Dividend-paying whole life insurance is a permanent policy issued by a mutual insurance company that can return a share of the company's surplus earnings to policyholders each year. It's a feature many buyers overlook entirely, often because it's poorly explained at the point of sale.

This guide covers how dividends work, what drives them, the five ways to put them to use, their key benefits, and how to decide whether this policy type fits your financial situation.

Key Takeaways

- Mutual insurers offer participating whole life policies where policyholders — not shareholders — receive a share of annual surplus earnings

- Dividends are not guaranteed, yet leading mutual carriers have paid them for over 100 consecutive years

- Five dividend options exist, each serving a different financial goal — most policies let you change your election as your needs shift

- The IRS generally treats dividends as a return of premium, not taxable income

- The dividend interest rate is not your personal rate of return — actual cash value growth depends on policy design and time horizon

What Is Dividend-Paying Whole Life Insurance?

Dividend-paying whole life insurance is a form of permanent life insurance sold by mutual insurance companies — insurers owned by their policyholders rather than outside shareholders. Because policyholders are treated as partial owners, they "participate" in the company's financial results. That participation is what makes these policies officially called participating whole life policies.

Stock company policies work differently: any profits flow to shareholders, not policyholders. The mutual structure changes that equation entirely.

The Mutual Company Structure

The NAIC defines a mutual insurance company as one owned by its policyholders. Companies like New York Life, MassMutual, Guardian Life, Northwestern Mutual, and Penn Mutual operate under this structure — none answer to outside shareholders. When the company performs well, eligible policyholders share in that success through dividends.

As the NAIC explains, a life insurance dividend is a refund of part of the premium when the company's actual costs come in lower than projected.

What's Included in the Policy

Dividend-paying whole life carries the same core features as any whole life policy:

- Guaranteed death benefit — stays in place for life as long as premiums are paid, regardless of health changes

- Fixed premiums — locked in at issue, so they won't increase as you age or your health shifts

- Tax-deferred cash value — grows at a guaranteed minimum rate, building a financial asset inside the policy

Dividends are an additional, non-guaranteed layer of potential value on top of these guarantees — not a replacement for them.

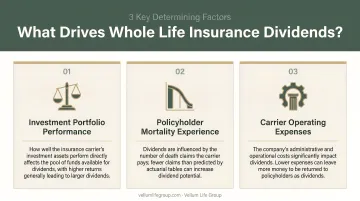

How Are Whole Life Insurance Dividends Determined?

Each year, a mutual insurer's board of directors evaluates the company's financial results and decides whether to declare a dividend and at what level. Three factors drive that decision:

- Investment performance: returns earned on the insurer's general account assets

- Mortality experience: whether actual death claims came in below actuarial projections

- Operating expenses: how closely the company's costs tracked its budget

When all three come in better than projected, a larger surplus is available to distribute. When results disappoint in one or more areas, the declared dividend may be lower.

Understanding what that declared rate actually means for your policy is where many people get tripped up.

The Dividend Rate vs. Your Actual Return

The dividend interest rate (DIR) is the rate used internally to calculate dividends. It does not represent what you personally earned on premiums paid.

A simple illustration: MassMutual's 2026 declared dividend interest rate is 6.60%, and Guardian's is 6.25%. But neither figure means a policyholder who paid $10,000 in premiums earned $660 or $625 that year. Your personal return depends on three things: how much cash value has accumulated, how the policy is structured (base premium vs. paid-up additions), and how long it has been in force. Early in a policy's life, the personal rate of return is typically well below the declared DIR.

Dividend Smoothing

Mutual insurers don't pass every investment gain or loss directly to policyholders in a single year. Instead, they spread performance results across multiple years — a practice called dividend smoothing. This is why long-term consistency matters more than any single year's rate, and why policies from well-run mutual companies tend to deliver stable dividends even through volatile markets.

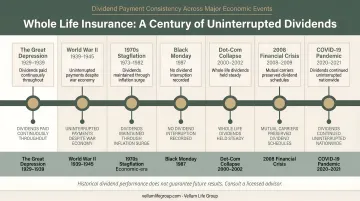

Historical Consistency

New York Life announced its 172nd consecutive annual dividend for 2026, having paid through the Civil War, the 1918 influenza pandemic, the Great Depression, and the 2008 financial crisis. MassMutual is in its 158th consecutive year, Guardian has paid every year since 1868, and Northwestern Mutual since 1872.

That track record doesn't guarantee future dividends (no insurer can), but it does demonstrate what a well-managed mutual company looks like over time.

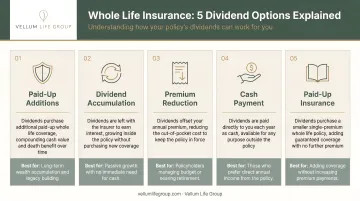

5 Ways to Use Your Whole Life Insurance Dividends

One of the most underappreciated aspects of participating whole life is the flexibility in how dividends can be applied. You're not locked into one approach — most carriers allow you to change your dividend election at any time, letting your strategy evolve as your financial needs shift.

Here are the five primary options:

1. Purchase Paid-Up Additions (PUAs)

Paid-up additions are small, fully paid-up units of additional whole life insurance purchased with your dividend. Each PUA increases both your death benefit and your cash value. Because PUAs are themselves participating, they can earn their own future dividends.

This compounding effect is why PUAs are the most popular dividend election. MassMutual confirms that paid-up additions are the most commonly elected option among its policyholders, and Northwestern Mutual echoes this. For policyholders focused on long-term wealth building, PUAs typically deliver the highest cumulative value.

2. Receive Dividends as Cash

Policyholders can receive their annual dividend as a direct payment — check or deposit. This cash is generally income tax-free (more on that below) and can be used however you'd like: living expenses, savings, or reinvestment elsewhere.

3. Reduce Premium Payments

Dividends can be applied to offset your next premium bill, lowering the out-of-pocket cost of keeping the policy in force. In years when the insurer performs well, this can meaningfully reduce what you spend on coverage — a practical option for budget-conscious policyholders.

4. Accumulate at Interest with the Insurer

You can leave dividends with the insurer in a separate account where they earn interest. The key tax caveat here: while the dividend itself is generally tax-free, any interest earned on accumulated dividends is taxable income in the year it's credited, per IRS Publication 525. It's worth choosing this election only if you have a specific near-term use in mind — otherwise, PUAs typically compound more efficiently over time.

5. Repay Outstanding Policy Loans

If you've borrowed against your policy's cash value, dividends can be directed toward loan repayment. This matters because unpaid policy loans accrue interest and can erode your death benefit over time. Directing dividends toward loan balances helps restore full policy performance and protects the coverage your beneficiaries depend on.

Key Benefits of Dividend-Paying Whole Life Insurance

Layered Financial Protection

Dividend-paying whole life provides three distinct layers of value from a single policy:

- Guaranteed death benefit — permanent protection regardless of age or health changes

- Guaranteed cash value growth — a minimum floor that never decreases due to market conditions

- Potential annual dividends — an additional non-guaranteed return tied to company performance

Term life provides only the first, and only for a fixed period. No market-linked investment provides the guaranteed floor.

Tax Efficiency

Few financial products carry as many tax advantages in one package:

- Cash value grows tax-deferred inside the policy

- Dividends are generally not taxable — the IRS treats them as a return of premium, not income, as long as total dividends received haven't exceeded total premiums paid

- Policy loans are typically income tax-free (with an exception for modified endowment contracts)

- Death benefits pass to beneficiaries income tax-free

Guardian's guidance on whole life tax benefits confirms that cash value is generally not taxed while growing inside the policy, and that loans against cash value are generally not treated as taxable income.

Stability Through Market Turbulence

The guaranteed cash value floor doesn't fluctuate with stock markets. Dividends, while not guaranteed, have been paid by leading mutual carriers through every major economic disruption of the past 150+ years. This predictability makes dividend-paying whole life a useful complement to market-linked investments, providing ballast without displacing growth-oriented assets.

Access to Cash Value During Your Lifetime

Policyholders can take loans against accumulated cash value for any purpose — supplementing retirement income, funding education, covering emergencies. These loans don't require credit approval or repayment on a fixed schedule. The trade-off: outstanding loans reduce both the death benefit and cash value, so they require careful management. The funds you access are your own accumulated cash value, with the policy itself serving as collateral.

Is Dividend-Paying Whole Life Insurance Right for You?

Who It Fits Well

This policy type tends to work best for someone who:

- Has a permanent insurance need — not just temporary income replacement during working years

- Has a time horizon of 10 or more years — the policy's economics improve materially over time

- Values financial predictability over the potential for higher market-linked returns

- Can commit to consistent premium payments — whole life premiums are substantially higher than term

LIMRA's 2025 market data shows whole life new premium reached $6.4 billion in 2025, up 7%, representing 37% of the total individual life market — a sign that permanent coverage is seeing renewed interest.

Who Might Be Better Served by Term + Investing Separately

If your primary need is income replacement during working years, or if your budget is limited, term life paired with a separate investment strategy may deliver more total value. The right answer depends on your goals, not a general rule.

What to Evaluate Before Buying

Before committing to a participating whole life policy, examine:

- Insurer financial strength: Look for A-rated carriers with multi-decade dividend records, not just current ratings

- Policy design: How premiums split between the base policy and paid-up additions drives long-term performance more than most buyers realize

- Whether your dividend election can change as your needs evolve — flexibility matters over a 20-30 year horizon

- Total cost vs. coverage goals: Get a detailed illustration with projected values, not just a headline premium figure

Because dividend-paying whole life is a long-term commitment, working with an independent advisor who can compare options across multiple A-rated carriers matters. A single-company agent can only show you one option.

Vellum Life Group works with more than 10 top-rated carriers and offers a free, no-pressure consultation to help you see the full picture before deciding. Reach Eva Ikonomakos at 917-363-3554 or book a conversation here.

Frequently Asked Questions

Are whole life insurance dividends guaranteed?

No. Dividends are declared annually by the insurer's board and can change year to year. That said, major mutual carriers like New York Life, MassMutual, Guardian, and Northwestern Mutual have paid dividends for over 100 consecutive years — through recessions, wars, and market downturns — a track record that reflects the resilience of well-managed mutual companies.

Are whole life insurance dividends taxable?

Generally no. The IRS treats life insurance dividends as a return of premium, reducing your cost basis rather than counting as income. They only become taxable if total dividends received exceed total premiums paid. One exception: interest earned on dividends left to accumulate with the insurer is taxable in the year it's credited.

What is the difference between the dividend rate and my actual return on a whole life policy?

The dividend interest rate is used internally by the insurer to calculate dividends — it's not your personal rate of return. Your actual return depends on accumulated cash value, policy structure, and how long the policy has been in force, and it typically runs well below the declared rate in the early years.

How much a month is a $1,000,000 whole life insurance policy?

Premiums vary widely based on your age, health, gender, insurer, and policy design. Whole life premiums are substantially higher than term because coverage is permanent and builds cash value. There's no single accurate figure without a personalized illustration — speak with an advisor for a quote specific to your profile.

How do I make $1,000 a month in dividends from a whole life policy?

Reaching meaningful monthly dividend income requires substantial, sustained premium investment over many years. The dividend amount depends on the insurer's annual performance and your policy's size and structure — this is a long-term wealth-building tool, not a quick-income strategy.

Can I change how my dividends are used after the policy is in force?

Yes, in most cases. Policyholders can typically change their dividend election at any time by notifying their insurer or financial advisor. This flexibility lets your dividend strategy adapt as your financial situation evolves.