Renewable term life insurance exists precisely for this moment. It's the built-in safety net that lets you extend coverage without proving you're still healthy enough to deserve it.

This guide covers what renewable term is, how it works, its real benefits and limitations, how it stacks up against other options, and who it actually makes sense for.

Key Takeaways

- Guaranteed renewability means you can extend coverage without a new medical exam, even if your health has declined

- Premiums rise at each renewal, recalculated by your age at the time, not your current health

- Renewal age caps vary by carrier and product; planning ahead before you hit that limit matters

- Renewable term builds no cash value; it provides pure death benefit protection only

- Best suited for short-term or uncertain coverage needs, not as a permanent solution

What Is Renewable Term Life Insurance and How Does It Work?

Renewable term life insurance is a standard term policy with one important addition: a guaranteed renewable clause. This clause gives you the right to extend coverage at the end of your term without reapplying or undergoing new health underwriting.

Per Insurance Compact standards, if a policy includes a renewable provision, the insurer cannot require new evidence of insurability at renewal. That's the core protection. Your renewal eligibility doesn't change because you were diagnosed with something between terms.

What does change is the premium. At renewal, your insurer recalculates the rate based on your current age — not your current health. The new premium follows a guaranteed schedule that was established when you first bought the policy.

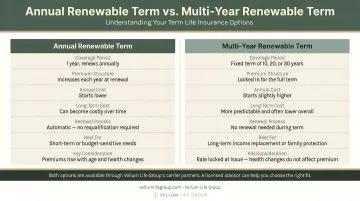

Annual Renewable Term vs. Multi-Year Renewable Term

Two structures exist, and they behave differently:

| Annual Renewable Term (ART) | Multi-Year Renewable Term | |

|---|---|---|

| Renewal cycle | One year at a time | Full term period (e.g., 5 years) |

| Premium changes | Adjust every year | Reset at the start of each new term |

| Cost pattern | Lower initial premiums; climbs faster over time | More stability within each term period |

Renewal age caps vary widely by carrier. Some insurers stop at 65 or 70; others extend renewal options to age 95. The terms will be spelled out in your policy contract — reading them before you need them is worth the time.

The Key Benefits of Renewable Term Life Insurance

Guaranteed Insurability When It Matters Most

If you develop a health condition between terms — high blood pressure, diabetes, a cancer diagnosis — you cannot be denied renewal or charged a higher premium because of it. Only age affects the renewal rate.

CDC data from 2023 shows that 78.4% of adults aged 35–64 had at least one chronic condition, and 52.7% had multiple chronic conditions. For anyone in that demographic who holds a renewable term policy, the guaranteed renewal clause removes one significant financial worry from an already complicated situation.

Lower Entry Cost Than Long-Term Alternatives

Because the coverage commitment is shorter, renewable term typically costs less upfront than locking in a 20- or 30-year level term or converting to permanent insurance. Forbes Advisor reports a $32/month average for a 35-year-old male purchasing $500,000 of 20-year level term coverage — and shorter-term renewable policies can start even lower, making them accessible during financially stretched periods.

Flexibility to Reassess as Life Changes

Coverage needs aren't static. A few events that frequently reduce or eliminate the need for coverage:

- Paying off a mortgage

- Children reaching financial independence

- Major financial changes (such as retirement or a large asset sale)

- Retirement (and the income it replaces)

Renewable term lets you evaluate at each renewal whether you still need the same coverage level — or any coverage at all — without having been locked into a 30-year commitment made at a very different life stage.

Bridge Coverage During Transitions

Renewable term can hold your protection in place while you're sorting out what comes next. Common situations where this matters:

- Waiting on a major financial event to close before committing to long-term coverage

- Planning to quit smoking (many carriers lower rates after 1–2 smoke-free years)

- Anticipating a life change that will clarify how much coverage you actually need

The Drawbacks to Consider

Premiums Escalate — Sometimes Steeply

Every renewal resets your premium at your attained age. Early renewals may feel manageable, but the cost curve gets steeper as you move into your 50s and 60s. Continuously renewing a short-term policy over 20 years typically results in a higher total cost than locking in a 20-year level term at a younger age. The math favors level term for people with known, long-duration needs.

There's an End Point

Renewable term is not permanent coverage. When you hit the policy's maximum renewal age or exhaust the number of allowed renewals, coverage ends with no path to renewal. Anyone who needs lifelong protection, plans to leave a legacy death benefit, or has estate planning needs should not treat renewable term as a long-term solution.

No Cash Value

Like all term insurance, renewable term builds nothing beyond a death benefit. That means:

- No savings component that grows over time

- No ability to borrow against the policy

- No return of premium unless you've added a specific rider

The trade-off is deliberate: lower ongoing cost in exchange for no financial accumulation.

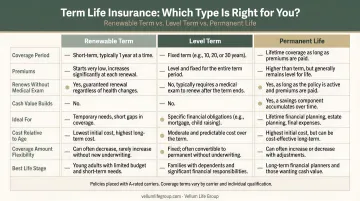

Renewable Term vs. Your Other Options

Before choosing any coverage structure, it helps to see the differences clearly:

| Feature | Renewable Term | Level Term | Permanent Life |

|---|---|---|---|

| Premium trajectory | Rises at each renewal | Fixed for full term | Fixed or predictable for life |

| Coverage duration | Short-term, renewable to age cap | Fixed term (10/20/30 years) | Lifetime |

| Cash value | None | None | Yes (whole/universal) |

| Renewability | Yes, without new underwriting | No (must reapply) | N/A — doesn't expire |

| Ideal use case | Uncertain or short-term need | Defined long-term obligation | Legacy, estate planning, lifetime need |

Renewable Term vs. Level Term

Level term wins on cost predictability over the long run. If you have a 30-year mortgage or dependents who'll need support for two decades, locking in a level rate at a younger, healthier age is almost always cheaper in total. Renewable term is the better fit when you genuinely don't know how long you'll need coverage.

Renewable Term vs. Convertible Term

Convertible term lets you switch to permanent coverage without a new medical exam, protecting your insurability permanently. The trade-off is that permanent premiums are much higher than renewed term premiums, especially in early years. Some policies offer both renewable and convertible features — worth asking about when you shop.

Renewable Term vs. Permanent Life

Permanent coverage — whole or universal life — never expires and builds cash value. It suits people with estate planning goals, lifetime income replacement needs, or anyone who wants a guaranteed death benefit no matter when they die. The cost is significantly higher, but for the right situation, it's the right tool.

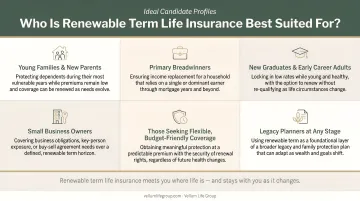

Who Is Renewable Term Life Insurance Best For?

Renewable term makes the most sense for specific situations. Here's an honest breakdown:

Renewable term is a strong fit if you are:

- People who need affordable coverage now but aren't certain how long they'll need it

- Those with a family history of illness or personal health concerns who want to lock in renewability early

- Smokers or people with lifestyle factors affecting rates who plan to change (and want bridge coverage while they do)

- Anyone navigating a major transition — new job, new baby, legacy planning — who isn't ready to commit to a 20-year rate

- The 42 million U.S. adults who say they need more life insurance coverage but face budget or health barriers to longer-term options

Other products are likely a better match if you:

- People who know they need coverage for 20+ years — level term locked in young is usually cheaper overall

- Anyone who wants lifelong protection or to build cash value — permanent insurance is the right answer

- Those with estate planning or legacy goals that outlast any term policy

The key question is simple: How certain am I about how long I'll need this coverage? The clearer the answer, the easier the decision.

If that answer still feels fuzzy, a side-by-side comparison usually clears it up. Working with an independent advisor like Eva Ikonomakos at Vellum Life Group means access to 10+ A-rated carriers and a no-pressure look at renewable term, level term, and convertible options together — so the differences become concrete, not theoretical.

How to Get the Right Renewable Term Policy

What to Look for in the Policy Contract

Not all term policies include a guaranteed renewable clause — it's a feature, not a default. Before signing anything, confirm:

- The guaranteed renewable provision is explicitly stated in the contract

- The maximum renewal age (and whether it fits your planning timeline)

- How frequently premiums reset and what the guaranteed maximum schedule looks like

- Whether a conversion option is also included

The Application Process

Many term policies — including those with renewable clauses — can be approved quickly. Guardian notes that life underwriting can take as little as 24 hours, though traditional underwriting can extend to 4–6 weeks depending on the applicant's health profile and whether a medical exam is required.

LIMRA noted in 2020 that for eligible applicants, accelerated underwriting can allow medical requirements like a paramedical exam to be waived entirely.

Working with an independent advisor rather than a single carrier's agent matters here. The NAIC distinguishes between independent agents — who access multiple carriers — and captive agents, who can only offer one company's products. When you're evaluating renewable term, level term, or convertible policies side by side, carrier selection makes a real difference in both features and price.

Vellum Life Group operates as an independent advisor with access to 15+ A-rated carriers, which means you get a side-by-side comparison — not a single company's pitch. The free consultation includes a custom quote and a 24-hour response time, with no obligation to move forward.

Frequently Asked Questions

What is renewable term life insurance?

Renewable term life insurance is a term policy with a built-in clause allowing you to extend coverage at the end of the term without a new medical exam. Renewal premiums are adjusted upward based on your age at renewal, not your current health status.

Does taking Lexapro affect my ability to get renewable term life insurance?

If you already hold a renewable term policy, renewing it doesn't require new health underwriting — so a current medication like Lexapro won't affect your renewal eligibility or premium. For a new application, insurers evaluate mental health history on a case-by-case basis, and outcomes vary by carrier — working with an independent advisor helps identify the most favorable option.

What happens when my renewable term policy reaches the age limit?

Once you hit the policy's maximum renewal age, coverage ends with no further extension option. Plan ahead by converting to permanent coverage or purchasing a new policy before reaching that limit, while health and age are still working in your favor.

Is renewable term more expensive than level term over time?

Yes. While renewable term starts with lower premiums, continuously renewing a short-term policy over many years typically costs more in total than locking in a 20- or 30-year level term rate at a younger age. The escalating renewal premiums add up.

Can I convert my renewable term policy to permanent coverage?

Some renewable term policies also include a conversion option, allowing you to switch to permanent coverage without a medical exam. Not all policies offer both features, so confirm this at purchase — it's far simpler to confirm upfront than to discover the option is missing when you need it.

How do I know if my current term policy is renewable?

Check your policy documents for a "guaranteed renewable" or "renewability" clause. If you can't locate it, contact your insurer or advisor directly. Most term policies include this feature, but age limits, premium schedules, and renewal frequency vary by contract.