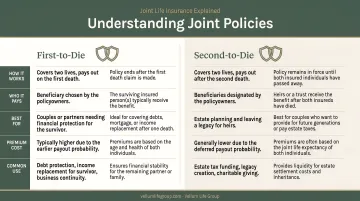

How Joint Term Life Insurance Works: First-to-Die vs. Second-to-Die

The structure of a joint term policy comes down to one question: when does the benefit pay out? There are two types, and they serve completely different purposes.

First-to-Die Joint Term Life Insurance

The death benefit is paid when the first insured person dies. The surviving partner receives the payout — then the policy ends. They are left without life insurance coverage and must reapply for a new individual policy at their current age and health status, which typically means higher premiums.

This structure is designed for income replacement. It makes the most sense for:

- Younger couples with shared income and a mortgage

- Families with young children who depend on both earners

- Couples who want coverage specifically tied to a defined financial obligation (for example, 20 years until the mortgage is paid off)

The key limitation is straightforward: the survivor is uninsured from the moment the benefit is paid. That's the central tradeoff to weigh before choosing this structure.

Second-to-Die Joint Term Life Insurance

Second-to-die (also called survivorship) policies pay only after both insured partners have died. The surviving spouse receives no benefit during their lifetime — the payout goes to heirs or beneficiaries after the second death.

This structure is unsuited for income replacement. It's used for:

- Leaving assets to children or other heirs

- Covering estate taxes after both parents are gone

- Funding special-needs trusts or legacy planning goals

Second-to-die term policies are extremely rare. Policygenius notes that most second-to-die policies are permanent rather than term. If survivorship coverage is your goal, a permanent joint policy is almost certainly the more practical option.

Quick comparison:

| Feature | First-to-Die | Second-to-Die |

|---|---|---|

| Pays when | First insured dies | Both insured die |

| Designed for | Income replacement, mortgage protection | Estate planning, heirs |

| Survivor benefit | Yes — survivor receives payout | No — survivor must continue paying premiums |

| Term version available? | Rare but exists | Very rare; usually permanent |

Joint Term Life Insurance vs. Separate Policies

Both paths provide real coverage — but they work differently enough that choosing between them can affect your family's protection for decades.

Cost Comparison

Joint term life can be less expensive in total premium. The reason is straightforward: with a joint first-to-die policy, the insurer faces a maximum payout of, say, $500,000. With two separate $500,000 policies, the insurer is on the hook for up to $1,000,000 if both partners die during the term. One exposure is smaller, so the premium reflects that.

The cost equation flips, however, when partners have different risk profiles. Separate policies become the better value when:

- One partner is significantly older than the other

- One partner smokes or has a pre-existing health condition

- Health differences are substantial enough that independent underwriting saves money on the lower-risk person

A healthy 30-year-old can typically get $500,000 in individual term coverage for under $30 per month. Joint term premiums vary by carrier and aren't published consistently, which is another reason to compare options directly.

Coverage Flexibility

Two separate policies give each partner complete independence:

- Different coverage amounts based on each person's income and obligations

- Different term lengths (one partner may need 20 years; the other, 30)

- Different riders tailored to individual needs

- No complications if the relationship changes

Joint policies link two people's coverage together — which creates real problems if circumstances shift. Divorce is the obvious example: Policygenius notes that some insurers offer a rider to split a joint policy upon divorce, but not all do, and a shared policy adds complexity to an already difficult process.

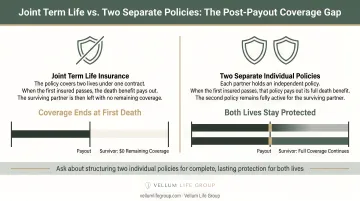

What Happens When the Policy Pays Out?

This is where the practical difference becomes most visible:

- First-to-die joint policy: The survivor gets the death benefit — and immediately loses all life insurance coverage. Replacing it at an older age, or with changed health, can cost significantly more.

- Two separate policies: The surviving partner keeps their own policy completely intact. No gap. No reapplication. No coverage interruption.

When couples compare only monthly premiums, they're missing the bigger number: what a surviving partner pays to get re-covered at 50 or 60, possibly after a health change, versus what they'd pay to simply keep a policy they already own.

Pros and Cons of Joint Term Life Insurance

Advantages

- Costs less upfront: One policy, one premium — typically cheaper than two individual policies covering the same total death benefit, which helps couples managing tight budgets

- One application, one insurer, one monthly payment — no juggling two separate policies

- Can open doors for a harder-to-insure partner: In some cases, a joint policy lets a partner with a health condition obtain coverage under the healthier applicant's underwriting profile — though this is carrier-dependent and not guaranteed

Disadvantages

- Harder to find: Joint term life is a genuine market gap — not every insurer offers it, which makes comparing options through a broker with access to multiple carriers especially important

- Pays out once, not twice: Two individual $500,000 policies create $1,000,000 in total potential coverage. A joint policy at the same premium typically pays only once

- Leaves the survivor uninsured: Once the first-to-die benefit pays out, the surviving partner has no coverage — and replacement policies at an older age or with worse health cost substantially more

- Vulnerable to life changes: Divorce, separation, or a shift in one partner's health creates complications that simply don't arise with two separate individual policies

Who Should Consider Joint Term Life Insurance?

Joint term isn't the right fit for every couple, but it works well in specific situations:

- Young dual-income couples with similar earnings and shared obligations — a mortgage, young children — who want simple, affordable income-replacement coverage without complex planning needs

- Couples where one partner has difficulty qualifying individually due to a pre-existing health condition, where a joint policy may offer one path to coverage (availability and underwriting terms vary by carrier)

- Couples in a defined financial window — for example, those who want coverage specifically while paying off a 20-year mortgage and plan to reassess once that obligation ends

Availability genuinely constrains this decision. Not every carrier offers joint term, so comparing your real options means working with an independent advisor who has access to multiple carriers — not just one.

How to Get Joint Term Life Insurance

Because joint term life isn't universally available, the first practical step is working with an independent broker who has relationships with multiple carriers. Going directly to a single insurer often means hearing "we don't offer that" without knowing what alternatives exist.

Vellum Life Group works with 15+ A-rated carrier partners and shops across that network to identify which carriers currently offer joint term options — and what pricing looks like for your specific situation. That kind of cross-carrier comparison is difficult to get by contacting insurers one at a time.

Once you've identified a carrier that fits, the application moves quickly. Here's what to expect:

The Application Process

Both partners complete the application together. Expect:

- Health questionnaires for both individuals

- Possible medical exams depending on coverage amount and carrier requirements

- Blended underwriting — both partners' age, health history, and lifestyle factors (including smoking) affect the final premium

Decisions to Make Before You Apply

- Choose a term length (10, 20, or 30 years) that covers your longest financial obligation — typically a mortgage or until dependents are independent

- Size coverage around income replacement, mortgage balance, outstanding debts, and what your dependents would need

- Decide between first-to-die (income replacement focus) or second-to-die (estate planning focus) — these serve entirely different purposes

- Get quotes for both joint and separate policies before committing; the pricing gap is often smaller than expected

Coverage needs shift as life does. An annual review keeps your policy aligned with major changes — new dependents, a refinanced mortgage, a shift in one partner's health. Vellum Life Group includes ongoing reviews as part of client support, so you're not left managing that alone.

Frequently Asked Questions

Can you do joint term life insurance?

Yes, joint term life insurance does exist. It's less commonly offered than permanent joint policies, though, and availability varies by carrier. Because it's a niche product, comparing options through a broker with multiple carrier relationships is the most reliable way to find what's actually available.

How much does a $1,000,000 term life insurance policy cost?

For a healthy nonsmoking individual around age 40, MoneyGeek data shows averages around $86/month for women and $109/month for men on a 20-year term. Costs vary by age, health, gender, and whether you're applying individually or jointly — getting a personalized quote gives a far more accurate figure.

Is joint term life insurance cheaper than two separate policies?

Often yes on total premium, but the tradeoff is one death benefit instead of two. Two individual $500,000 policies can pay out $1,000,000 in total; a joint policy pays only $500,000. If your household needs $1,000,000 in total protection, the "cheaper" joint policy may actually leave you underinsured.

Can unmarried couples get joint term life insurance?

Yes, in most cases. Domestic partners, engaged couples, and unmarried partners who can demonstrate insurable interest — such as a shared mortgage, joint financial obligations, or financial dependency — typically qualify. Documentation of the relationship or shared finances is usually required.

What happens to a joint term life policy if we divorce?

Divorce complicates joint policies significantly. Some insurers offer a rider that splits the policy upon divorce, but not all do, and one or both partners may end up without coverage during the transition.

Should couples get joint or separate life insurance policies?

Separate policies offer more flexibility, independent coverage amounts, and no complications if circumstances change. Joint term life can make sense for couples with nearly identical coverage needs and simple financial goals. For most couples, though, the long-term flexibility of two individual policies outweighs the upfront premium savings.