Most seniors deserve a straight answer rather than more marketing spin. The reality is more nuanced than the ads suggest, but it's also more manageable than you might fear. According to the NFDA, the national median cost of a funeral with viewing and burial was $8,300 in 2023, and cremation averaged $6,280. That's a real financial burden — and it lands on families fast.

This article explains what "free burial insurance" actually means, what government help genuinely exists, and what affordable coverage realistically looks like for seniors today.

Key Takeaways

- Truly free burial insurance doesn't exist — any policy with a meaningful death benefit requires monthly premiums

- Government programs like Social Security and VA burial benefits provide partial help, not full funeral coverage

- Most seniors ages 50–85 qualify for some form of burial insurance, even with serious health conditions

- Premiums lock in at purchase and never increase, so waiting only costs more

The Truth About "Free" Burial Insurance Ads

What Those Ads Are Actually Selling

The TV commercials, mailers, and online ads using phrases like "a final expense benefit available to seniors" are almost always advertisements for paid insurance products. The word "benefit" does the heavy lifting here — it implies an entitlement, something owed to you, rather than a product you'd purchase.

One of the most widely advertised examples is Colonial Penn's Guaranteed Acceptance Life Insurance, which starts at $9.95 per month. That price is real. What the ads don't emphasize clearly: $9.95 buys one "unit" of coverage, and the actual death benefit that unit provides depends entirely on your age, gender, and state of residence. For older applicants, a single unit at that price may provide a death benefit far below what a real funeral costs.

The South Carolina Department of Insurance issued a Consumer Fraud Alert specifically warning seniors about misleading final expense coverage solicitations — a sign that consumer confusion in this space is widespread enough to draw regulatory attention.

Why Free Burial Insurance Can't Exist

The economics are straightforward: insurance companies pool premiums from many policyholders to fund death benefits. Remove the premiums, and there's no pool of money to pay claims. No private insurer can offer genuine, no-cost coverage: without premiums, there's nothing to pay claims with.

The "final expense benefit you may be missing" framing is a marketing hook, not a reference to a secret government program. Real government assistance does exist — but it's limited in scope and won't cover a full funeral on its own.

If you're searching for free burial insurance, you deserve a straight answer: it doesn't exist as a private product. What does exist are legitimate low-cost options and partial government assistance — both worth understanding clearly.

What Government Help Is Actually Available for Burial Costs

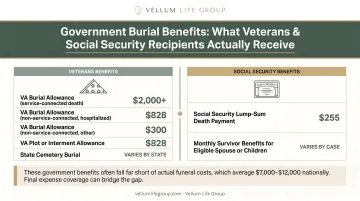

Social Security Lump-Sum Death Benefit

Social Security pays a one-time lump-sum death payment of $255 upon the death of a qualifying worker. That figure hasn't changed in decades.

Who can receive it:

- A surviving spouse who was living with the deceased

- In some cases, a dependent child (age 17 or younger, or 18–19 if attending K-12 full time, or any age if disabled before age 22)

Survivors must apply within two years of the death — against an $8,300 median funeral cost, that $255 covers roughly 3% of expenses.

VA Burial Benefits

Eligible veterans have meaningful options worth understanding:

- National cemetery burial at no cost — gravesite, opening and closing of the grave, government headstone, burial flag, and perpetual care are all included for eligible veterans

- Service-connected death allowance — up to $2,000 toward burial expenses for deaths on or after September 11, 2001

- Non-service-connected death allowance — for deaths on or after October 1, 2025, a $1,002 burial allowance plus a $1,002 plot or interment allowance applies

Eligibility depends on the veteran's discharge status and the circumstances of death. Spouses and qualifying dependents may also be eligible for national cemetery burial.

State and Local Assistance Programs

Some states and counties offer burial assistance for low-income individuals with no means to cover funeral costs. A few examples:

- Massachusetts: Up to $1,100 when total costs don't exceed $3,500

- Michigan: Up to $875 for burial with memorial, $640 for cremation with memorial

- Maryland: Payment goes directly to the funeral director; already-paid expenses cannot be reimbursed

These programs differ widely by location and are reserved for very low-income households. Qualifying typically means accepting minimal arrangements with little say over the details.

Even the most generous option here tops out around $2,000 — a fraction of the $8,300 median funeral cost. For most families, government assistance can reduce the burden, but it won't eliminate it.

What Is Burial Insurance and How Does It Actually Work

Burial insurance — also called final expense insurance or funeral insurance — is a type of permanent whole life insurance designed specifically to cover end-of-life expenses. Coverage amounts typically range from $5,000 to $25,000, which aligns with the NFDA's reported funeral cost benchmarks.

Two Policy Types Seniors Will Encounter

| Policy Type | Health Requirements | Waiting Period | Premium Level | Best For |

|---|---|---|---|---|

| Simplified Issue | Short health questionnaire; no medical exam | Usually none — full coverage from day one | Lower | Seniors in reasonably good health |

| Guaranteed Issue | No health questions; guaranteed approval | 2-year waiting period for non-accidental death | Higher | Seniors with serious health conditions or prior declinations |

The waiting period on guaranteed issue policies is worth understanding before you buy. If the insured passes away from natural causes during the first two years, beneficiaries typically receive all premiums paid plus 10% — not the full death benefit. After two years, the full benefit pays out for all causes of death. Accidental death is covered in full from day one.

Core Features That Make Burial Insurance Work for Seniors

- Premiums are locked in at purchase and never increase — a standard feature across carriers like Mutual of Omaha and Colonial Penn

- Coverage is permanent — it doesn't expire at age 80 or after a set term

- No medical exam required for either policy type

- Death benefit pays in cash directly to the named beneficiary, usually within days, with no restrictions on use

The beneficiary can use the money for funeral director fees, casket or urn, burial plot or cremation, headstone, outstanding medical bills, or anything else the family needs. Any amount remaining after expenses belongs to them.

How Much Does Burial Insurance Actually Cost for Seniors

What Drives Your Premium

Six factors determine what you'll pay each month:

- Age at purchase — the single biggest factor

- Gender — women typically pay less

- Tobacco use — smokers pay more

- Health history — relevant for simplified issue policies

- Coverage amount selected

- Policy type — guaranteed issue costs more than simplified issue

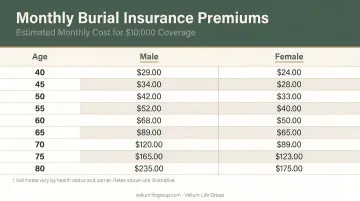

Sample Monthly Premium Estimates

The following estimates for $10,000 in coverage are based on Forbes Advisor's burial insurance analysis using averages from the three least expensive guaranteed issue quotes. These are estimates, not carrier-guaranteed rates — actual quotes will vary.

| Age | Male (Est.) | Female (Est.) |

|---|---|---|

| 60 | ~$63/month | ~$49/month |

| 70 | ~$97/month | ~$73/month |

| 80 | ~$197/month | ~$158/month |

The Real Cost of Waiting

Those rate differences by age aren't just numbers in a table — they're locked in the moment you apply. A 65-year-old buying a $10,000 policy today pays that lower rate for life. Wait until 75, and the same policy costs significantly more every single month, permanently. Since premiums never reset, every year of delay adds to what you'll owe for as long as you hold the policy. The earlier you lock in a rate, the less you pay over time.

Who Qualifies — and How to Find the Right Coverage

Most seniors between ages 50 and 85 qualify for some form of burial insurance. Carriers like Colonial Penn and Mutual of Omaha both offer guaranteed acceptance products up to age 85.

If you have serious health conditions — COPD, diabetes, heart disease, a history of cancer — guaranteed issue policies ask no health questions. Approval is based on age and state of residence alone, so being declined elsewhere doesn't close the door on coverage.

Simplified Issue vs. Guaranteed Issue: Which One Applies to You

- Good to excellent health? Simplified issue likely gives you better coverage with lower premiums and no waiting period

- Serious health conditions or prior declinations? Guaranteed issue gets you covered — the trade-off is a 2-year waiting period and higher premiums

How to Find the Best Rate

Once you know which policy type fits your health profile, the next step is finding the best rate. Going directly to a single carrier means you see one price — and no alternatives. An independent advisor compares multiple A-rated carriers at once, which typically surfaces lower premiums for the same coverage.

Vellum Life Group works with 15+ A-rated carriers including Mutual of Omaha, Aflac, Americo, Foresters Financial, and Transamerica, among others. Their process is straightforward:

- Start with a free, no-obligation call to discuss your health, budget, and coverage needs

- Receive side-by-side quotes from multiple carriers tailored to your profile

- Complete a simple application — many policies are approved the same day or within a few days

- Get ongoing support including annual reviews and claims assistance, included at no extra cost

To get started, reach Vellum Life Group through any of these channels:

- Phone: 917-363-3554

- Email: info@vellumlifegroup.com

- Book online: calendly.com/eva-ikonomakos/30min

Frequently Asked Questions

Is there really a final expense benefit for seniors?

No secret government entitlement called "final expense insurance" exists. That phrase is used in marketing for paid life insurance products. Social Security's $255 death payment and VA burial benefits are real but limited — neither comes close to covering a full funeral.

What is the $25,000 final expense package?

This refers to a private burial insurance policy with a $25,000 death benefit — not a government program. These policies require monthly premiums and are available from multiple carriers, with eligibility based on age and health history.

Who gets the $25,000 death benefit?

The death benefit pays directly to the named beneficiary — typically a spouse, adult child, or trusted family member — as a tax-free cash payment. They can use it for funeral costs or any other purpose.

What is the Social Security death benefit for seniors?

Social Security's lump-sum death payment is $255. It's a one-time payment — not an ongoing benefit — available to a surviving spouse who lived with the deceased, or in some cases a qualifying dependent child. It does not come close to covering funeral expenses.

Can seniors with health problems still get burial insurance?

Yes. Guaranteed issue burial insurance is available for seniors up to age 85 with no health questions asked — approval is guaranteed regardless of medical history. A 2-year waiting period applies to non-accidental deaths, but accidental death is covered from day one.

How much does burial insurance typically cost per month for a senior?

Costs vary by age, gender, health, and coverage amount. As a general reference, a 70-year-old seeking $10,000 in coverage might pay roughly $73–$97 per month depending on gender and policy type. Working with an independent advisor like Vellum Life Group — which compares rates across 15+ carriers — helps you find the most competitive option for your situation.