Introduction

Most families buy life insurance with one goal in mind: make sure the people they love are financially protected. What many don't realize is that without the right structure, a life insurance payout can be delayed by probate, reduced by estate taxes, or distributed in ways that don't reflect the policyholder's actual wishes.

According to LIMRA's 2025 Facts About Life Insurance, 51% of American adults have some form of life insurance. Yet a 2025 Caring.com survey found only 13% have a living trust. For the remaining 87%, that's a meaningful gap — one that can cost families both time and money at the worst possible moment.

This guide covers what a family trust life insurance arrangement actually is, the three concrete advantages it provides, and how to tell whether it makes sense for your situation.

TL;DR

- A family trust life insurance arrangement places a life insurance policy inside a legal trust, so the trust owns the policy and controls how proceeds reach beneficiaries.

- The three main advantages: shielding proceeds from estate taxes, bypassing probate for faster payouts, and giving you direct control over how beneficiaries receive the money.

- Most valuable for parents of minor children, blended families, cohabiting couples, and estates that approach state or federal tax thresholds.

- Permanent life insurance (whole or universal life) works better than term inside a trust, since a term policy can expire before it's ever needed.

- Setting up a trust requires an estate planning attorney. Finding the right policy to place inside it requires a licensed insurance advisor who can match coverage to your trust's structure.

What Is Family Trust Life Insurance?

In a family trust life insurance arrangement, a legal trust — rather than the individual — owns the life insurance policy. When the insured passes away, the death benefit bypasses the personal estate and goes directly to the trust, which then distributes funds to named beneficiaries according to the terms the grantor set in advance.

Revocable vs. Irrevocable Trusts

There are two main structures, and the distinction matters:

| Trust Type | Can Be Changed? | Removes Policy from Estate? | Best Used For |

|---|---|---|---|

| Revocable trust | Yes | No | Probate avoidance, minor children, flexibility |

| Irrevocable (ILIT) | No | Yes | Estate tax protection, legacy planning |

A revocable trust gives you flexibility — you can amend it, dissolve it, or change beneficiaries at any time. The tradeoff: because you retain control, the policy typically remains in your taxable estate.

An irrevocable life insurance trust (ILIT) cannot be changed once established. But that permanence is precisely what removes the policy from your taxable estate, which matters most for families with significant estate tax exposure.

Understanding which structure fits your situation is the first step — and it shapes every decision that follows, from how the policy is funded to how beneficiaries receive their distributions.

Key Advantages of Family Trust Life Insurance

Setting up a family trust for life insurance affects three things your family cares about most: how much they receive, how fast they receive it, and whether it's used the way you intended.

Advantage 1: Shielding Life Insurance Proceeds from Estate Taxes

Under IRC Section 2042, when an individual personally owns a life insurance policy, the death benefit is included in their taxable estate. A $1 million or $2 million payout intended for your family can become a direct tax liability instead.

The federal estate tax rate reaches 40% above the exemption threshold. For 2025, the federal basic exclusion amount is $13.99 million, rising to $15 million for 2026 per recent IRS updates. Most families won't hit that threshold federally.

But state-level estate taxes are a different story:

- Oregon: $1M threshold

- Massachusetts: $2M threshold

- Rhode Island: ~$1.8M threshold

- Minnesota / Washington: ~$3M threshold

- Illinois: $4M threshold

A $1 million life insurance policy, added to existing home equity, retirement accounts, and investments, can push a family over these state thresholds without any warning.

When an ILIT owns the policy for more than three years before the insured's death, the proceeds are generally excluded from the taxable estate entirely. The trust becomes the policy owner, so the death benefit flows directly to the trust and falls outside estate tax calculations. The difference can be tens of thousands of dollars reaching your heirs instead of the IRS.

This advantage is most relevant for:

- Families in states with low estate tax thresholds

- Estates where the life insurance benefit itself could trigger state-level tax

- Married couples using survivorship (second-to-die) policies

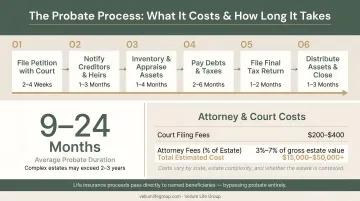

Advantage 2: Bypassing Probate for Faster, Private Payouts

Without a trust, life insurance proceeds paid to an individual's estate must pass through probate — the court-supervised process of validating a will and settling debts — before beneficiaries can access a dollar.

According to the American Bar Association, the average estate completes probate in 6 to 9 months, and contested cases can stretch to years. During that time, a surviving spouse or partner may have no access to funds intended for immediate expenses: mortgage payments, childcare, medical bills.

Probate also isn't free. Nolo reports attorney fees ranging from $150–$250+ per hour, with some states using percentage-based fee schedules. In California, for example, statutory attorney compensation runs 4% of the first $100,000 in estate value, then scales down from there — on a $500,000 estate, that adds up quickly.

Because the trust is a separate legal entity, the trustee can collect and distribute the death benefit directly once the insurance company receives the required documentation. That often happens within weeks of a death certificate being issued, not months into a court process.

There's also a privacy benefit. Probate proceedings are public record — anyone can see what assets were distributed and to whom. Trust distributions remain private.

This advantage matters most for:

- Unmarried or cohabiting couples (under intestacy rules, unmarried partners typically receive nothing from an estate they're not named in)

- Blended families where competing claims could slow or complicate probate

- Families with minor children who need immediate financial support

Advantage 3: Controlled, Protected Distribution to Beneficiaries

Naming a beneficiary directly on a life insurance policy is simple, but it gives you no control over how the money is used once it's paid out. A lump sum delivered to an 18-year-old, a beneficiary with financial challenges, or someone receiving government benefits can create outcomes you never intended.

A trust changes that entirely. The trust document can specify:

- Funds released in installments over time

- Distributions restricted to specific purposes (education, housing, medical care)

- Access only after beneficiaries reach a certain age

- A trustee you choose to manage and enforce these terms

Two situations where this matters most:

Minor children. Minors cannot legally receive life insurance proceeds directly. Without a trust, a court appoints a property guardian to manage the funds — someone you didn't choose, under terms you didn't set. A trust puts you in control.

Beneficiaries receiving government benefits. The SSA sets SSI resource limits at $2,000 for an individual and $3,000 for a couple. A direct lump-sum inheritance can disqualify a beneficiary from Medicaid or SSI. A properly structured special needs trust can preserve those benefits while still providing financial support.

This advantage is especially valuable for:

- Parents of young children

- Families with a special needs dependent

- Blended families where the grantor wants to differentiate between a surviving spouse and children from a prior relationship

- Anyone building multigenerational wealth with structured milestones

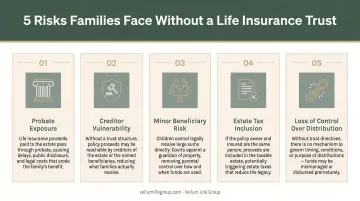

What Happens When Family Trust Life Insurance Is Ignored

Without a trust, the default outcome is rarely what families intended.

Life insurance proceeds paid to an estate enter probate. From there, they're subject to delays, legal costs, and distribution based on whatever the will says — or, for the 76% of Americans who don't have a will, by state intestacy rules that have nothing to do with the insured's actual wishes.

Specific risks families face without a trust structure:

- Estate tax exposure on a large death benefit, particularly in states with low thresholds like Oregon ($1M) or Massachusetts ($2M)

- Probate delays of 6 months to over a year, leaving the surviving family without access to funds

- Court-supervised guardianship for minor beneficiaries, introducing legal costs and removing parental control over how funds are managed

- Cohabiting partners left unprotected if not named as beneficiary — and even with a designation, having no recourse if the estate is contested

- Lump-sum payouts with no restrictions, potentially affecting a beneficiary's eligibility for government benefits or their long-term financial stability

Each of these risks is preventable. The gap isn't intent — it's information. Most families don't realize their life insurance payout can be delayed, reduced, or misrouted until the right structure is already in place.

How to Get the Most Value from Family Trust Life Insurance

Getting this arrangement right comes down to three decisions — and each one affects whether the trust actually delivers for your family.

1. The right trust structure

- Revocable trust: for probate avoidance, minor children, and flexibility

- ILIT: for estate tax protection and legacy planning (remember the 3-year rule — an ILIT must own the policy for more than 3 years before death for the proceeds to be excluded from the estate)

2. The right policy type Permanent life insurance — whole life or universal life — is generally preferred over term inside a trust. A term policy risks expiring before the insured passes away, leaving the trust unfunded. Whole life provides a guaranteed death benefit for life; universal life adds premium flexibility and adjustable benefit options.

3. A trustee who will follow your wishes The trustee manages the trust, ensures compliance with its terms, and distributes funds according to your instructions. Choose someone who understands both the responsibility and your family's situation.

The two-step professional process:

- An estate planning attorney drafts and establishes the trust

- A licensed insurance advisor identifies the right policy — coverage amount, policy type, and carrier — to fund it

These are distinct roles, and both matter. Advisors like those at Vellum Life Group work with 15+ A-rated carriers and specialize in legacy planning. As an independent broker — not a captive agent tied to one company — Vellum can search across carriers to find the permanent policy that fits your specific trust structure and goals.

Annual reviews matter too. A new child, a divorce, a significant increase in assets — any of these may require updates to the trust or the underlying policy. Vellum Life Group includes annual reviews as part of ongoing client support, so the arrangement stays aligned with your family's situation as it changes.

Conclusion

A family trust life insurance arrangement is one of the most effective tools available for making sure a life insurance policy delivers its full intended benefit — to the right people, at the right time, in the right way.

The advantages compound over time. The earlier the structure is in place, the more effectively it protects against estate tax exposure, probate friction, and uncontrolled distribution. Starting early also locks in coverage while the insured is still insurable — before health changes make qualifying harder or premiums climb.

Family trust life insurance is an ongoing part of a family's legacy plan — not a box to check once and forget. At minimum, review the arrangement annually to confirm the trust terms, beneficiary designations, and premium funding still reflect your current situation. An independent advisor can help you spot gaps before they become problems.

Frequently Asked Questions

What is the difference between a revocable and irrevocable life insurance trust?

A revocable trust can be changed or dissolved at any time, offering flexibility — but the policy typically remains in the taxable estate. An irrevocable trust (ILIT) cannot be changed once established, but removes the policy from the estate entirely, providing estate tax protection that a revocable trust cannot.

Can I get family trust life insurance if I have a medical condition or take medications?

A medical condition or medication use doesn't automatically disqualify someone from obtaining life insurance for a trust — outcomes depend on the specific condition, its severity, and the carrier. Working with an independent advisor who accesses multiple carriers increases the likelihood of finding competitive rates, since underwriting standards vary significantly across insurers. Vellum Life Group works with 15+ carriers to help clients in exactly this situation.

What type of life insurance policy is best to put in a trust?

Permanent life insurance — whole life or universal life — is generally preferred because it provides a guaranteed death benefit for the insured's lifetime. Term policies can be placed in a trust but carry the risk of expiring before the insured passes, which would leave the trust without proceeds.

Does putting life insurance in a trust mean my family avoids probate?

Yes. When a trust owns the life insurance policy and is named as beneficiary, the death benefit bypasses the probate process entirely. The trustee can distribute funds directly to beneficiaries based on the trust's terms, often within weeks of the death being documented.

Can I change the beneficiaries after putting life insurance in a trust?

It depends on the trust type. With a revocable trust, changes can be made at any time. With an irrevocable trust, beneficiaries and terms are fixed once established — making it worth thinking carefully before setup and consulting both an estate planning attorney and a licensed insurance advisor.

How much does it cost to set up a family trust life insurance arrangement?

Trust setup costs vary by complexity and location. Working with an estate planning attorney to draft the trust document typically starts at $1,200–$2,000 according to FindLaw, though more complex structures cost more. The life insurance policy is a separate, ongoing cost — but consultations with a licensed insurance advisor, including through Vellum Life Group, are typically free.