The reality: department-issued group coverage is often capped well below what a family actually needs, and it disappears the moment an officer retires or changes agencies. Individual life insurance, on the other hand, is more accessible — and more affordable — than most officers expect.

This guide covers how being an officer affects underwriting, what policy types make sense at different career stages, what coverage costs in 2026, and how to determine the right amount for your family's specific situation.

Key Takeaways

- Most municipal patrol officers qualify for individual life insurance at standard or preferred rates — the badge alone doesn't automatically raise your premiums

- Department and union coverage typically pays only 1–2x base salary and is not portable after retirement or a career change

- Hazardous specialties like SWAT, bomb disposal, or undercover narcotics may affect premiums, but rarely result in outright denial

- Term life is the most affordable starting point for income replacement and mortgage protection

- Locking in coverage while young and healthy protects both your rate and your future insurability

Why Department-Issued Life Insurance Often Falls Short

Group life insurance through a department or union is tied to your membership in that plan. When you retire, transfer agencies, or leave law enforcement, that coverage typically ends — and converting it to an individual policy comes with tight deadlines and restrictions.

Deadlines are tighter than most officers realize. New Jersey's public group life coverage, for example, ends just 31 days after coverage ends. Officers have a one-time conversion option within that window, but the converted policy cannot be term insurance.

FEGLI (the federal government's group plan) continues into retirement only if you retire on an immediate annuity with five years of prior continuous coverage.

The Benefit Amount Problem

Most public-sector group plans pay a fixed benefit or a salary multiple that leaves significant gaps. A few real examples:

- Chicago FOP (MetLife plan): $25,000 for less than one year of service; $75,000 for one year or more

- FEGLI Basic: Annual pay rounded up to the next $1,000, plus $2,000

- Newport News, VA (VRS): Two times annual salary

At a median officer salary of $77,270, a $75,000 fixed benefit covers less than one year of income — nowhere near what a family with a mortgage and young children would need.

What Happens Near Retirement

Group benefits often shrink precisely when you'd expect them to hold steady. Under FEGLI's standard election, coverage begins reducing by 2% per month at age 65 until only 25% of the original benefit remains. Option B and C coverage can reduce all the way to zero unless a no-reduction election is made at a notably higher premium cost.

An officer who spent 25 years on the force can lose the bulk of that group coverage right at the moment their family still carries a mortgage, college tuition, or other long-term financial obligations — which is exactly why independent coverage matters.

How Life Insurance Underwriting Works for Police Officers

Underwriters evaluate three main areas: your health and age, lifestyle factors, and your occupation. For most municipal patrol officers, the occupation piece is less of an issue than many assume.

According to Policygenius, municipal officers without hazardous specialties can often qualify for standard rate classifications — meaning their occupation alone doesn't add cost to their policy.

How Your Assignment Affects Your Rate

Not all law enforcement roles are treated equally:

- General patrol and desk duty: Typically eligible for standard rates alongside the general population

- SWAT, bomb disposal, undercover narcotics, Secret Service: Evaluated case by case, requiring detailed documentation of daily duties — not an automatic decline, but underwriters want specifics

- Border patrol, corrections, similar roles: May fall into individual consideration depending on the carrier

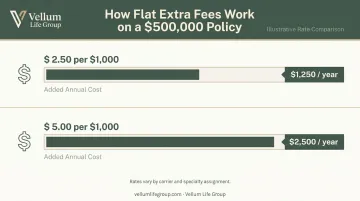

Understanding Flat Extra Fees

When a higher-risk specialty does affect underwriting, carriers often apply a flat extra fee — an additional charge per $1,000 of death benefit — rather than simply declining the application.

Public underwriting materials and industry sources cite flat extras typically ranging from $2.50 to $5 per $1,000 of coverage. On a $500,000 policy, that math looks like this:

| Flat Extra Rate | Annual Added Cost on $500,000 Policy |

|---|---|

| $2.50 per $1,000 | $1,250/year |

| $5.00 per $1,000 | $2,500/year |

Whether a flat extra applies — and at what rate — depends on the specific carrier and the specifics of your role.

Mental Health and PTSD

Occupation risk isn't the only factor underwriters weigh. Officers have roughly twice the prevalence of PTSD and depression compared to the general population, and carriers will review any treatment history or active diagnosis during underwriting.

That said, a diagnosis doesn't disqualify you. What matters is:

- Receiving treatment: Generally viewed more favorably than untreated conditions

- Timing and stability: How recently symptoms occurred and whether they're managed

- Full disclosure: Misrepresentation — even unintentional — can result in a denied claim when your family needs it most

Why an Independent Broker Matters Here

Different carriers treat the same occupation very differently. One insurer might apply a flat extra for undercover work; another might offer standard rates. An independent broker with access to multiple A-rated carriers can identify which insurer will view your specific assignment most favorably, rather than defaulting to a single carrier option.

Vellum Life Group works with 15+ A-rated carriers, comparing options across the market before recommending a policy. Annual reviews are built into the process, so coverage adjusts as your assignment or circumstances change.

Life Insurance Options for Police Officers

Term Life Insurance

Term life is the most commonly chosen option for officers with young families, mortgages, or income replacement needs. It provides a fixed death benefit for a set period — typically 10, 20, or 30 years — at a level premium that doesn't change.

It's well-suited for covering specific, time-bound obligations:

- Replacing income during the years dependents rely on you

- Covering an outstanding mortgage balance

- Providing for children through college

Officers in good health without hazardous specialties may qualify for accelerated underwriting — approval without a traditional medical exam, which carriers like Banner Life offer for ages 20–60 up to $5 million. That's a convenient path for officers who can't easily schedule a paramedical appointment around shift work.

Whole Life Insurance

Whole life is permanent coverage with guaranteed lifelong protection, fixed premiums that never increase, and a cash value component that grows at a guaranteed rate. It costs significantly more than term, but the trade-off is predictability — the premium you pay at age 32 is the same at 62, and the policy never expires.

Some officers use whole life as part of a legacy planning strategy, building guaranteed cash value over decades that can be borrowed against or passed on to heirs.

Indexed Universal Life (IUL)

An IUL is a flexible permanent policy where the cash value grows based on the performance of a market index — typically the S&P 500 — with a floor that protects against losses. Some officers use IUL policies as a tax-advantaged supplement to pension income, accumulating cash value they can access in retirement.

LIMRA reports IUL new premium reached $4.5 billion in 2025, representing 25% of the individual life market — reflecting broader interest in this product type.

IULs are also the most complex of the three options. Before committing, understand how each of these factors affects your long-term results:

- Caps limit how much growth is credited in strong market years

- Participation rates determine what percentage of index gains apply to your policy

- Policy charges can erode cash value if not monitored over time

They work best when an advisor models realistic assumptions rather than optimistic projections.

Group Coverage Through Your Department or Union

Department coverage, FOP group plans, and similar association policies serve as a useful foundation — enrollment is straightforward, premiums are low, and no medical exam is required. But they work best as a supplement to individual coverage, not a replacement, given the portability limits and capped benefit amounts covered earlier.

Guaranteed Issue and Simplified Issue

Officers with health conditions that complicate traditional underwriting may have access to guaranteed issue or simplified issue policies. These policies ask few to no medical questions, making them accessible when standard underwriting isn't an option. The trade-offs to know upfront:

- Lower benefit limits than standard policies

- Graded benefit period — the full death benefit may not pay out if death occurs within the first two to three years

- Higher cost per dollar of coverage relative to medically underwritten policies

They're a practical fallback when standard underwriting isn't available, but work best as a supplemental layer rather than a primary solution.

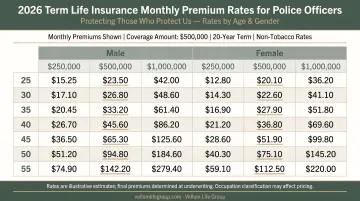

What Does Life Insurance Cost for Police Officers in 2026?

For a non-hazardous municipal officer in good health, term life premiums are often lower than most people expect. The table below shows approximate monthly premiums for a 20-year, $500,000 term policy for non-smokers, based on publicly available 2025–2026 benchmark data:

| Age | Female (Monthly) | Male (Monthly) |

|---|---|---|

| 25 | ~$21 | ~$25 |

| 30 | ~$24 | ~$28 |

| 40 | ~$35 | ~$35 |

| 50 | ~$71 | ~$93 |

These are representative benchmarks for non-smokers at standard or preferred health classes — not guaranteed quotes or police-specific rates. Actual premiums vary by carrier, health classification, and duty assignment.

What Drives Your Premium

- Age at application — the single largest factor; rates increase each year you wait

- Health classification — preferred rates go to applicants with clean medical histories

- Gender — statistically, women pay less for the same coverage

- Tobacco use — smokers pay significantly more across all carriers

- Duty assignment — hazardous specialties (SWAT, K-9, narcotics) may trigger a flat extra charge from some carriers

The Case for Acting Early

A 28-year-old officer who locks in a 30-year term policy secures that rate for the entire term. If they later transfer to a SWAT unit, develop a health condition, or face any other change — the premium doesn't move. Waiting even five years and buying the same policy at 33 means a higher base rate locked in for every year of that policy's life — often $20–$40 more per month, which adds up to thousands over a 30-year term.

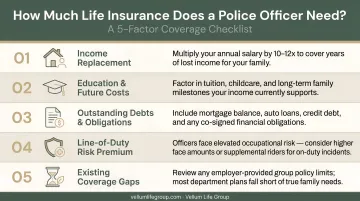

How to Determine the Right Coverage Amount

The "10 times your salary" rule is a starting point, not an answer. At a median officer salary of $77,270, that's roughly $772,000 — but the right number depends on your actual obligations.

Work through these inputs:

- Mortgage balance — what's left to pay off?

- Dependents — ages and number of children; estimated education costs (in-state four-year tuition averages $11,950/year; private nonprofit averages $45,000/year)

- Spouse's income — does your family lose 50% or 100% of household income?

- Existing savings and assets — what offsets the need?

- Income replacement years — how many years until your youngest child is independent?

LendingTree estimates raising a child through age 18 now costs approximately $303,418 on average. Against that figure, a $100,000 group policy covers less than a third of one child's upbringing — before a mortgage, lost income, or any other obligation enters the picture.

Think Beyond Your Active-Duty Years

Those calculations above reflect your needs today — but coverage should hold through your retirement age, not just your active-duty years. Individual policies travel with you through agency changes, promotions, and career transitions. Group coverage does not.

Annual policy reviews matter here. As debt decreases, children age out of dependence, and assets grow, the right coverage amount shifts. Eva Ikonomakos at Vellum Life Group builds annual reviews into every client relationship as a standard part of ongoing service — so coverage adjusts as your life does, rather than sitting static until something goes wrong.

Working through these numbers with an advisor who knows officer-specific coverage gaps is the most practical starting point. A free consultation with Vellum Life Group costs nothing and typically surfaces coverage needs — or redundancies — that most officers wouldn't catch on their own.

Frequently Asked Questions

What is a law enforcement IUL policy?

A law enforcement IUL is an Indexed Universal Life policy — a permanent policy that builds tax-advantaged cash value tied to a market index like the S&P 500, with a floor protecting against losses. Some officers use it as a supplemental retirement income strategy alongside their pension.

How much does a $1,000,000 law enforcement IUL policy cost per month?

Cost depends on your age, health, premium funding level, and how the policy is structured — there's no single published rate. A personalized illustration from a licensed advisor is the only accurate way to get a real number.

Can police officers get life insurance despite their high-risk job?

Yes. Most officers qualify for individual life insurance, often at standard or preferred rates. Working with an independent broker who understands law enforcement underwriting helps ensure you're matched to the carrier most likely to view your specific role favorably.

Is department or union life insurance enough for police officers?

For most officers with dependents, a mortgage, or significant financial obligations, group coverage alone falls short. It typically covers only 1–2x salary, doesn't travel with you after retirement, and can shrink in value as you age.

Does working in SWAT or a hazardous specialty affect my life insurance premiums?

It can. Hazardous specialties may trigger additional underwriting review and flat extra fees. Shopping your application across multiple carriers — with a broker who knows law enforcement underwriting — gives you the best shot at a competitive rate.

When is the best time for a police officer to buy life insurance?

The earlier, the better. Premiums are lowest when you're young and healthy, and locking in a rate now protects you against future increases — even if your health changes or your duty assignment becomes more hazardous down the road.