According to LIMRA's 2025 Insurance Barometer Study, roughly 40% of American adults — close to 100 million people — say they need more life insurance than they currently have. That gap is the difference between a family that weathers a tragedy and one that doesn't.

This guide covers the four core insurance types families should consider for income protection, how to calculate the right coverage amounts, and how to layer policies so no single risk goes unaddressed.

Key Takeaways

- Term life insurance delivers the most coverage per dollar — typically recommended at 10–12x your annual salary

- Permanent/whole life insurance provides lifelong coverage plus cash value, making it valuable for legacy and estate planning

- Universal life insurance offers flexible premiums and adjustable coverage as your family's needs change over time

- Final expense insurance ensures end-of-life costs don't become a financial burden for the people you leave behind

- The strongest family income protection combines term, permanent, and supplemental life policies tailored to your stage of life

Best Insurance Options for Protecting Your Family's Income

These four coverage types form the foundation of a family income protection plan. Each addresses a different financial risk that savings alone cannot reliably cover.

Term Life Insurance

Term life insurance pays a death benefit if the insured passes away within a defined period — typically 10, 20, or 30 years — with premiums that stay level throughout the term. It's the most widely recommended option for families with dependents, outstanding mortgages, or young children, primarily because it delivers the highest coverage amounts at the lowest monthly cost.

A healthy 30-year-old can often secure $500,000 in term coverage for under $30 per month — making it the most practical starting point for families balancing protection with budget.

Key considerations at a glance:

| Feature | Details |

|---|---|

| Term lengths | 10, 20, or 30 years (standard) |

| Best for | Income replacement during peak earning/dependency years |

| Cash value | None |

| Premium stability | Level throughout the term |

| Coverage end | Policy expires when term ends — no payout if still living |

Vellum Life Group offers term policies through 15+ A-rated carriers including Corebridge Financial, Mutual of Omaha, Transamerica, and Ameritas, allowing families to compare rates and find the most competitive fit for their situation.

Permanent (Whole Life) Insurance

Whole life insurance provides coverage that never expires, as long as premiums are paid. Unlike term, it includes a cash value component that grows over time and can be borrowed against or surrendered — making it both a protection tool and a long-term financial asset.

Where term covers a defined window, whole life ensures a death benefit is available regardless of when the insured dies — at 45 or 85. It's particularly useful for:

- Final expense coverage

- Legacy and estate transfers

- Long-term wealth building

- Situations where the insured may outlive a term policy

Key considerations:

- Premiums are significantly higher than term for the same death benefit

- Premium rates are locked in at the time of purchase

- Cash value accumulates over time and can be accessed through loans or withdrawals

- Best suited for families who want lifelong protection and are financially prepared for higher premiums

For context, a $500,000 whole life policy for a healthy 30-year-old nonsmoker runs around $440/month on average, compared to under $30/month for comparable term coverage. That gap is worth factoring into any coverage decision.

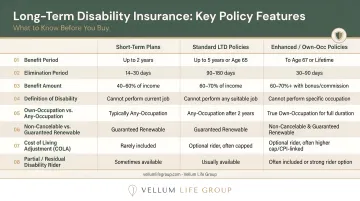

Long-Term Disability Insurance

Long-term disability (LTD) insurance protects income when a policyholder is alive but unable to work due to illness or injury. It's the coverage most families overlook, even though statistically it's among the most likely risks they'll actually face.

The Social Security Administration reports that a 20-year-old worker has a 1-in-4 chance of developing a disability before reaching full retirement age. Yet according to LIMRA, only about 18% of consumers say they have disability insurance, and at least 51 million working adults lack coverage beyond Social Security.

LTD typically replaces 50–70% of pre-disability income, covering mortgage payments, daily expenses, and debt obligations during recovery or permanent disability. Most life insurance only pays on death — LTD fills the equally devastating gap of being alive but unable to earn.

Key policy features to compare:

- Elimination period: How long before benefits begin — commonly 90 days, though some plans extend to 6 months

- Benefit period: Length of payments — ranges from a few years to retirement age

- Definition of disability: "Own-occupation" (can't do your specific job) vs. "any-occupation" (can't do any job) — a critical distinction

- Source: Group LTD through a group plan (only 37% of private-industry individuals have access) vs. individual policies you own independently

Note: Disability insurance falls outside Vellum Life Group's current service offerings. This section is included because LTD is a critical component of any complete family income protection plan — and knowing the landscape helps you ask the right questions with the right provider.

Health Insurance

Health insurance doesn't replace income directly, but it prevents medical bills from destroying everything else. KFF estimates at least $220 billion in U.S. medical debt, with 14 million adults owing more than $1,000 in medical costs. A single hospitalization without adequate coverage can drain an emergency fund and push a family into debt that takes years to recover from.

Main paths to coverage:

- Group-sponsored plans: Most cost-effective for salaried individuals — Census data shows roughly 53.8% of Americans have plan-based coverage

- ACA Marketplace: Subsidized options for those without group coverage; families of four earning between $33,000–$132,000 may qualify for premium tax credits

- Medicaid: Covers approximately 17.6% of Americans, primarily lower-income families

- Individual/private plans: Available for the self-directed or those between plans

When reviewing health plans, pay close attention to premiums, deductibles, out-of-pocket maximums, and in-network provider access — especially after major life changes like a new child or job transition.

Note: Health insurance is outside Vellum Life Group's scope. The information above is provided for context — a complete income protection strategy requires coordination across multiple coverage types, and life insurance is where Vellum Life Group can help.

How Much Coverage Does Your Family Actually Need?

The Income Replacement Rule of Thumb

Most financial planners use 10–12x annual salary as a baseline for life insurance coverage. Life Happens, a nonprofit supported by major insurance industry organizations, recommends starting at 10–15x gross income as a rough estimate. For a household earning $80,000 per year, that translates to a coverage target of $800,000 to $1.2 million.

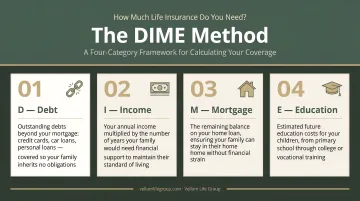

The DIME Framework

For a more precise number, the DIME method walks through four categories:

- Debt — All outstanding loans (auto, credit cards, student loans) outside of the mortgage

- Income — Annual salary × number of years until the youngest dependent is financially independent

- Mortgage — Full remaining balance on the home

- Education — Projected college costs for each child

Add those four together and you get a coverage target grounded in your actual financial obligations — not just a rule of thumb.

Dual-Income and Stay-at-Home Households

In dual-income households, both earners need their own policies. Losing either income creates real financial hardship, even if the surviving spouse continues working.

The same logic applies to stay-at-home parents. Salary.com estimates the annual value of a stay-at-home parent's contributions — childcare, household management, transportation, and related services — at approximately $178,201 per year. A surviving spouse would need to replace those functions, and life insurance is what makes that financially possible.

Coverage Needs by Life Stage

Your coverage needs shift at every major milestone — what was right five years ago may leave your family underprotected today:

- New parents: Maximum coverage need — more years of dependency, full mortgage, new childcare costs

- Mid-career families: Reassess as income grows and debts decrease

- Empty nesters: Coverage need often decreases, though legacy goals may sustain higher amounts

- Trigger events to review: Marriage, new child, home purchase, income change, job transition

Any of these milestones is a good reason to revisit your current policy — or get a first one in place.

How to Build a Layered Protection Strategy

No single policy covers every risk. A complete protection plan typically rests on three pillars: health coverage, disability insurance, and life insurance. Each addresses a distinct scenario, and removing any one leaves a gap the others can't fill.

Life insurance is the cornerstone Vellum Life Group helps families build — but it works best alongside disability and health coverage sourced from the appropriate specialists. Here's how the three fit together:

- Health insurance covers medical costs directly (through a group plan or a separate health plan)

- Disability insurance replaces income if you're alive but unable to earn (typically plan-based or through a disability specialist)

- Life insurance protects your family financially after the breadwinner's death — and is where thoughtful policy design makes the biggest difference

Prioritizing When Budget Is Limited

If a family can't fund everything at once, here's a practical sequencing:

- Term life first — highest income replacement impact per dollar, especially for families with dependents

- Long-term disability second — particularly if not covered through a group plan (only 37% of private-industry individuals have access, according to the U.S. Bureau of Labor Statistics — add source link)

- Health insurance third — often plan-based, but a critical gap if it isn't

As budget grows, consider adding permanent life insurance for legacy goals, or policy riders to extend a base policy's protection without purchasing entirely new coverage.

The Value of Policy Riders

Riders let families expand coverage without buying separate policies. Common options worth asking about include:

- Accelerated death benefit — access a portion of the death benefit if diagnosed with a terminal illness

- Waiver of premium — premiums are waived if the insured becomes disabled

- Child term rider — adds coverage for minor children at low cost

- Disability income rider — adds income replacement to a life insurance policy

These riders won't replicate standalone disability or health insurance, but they can meaningfully strengthen a base policy for a relatively modest additional premium.

Common Mistakes Families Make With Income Protection Insurance

Relying Solely on Group Life Coverage

LIMRA's 2025 workplace data shows the median basic group life coverage is $20,000 or 1x salary — and 49% of households relying only on group plan coverage would struggle financially within six months after a wage-earner's death. Worse, that coverage isn't portable. It ends when the group plan lapses.

Individual policies you own and control are the only reliable foundation. Group coverage can supplement — it shouldn't serve as the primary plan.

The Underinsurance Trap

Many families select lower coverage to save on premiums without realizing what that shortfall actually means. Consider a family earning $70,000 per year needing 20 years of income replacement — that's a $1.4 million coverage need. A $250,000 policy feels substantial until you run that math.

The difference in monthly premium between a $250,000 and a $1 million term policy is often smaller than families expect — but the protection gap is enormous.

Waiting Too Long to Buy

Premiums are set at the time of application, based on age and health. A healthy 30-year-old can lock in rates 50–60% lower than the same person at 45 — before a health diagnosis changes the picture entirely. Waiting has real consequences:

- Rates increase with every year of age, even in perfect health

- A new diagnosis (diabetes, heart disease, high blood pressure) can raise premiums significantly or trigger a denial

- Some conditions make certain policy types unavailable altogether

The families who get the best coverage at the lowest cost are almost always the ones who acted before they needed to.

How to Choose the Right Insurance Plan — and Advisor — for Your Family

When evaluating any life insurance policy, focus on five criteria:

- Coverage amount — Does it match your actual income replacement need?

- Premium affordability — Can you sustain this payment for the life of the policy?

- Insurer financial strength — Look for AM Best ratings of A- Excellent or above

- Flexibility — Can coverage be adjusted as life changes?

- Claims process — How straightforward is it to file and receive benefits?

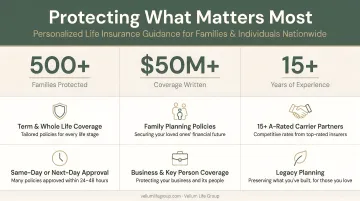

Working with an independent advisor — one who shops across multiple carriers rather than representing a single insurer — gives families access to competitive rates and unbiased comparisons. A captive agent is limited to one carrier's products; an independent advisor like Eva Ikonomakos at Vellum Life Group works with 15+ A-rated carriers to find the right fit for your family's situation, income, and goals.

With 15+ years of experience across financial services, healthcare, and international business, Eva built Vellum Life Group around that principle. Her carrier network includes Mutual of Omaha, Transamerica, Corebridge Financial, Aflac, and more than a dozen other top-rated insurers.

She has helped protect 500+ families across the country with $50M+ in coverage written — through a transparent, no-pressure process that includes a 24-hour response guarantee and ongoing annual reviews as life changes.

Many policies can be approved the same day or within a few days. To assess your current coverage gaps and explore options tailored to your family's situation, schedule a free, no-obligation consultation with Vellum Life Group at info@vellumlifegroup.com or call/text 917-363-3554.

Frequently Asked Questions

What insurance do I need to protect my family?

Life insurance is the foundation of family income protection. Most families need at least term life insurance to replace a breadwinner's income, and many benefit from layering in whole or universal life coverage as their financial picture grows. The right approach depends on family size, income, age, and whether group coverage is already in place.

What is the best life insurance policy type for my family?

Term life is the most affordable option for income replacement during peak earning years and is ideal for young families. Whole and universal life policies cost more but offer permanent coverage and build cash value over time. Most families start with term and revisit permanent coverage as their income and responsibilities grow.

How much life insurance does a family need?

The 10–12x annual salary rule is a useful starting point. For a more precise number, use the DIME method: add up your Debt, Income to replace, Mortgage balance, and projected Education costs for children. That total gives you a personalized coverage target.

What is the difference between term and whole life insurance?

Term life covers a set period (typically 10–30 years) at a lower cost, making it ideal for income replacement during a family's highest-need years. Whole life provides permanent coverage and builds cash value but comes at a higher premium. Most families start with term and revisit permanent options as their finances evolve.

Can a stay-at-home parent get life insurance?

Yes, and it's one of the most overlooked gaps in family coverage. Salary.com estimates the annual replacement value of a stay-at-home parent's contributions at around $178,201. A life insurance policy ensures the surviving spouse can cover childcare and household costs without draining savings.

What happens to coverage if a group plan changes or lapses?

Group plan coverage is not portable; it ends when the group plan does. Owning an individual policy independently ensures your family stays protected through plan changes, lapses, or transitions, with no gap in coverage.