Introduction

If people depend on your income, the most important financial decision you can make is also one of the simplest: putting an affordable safety net in place so your family stays secure if you're no longer there to provide for them. For most families, term life insurance is the most direct and cost-effective way to do exactly that.

Term life insurance pays a lump sum to the people you love if you die during the policy's term. It is straightforward, predictable, and inexpensive relative to the protection it provides — which is why it remains the cornerstone of family financial planning.

This guide breaks down what individual term life insurance is, how it works, how to choose the right term length and coverage amount, what drives the cost, and the riders that can tailor a policy to your family's real needs.

Key Takeaways

- Individual term life insurance pays a tax-free lump-sum death benefit if you die during a set term, usually 10 to 30 years

- Because you own the policy personally, it stays with you regardless of your coverage status or what happens to any group plan

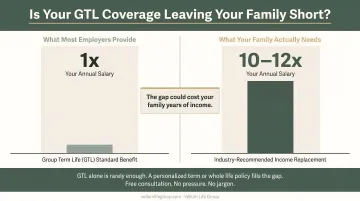

- Most planners suggest coverage of roughly 10–12x your annual income, sized to replace earnings and clear debts

- Premiums are locked in for the level term and are driven mainly by age, health, term length, and coverage amount

- Riders such as waiver of premium, accelerated death benefit, and child riders let you customize coverage to your situation

What Is Term Life Insurance?

Term life insurance is a policy you own that pays a death benefit to your named beneficiaries if you pass away during a defined period — the "term." If the term ends and you're still living, coverage simply expires (or can often be renewed or converted).

The name itself explains the structure:

- Term — coverage lasts for a fixed period you choose, commonly 10, 15, 20, 25, or 30 years

- Life insurance — it pays a lump-sum death benefit to the beneficiaries you name

- Individual — you apply for it, you own it, and you control it, independent of any job

Why "Individual" Matters

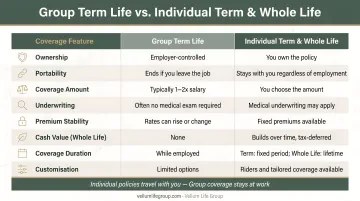

With an individually owned policy, the coverage belongs to you. You name the beneficiaries, you choose the amount and term, and the policy follows you through job changes, moves, and life transitions. A workplace or group plan, by contrast, is generally limited in size, isn't owned by you, and ends when the job does — which is precisely why a personally owned policy is the dependable foundation families rely on.

Typical Coverage Amounts

Policies are commonly written from $100,000 up to several million dollars. The right number isn't a guess — it's tied to what your family would need to replace your income, pay off debts, and cover future goals like education. We'll walk through how to size it below.

Term Life vs. Whole Life

| Type | Coverage Length | Cash Value? | Cost |

|---|---|---|---|

| Term Life | Fixed term (10–30 yrs) | No | Lowest premium |

| Whole Life | Lifetime | Yes | Higher premium |

| Universal Life | Lifetime, flexible | Yes | Moderate to high |

For most families, term life delivers the largest death benefit for the lowest cost during the years protection matters most — while children are at home and the mortgage is being paid down.

How Term Life Insurance Works

Applying and Underwriting

Unlike automatic group enrollment, an individual policy is something you apply for. You complete an application about your health, lifestyle, and finances, and most policies involve underwriting — a review that may include a brief medical exam or health records. The healthier you are and the younger you apply, the lower your locked-in rate.

Choosing Your Beneficiaries

You name who receives the death benefit — a spouse, children, a trust, or any combination. Review your beneficiary designations after major life events such as marriage, divorce, or the birth of a child, so the payout always goes to the people you intend.

Paying Premiums

With level term life, your premium is fixed for the entire term. A 20-year policy keeps the same monthly cost for all 20 years, making it easy to budget. As long as premiums are paid, the coverage stays in force.

Filing a Claim

If you pass away during the term, the insurer pays the death benefit directly to your beneficiaries — typically as a federal income tax-free lump sum. They can use it however they need: covering the mortgage, replacing income, funding college, or paying final expenses.

What Happens When the Term Ends

When the level term expires, you generally have options. Many policies are renewable (at higher rates) and convertible to permanent coverage without a new medical exam. If your needs have changed — the mortgage is paid, the kids are grown — you may simply let it lapse.

Choosing the Right Term Length

The goal is to match the term to the years your family is financially dependent on you.

- 10–15 years — a good fit if you're closer to paying off the house or your children are nearing independence

- 20 years — the most popular choice, often aligned with raising children and a typical mortgage

- 25–30 years — ideal for young parents who want protection through the full span of child-rearing and a long mortgage

A practical rule: choose a term that runs at least until your youngest child is financially independent and your largest debts are paid off.

How Much Coverage Do You Need?

Under-insuring is the most common and costly mistake families make. A useful starting point cited by financial planners such as Fidelity is 10–12x your annual income, but you can size it more precisely.

Add up what your family would need to:

- Replace your income for the years your family depends on it

- Pay off the mortgage and other major debts

- Cover future costs such as childcare and college tuition

- Handle final expenses like funeral and medical bills

Then subtract existing savings and any other resources. The difference is roughly the coverage gap your policy should fill.

Example: A parent earning $65,000 with a $250,000 mortgage and two young children might need $250,000 to clear the mortgage plus 10x income ($650,000) to replace earnings — pointing toward roughly $900,000 in coverage, adjusted for savings and education goals.

What Affects the Cost of Term Life Insurance

Term life is remarkably affordable, but several factors shape your premium:

- Age — the single biggest factor; rates climb with each year you wait

- Health — blood pressure, cholesterol, weight, and medical history all matter

- Tobacco use — smokers pay significantly more

- Term length — longer terms cost more because the insurer covers more years

- Coverage amount — a larger death benefit means a higher premium

- Gender and family history — actuarial factors that influence risk

The cost is often lower than people expect. A healthy 30-year-old can frequently secure $500,000 in 20-year term coverage for under $30 per month — protection that stays in place regardless of where you work.

Common Term Life Riders

Riders let you customize a policy to your family's needs:

- Waiver of premium — keeps coverage active without payments if you become disabled and can't work

- Accelerated death benefit — lets you access part of the benefit early if you're diagnosed with a qualifying terminal illness

- Child term rider — adds modest coverage for your children under your policy

- Return of premium — refunds premiums paid if you outlive the term, in exchange for a higher cost

- Conversion option — allows you to convert to permanent coverage later without new underwriting

Why a Personally Owned Policy Protects Your Family

Many people assume that whatever life coverage they have through work is enough. In reality, workplace or group coverage is typically limited in amount and, crucially, not portable — it generally ends the moment you leave that job, whether you resign, are laid off, or retire. That can leave a gap exactly when replacing coverage becomes harder or more expensive due to age or health changes.

An individually owned term policy solves this. Because you own it:

- It stays in force through every job change, move, or career break

- You choose a coverage amount sized to your family's real needs, not a fixed plan limit

- Your rate is locked in based on your age and health today

- You control the beneficiaries and the policy on your own terms

That independence is why a personally owned policy is the reliable foundation of family protection.

Self-Assessment Questions

Work through these to gauge whether your coverage is adequate:

- How many people depend on your income?

- What debts would your family inherit — mortgage, student loans, car payments?

- Do you have enough savings to cover 10+ years of income replacement?

- If you passed away tomorrow, could your family stay in their home and meet their goals?

If you answered "no" or "I'm not sure" to any of these, it may be time to put a policy in place — or increase what you have.

Getting Personalized Guidance

An independent advisor — one who shops options across multiple carriers rather than representing a single company — makes it easier to find coverage that fits your needs and your budget.

At Vellum Life Group, founder Eva Ikonomakos offers free, no-obligation consultations to help individuals and families find the right coverage. With access to 15+ A-rated carriers and 15+ years of experience across financial services, her goal is straightforward: help you understand your options clearly, without pressure.

To book a free 30-minute consultation, visit calendly.com/eva-ikonomakos/30min or call 917-363-3554.

Frequently Asked Questions

What is term life insurance?

Term life insurance is a policy you own that pays a tax-free lump-sum death benefit to your named beneficiaries if you die during a set period — commonly 10 to 30 years. It offers the most coverage for the lowest cost during the years your family depends on your income.

How much term life insurance do I need?

A common starting point is 10–12x your annual income, but the most accurate approach adds up what your family would need to replace your income, pay off the mortgage and debts, fund future goals like college, and cover final expenses — then subtracts existing savings. A family-focused review can help you pin down the number.

How long should the term be?

Choose a term that lasts at least until your youngest child is financially independent and your largest debts, such as a mortgage, are paid off. Twenty years is the most popular choice, while young parents often opt for 25 or 30 years.

Is term life insurance a good idea?

For most families, yes. It provides substantial protection at a low, predictable cost, and because you own it personally, it stays with you no matter where you work. It is the dependable foundation of a family financial safety net.

Will I need a medical exam?

Many individual term policies involve some underwriting, which can include a brief medical exam or a review of your health records. Applying while you're younger and healthier generally locks in the lowest rate for the life of the term.