The catch: the tax rules governing these transfers are unforgiving. One mistimed move — dying within three years of the transfer — can undo the entire estate planning benefit. The paperwork must be airtight, and the ongoing behavior after the transfer matters just as much as the transfer itself.

This guide covers the IRS rules you need to understand first, the exact steps to complete the transfer, how to choose between a direct transfer and an Irrevocable Life Insurance Trust (ILIT), and the most common mistakes families make.

Key Takeaways

- Transferring ownership removes the policy from your taxable estate — but only if you survive at least three years after the transfer date

- Once transferred, you permanently lose all control: no changing beneficiaries, no borrowing against the policy, no canceling coverage

- The transfer may trigger gift tax reporting if the policy's cash value exceeds the $19,000 annual gift exclusion (2025)

- Your child assumes full responsibility for premium payments after the transfer

- Two paths exist: a direct transfer to your child, or a transfer into an ILIT, each suited to different estate planning goals

IRS Rules and Tax Implications You Must Know Before Transferring

Three IRS rules can quietly undo the estate planning benefit you're trying to create. Understanding them before you transfer is the difference between a successful transfer and one that lands right back in your taxable estate.

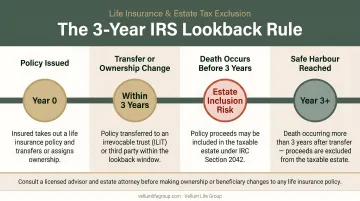

The Three-Year Rule

Under IRC Section 2035, if you transfer a life insurance policy and die within three years of the transfer date, the IRS pulls the full death benefit back into your taxable estate. The tax benefit you planned for disappears entirely.

For 2025, the federal estate tax exemption sits at $13.99 million per individual (per IRS Rev. Proc. 2024-40). That means federal estate tax exposure only affects a small fraction of estates — roughly 0.07% of decedents, according to Congressional Research Service data. But for parents with large policies, significant assets, or state-level estate tax exposure, the three-year rule is a real risk — especially for those in declining health or approaching later retirement.

The practical takeaway: transfer early, not late.

Surviving the three-year window is necessary — but it's not sufficient on its own. Even a completed transfer can be pulled back into your estate if you retain certain control rights over the policy.

Incidents of Ownership

Treasury Regulation 20.2042-1 defines "incidents of ownership" broadly. They're not just formal ownership — they include any economic control rights you retain over the policy after the transfer.

Retaining any of these rights keeps the policy in your estate:

- Changing the beneficiary

- Surrendering or canceling the policy

- Assigning the policy or revoking an assignment

- Pledging the policy as loan collateral

- Borrowing against the cash surrender value

Retaining even one of these rights gives the IRS grounds to include the policy in your estate. The transfer must be complete and unconditional.

Gift Tax Considerations

Transferring a policy is treated as a taxable gift if the policy's fair market value exceeds the $19,000 annual gift exclusion per donee for 2025.

A few important distinctions:

- Term policies typically carry minimal or no cash value, so gift tax exposure is low

- Permanent policies (whole life, universal life) with significant cash value require a formal valuation — under Treasury Regulation 25.2512-6, the IRS uses interpolated terminal reserve plus unearned premium, not simply cash surrender value. Request a carrier valuation before filing.

- Gift tax does not automatically mean tax is owed — amounts above the annual exclusion can be applied against the lifetime unified exemption ($13.99 million in 2025), but you must file IRS Form 709 to report the gift

Once you understand these three rules, the actual transfer process becomes much more straightforward — as long as you follow the steps in the right order.

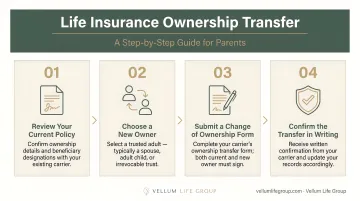

How to Transfer Life Insurance Policy Ownership to Your Child

The transfer process must satisfy both your insurer's administrative requirements and the IRS's ownership rules. Working with a licensed insurance advisor like Vellum Life Group at this stage ensures paperwork is completed correctly and no ownership rights are inadvertently retained.

Step 1: Confirm Your Policy Is Eligible for Transfer

- Individual policies can be transferred; group or group-sponsored policies generally cannot

- Check your policy documents or call your insurer to confirm no endorsements or provisions restrict ownership transfer

- Identify whether the policy is term or permanent — this affects your gift tax obligations

Step 2: Decide Whether Your Child Is Ready to Assume Ownership

Two requirements must be met before proceeding:

- Age: Your child must be a legal adult (18 or older in most states). Minors cannot legally own a life insurance policy and cannot enter into contracts. The transfer must wait until adulthood, or a trust or custodial arrangement must be used instead.

- Financial readiness: Your child must understand and accept ongoing premium payment responsibility. If you continue paying premiums after the transfer, the IRS may treat that as evidence of retained ownership and pull the policy back into your estate.

Step 3: Request and Complete the Transfer Paperwork

Contact your insurer directly and request their ownership transfer or absolute assignment form. This is the legal document that moves all policy rights from you to your child.

Key points about the paperwork:

- The form must be completed by both you (current owner) and your child (new owner)

- If the insured is a different person than the owner, they may also need to sign

- Forms are insurer-specific — there is no universal industry form; Prudential's, Mutual of Omaha's, and Transamerica's forms, for example, each have their own requirements

- The insurer records the new owner internally once the form is processed

Step 4: Confirm the Transfer and Update Related Records

Once the insurer processes the assignment:

- Obtain written confirmation showing your child's name as the new owner — this documentation is critical for tax and estate records

- Review beneficiary designations — original beneficiaries may remain on file unless the new owner (your child) takes action to update them

- Keep a copy of the completed assignment form and the insurer's confirmation letter in a secure location

Direct Transfer vs. Irrevocable Life Insurance Trust (ILIT): Which Is Right for You?

Parents have two paths: transferring the policy directly to an adult child, or first establishing an ILIT and transferring the policy into it. Your estate size and how much ongoing control you want over the death benefit will largely determine which approach fits.

Direct Transfer to Your Child

Best fit when:

- Your child is financially stable and capable of managing long-term premium payments

- You want a simple process with no legal setup or ongoing trust administration

- Your estate is below the federal exemption threshold and you're primarily focused on avoiding probate or simplifying your legacy

The trade-off: Once completed, the transfer is permanent. If your relationship changes, your child faces financial hardship, or you have second thoughts, you cannot reclaim ownership or direct who receives the death benefit.

Irrevocable Life Insurance Trust (ILIT)

An ILIT holds the policy in trust rather than in your child's hands directly. The death benefit stays outside your estate and, depending on how the trust is drafted, outside your child's estate too. You can also set terms governing how and when proceeds are distributed.

Best fit when:

- Your estate is large enough that both your estate and your child's estate face tax exposure

- You want structural control over how the death benefit is used (for example, staggered distributions or restrictions)

- You're comfortable with higher upfront complexity in exchange for long-term flexibility

The trade-off: An ILIT requires an estate planning attorney to draft, adds cost and administrative requirements, and is itself irrevocable — it cannot be changed once established. Premium gifts to the trust commonly use Crummey withdrawal powers (per Crummey v. Commissioner, 397 F.2d 82) to qualify for the annual gift exclusion, requiring the trustee to send documented notices to beneficiaries.

The table below summarizes how the two approaches compare across the factors that matter most to most families:

| Feature | Direct Transfer | ILIT |

|---|---|---|

| Setup complexity | Low | High (attorney required) |

| Cost | Minimal | Higher (legal/admin fees) |

| Proceeds in child's estate | Potentially yes | Can be excluded if properly structured |

| Control over distributions | None after transfer | Governed by trust terms |

| Irrevocability | Yes | Yes |

| Three-year rule applies | Yes | Yes (for existing policy transfers) |

Common Mistakes When Transferring a Life Insurance Policy to Your Child

Even a well-intentioned transfer can unravel if the details aren't handled correctly. These are the four mistakes that most often derail the process:

Waiting too long. Parents approaching retirement or in declining health risk dying within the three-year lookback window, which wipes out the estate tax benefit entirely. This transfer should happen well in advance.

Continuing to pay premiums. After the transfer, your child must pay the insurer directly. If you want to help financially, gift the funds to your child first — letting premium payments flow through you creates documentation risk the IRS will scrutinize.

Transferring to a minor. Minors cannot legally own a life insurance policy in most states. New York sets a minimum age threshold of 14 years and 6 months, and the NAIC notes most insurers won't pay proceeds directly to minors at all. Without a trust or custodial structure in place, the transfer can be delayed or invalidated.

Skipping guidance on permanent policies. Term transfers are straightforward — minimal cash value, limited gift tax exposure. Permanent policies are a different matter. Significant cash value triggers formal valuation requirements, Form 709 filing, and a more complex IRS review. Errors in valuation or paperwork often require costly legal corrections to fix.

Conclusion

A life insurance policy ownership transfer can be a genuine legacy planning tool — removing a meaningful asset from your taxable estate, locking in coverage for your child at existing terms, and passing the policy's benefits to them intact. But execution matters more than intention here.

Getting it right comes down to three factors:

- Timing — surviving the three-year lookback window after transfer

- Clean transfer — relinquishing all incidents of ownership completely

- Right structure — choosing between a direct transfer or an ILIT based on your estate goals

Before taking any action, speak with a licensed insurance and legacy planning advisor. Vellum Life Group offers free, no-pressure consultations to help families understand their options and structure transfers correctly — reach Eva Ikonomakos at 917-363-3554 or info@vellumlifegroup.com.

Frequently Asked Questions

Is transferring ownership of a life insurance policy to your child taxable?

The transfer may be subject to gift tax if the policy's fair market value exceeds the $19,000 annual gift exclusion (2025). Reporting on Form 709 doesn't always mean tax is owed — excess amounts can offset your lifetime exemption instead. Note that if the insured dies within three years of transfer, proceeds may be pulled back into the taxable estate.

What happens when you transfer ownership of a life insurance policy to your child?

Your child becomes the legal owner, gains the right to change beneficiaries or cancel the policy, and takes on premium payment responsibility. The death benefit is removed from your taxable estate, as long as you survive at least three years after the transfer (see the three-year rule below).

Can you transfer a life insurance policy to a minor child?

In most states, minors cannot legally own a life insurance policy. The policy must typically wait until the child turns 18, or parents can use a trust or custodial arrangement to hold it on the minor's behalf in the meantime.

Does the three-year rule always apply when transferring life insurance to my child?

Under IRC Section 2035, the rule applies to transfers made for estate tax purposes without full consideration. If the original owner survives three full years after the transfer date, the death benefit is fully excluded from their taxable estate.

Who pays the premiums after a life insurance policy is transferred to a child?

Your child takes over premium responsibility after the transfer. If the original owner continues paying, the IRS may treat it as evidence of retained ownership, potentially pulling the policy back into the taxable estate.

Can I take back ownership of a life insurance policy after transferring it to my child?

No. A completed absolute assignment is generally irrevocable — the original owner cannot reclaim the policy or any of its associated rights. That's why consulting an advisor before initiating the transfer is worth the time.