Burial insurance with no waiting period does exist. Most people qualify for it, even with pre-existing conditions. But getting it requires understanding which type of policy you're actually buying — and that's exactly what this guide covers.

Here you'll find the difference between policy types, who qualifies for day-one coverage, what it costs, and how to read your policy to confirm you're actually protected from day one.

Key Takeaways

- Day-one coverage pays the full death benefit immediately — but requires answering health questions at application

- "No medical exam" and "no waiting period" are not the same thing — they describe two separate policy features

- Guaranteed issue policies always carry a mandatory 2-year waiting period — no exceptions, regardless of carrier

- Diabetes, high blood pressure, and COPD are common pre-existing conditions that can still qualify for immediate coverage

- The 2-year contestability clause is not a waiting period — it only applies if you misrepresented your health at application

What Is Burial Insurance With No Waiting Period?

Burial insurance — also called final expense or funeral insurance — is a small permanent whole life policy, typically ranging from $5,000 to $25,000 in coverage. It's designed specifically to cover end-of-life costs: funeral arrangements, cremation, outstanding medical bills, or any debts left behind. Premiums are fixed, the death benefit is guaranteed, and the policy doesn't expire as long as premiums are paid.

"No waiting period" means one thing: the full death benefit is payable from the very first day of coverage, for both natural and accidental causes of death. The only standard exclusion across virtually all carriers is suicide, typically within the first two policy years.

Waiting Period vs. Contestability Clause

These two terms get confused constantly, and the difference matters enormously.

Every life insurance policy includes a standard 2-year contestability period. During this window, the insurer can review medical records if a claim is filed — to verify that what you stated on the application was accurate. If you answered honestly, this clause has zero effect on your payout.

A waiting period is something different. Under a waiting period policy, if the policyholder dies from natural causes within the first two years, the insurer pays back only the premiums collected — sometimes with modest interest — rather than the full death benefit. A $15,000 policy where the insured dies in month eight might pay the family only $600 instead of $15,000.

Why Does the Waiting Period Exist?

Waiting periods exist because insurers need to manage risk when policies involve minimal or no medical underwriting. Without health questions, nothing stops someone with a terminal diagnosis from purchasing a policy and having their family file a claim within weeks.

As Western & Southern notes, simplified issue and guaranteed issue policies commonly include waiting periods of 1–3 years for exactly this reason. In practice, waiting periods serve three purposes:

- Protect insurers against applicants who are already terminally ill at the time of purchase

- Keep guaranteed issue premiums affordable for everyone else

- Make no-health-question policies financially viable to offer at all

The tradeoff: your family isn't fully protected from day one.

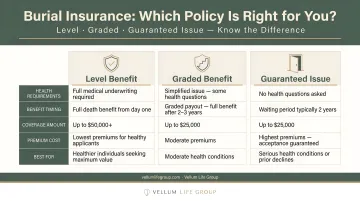

The Three Types of Burial Insurance Policies

The policy type determines everything: whether there's a waiting period, what it costs, and whether health questions are required. There are three distinct tiers.

Level Benefit (No Waiting Period)

Level benefit policies are simplified issue whole life products. You answer health questions, but the application process is straightforward:

- No medical exam, no blood draw, no physical

- Approval based on your health history alone

- Coverage is immediate — the full death benefit is in force from day one

For applicants who qualify, this tier delivers the most coverage per dollar — you're not paying the premium markup that comes with guaranteed issue. According to Mutual of Omaha's Living Promise product guide, their Level Benefit Plan pays 100% of the death benefit from day one for approved applicants ages 45–85, with face amounts from $2,000 to $40,000.

Graded/Modified Benefit (Partial Waiting Period)

Graded benefit policies are designed for applicants with more serious health histories who don't meet the standards for level coverage. You still answer health questions, but the death benefit phases in over time.

A typical graded structure looks like this:

| Policy Year | Natural Death Benefit |

|---|---|

| Year 1 | Premiums paid + 10% interest |

| Year 2 | Premiums paid + 10% interest |

| Year 3+ | 100% of face amount |

Foresters PlanRight Basic works exactly this way — accidental death pays 100% of the face amount from day one, but natural causes are limited during the first two years.

Guaranteed Issue (Full 2-Year Waiting Period)

Guaranteed issue policies ask no health questions and guarantee acceptance for applicants within the eligible age range (typically 50–85) — but every guaranteed issue policy carries a mandatory 2-year waiting period for natural causes of death, without exception.

Under Mutual of Omaha's guaranteed whole life product, for example, natural death in the first two years pays all premiums plus 10% — not the full benefit. Corebridge's guaranteed issue product pays 110%–120% of premiums paid for natural death in the first two policy years. That combination of higher premiums and delayed full coverage makes this the last resort — worth considering only when health conditions rule out every other option.

The critical myth to clear up: "No medical exam" does NOT mean "no waiting period." Foresters PlanRight, for instance, offers Preferred and Standard options with no exam and no waiting period. Mutual of Omaha also has no-exam policies — some with day-one coverage, some without. The exam and the waiting period are entirely separate features. Only policies with no health questions at all (guaranteed issue) always carry the 2-year wait.

Who Qualifies for Day-One Coverage?

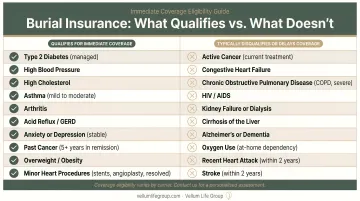

More people than most assume. The majority of burial insurance applicants can qualify for a level benefit policy — even with pre-existing conditions — as long as those conditions fall within a carrier's underwriting guidelines.

Conditions that commonly qualify for immediate coverage (depending on severity and carrier):

- High blood pressure and high cholesterol

- Type 1 and Type 2 diabetes, including some insulin users

- COPD and chronic bronchitis (varies by severity)

- Sleep apnea

- Anxiety and depression (mild to moderate)

- Asthma, arthritis, obesity

- AFib (depending on treatment and stability)

Conditions that typically result in a waiting period or decline:

- Active cancer treatment (some early-stage skin cancers may be excepted)

- Dementia or Alzheimer's disease

- Hospice care or terminal illness (typically defined as life expectancy of 12 months or less)

- Dialysis or chronic renal failure

- Current residence in a nursing home or skilled nursing facility

- Home health care for a chronic condition

Look-Back Windows Matter

Some conditions don't automatically trigger a waiting period. Instead, they come with time-based rules. A heart surgery that occurred more than 24 months ago may qualify for immediate coverage at one carrier, while the same surgery within the past 12 months might result in a graded benefit or decline at another.

These windows vary by carrier, which is exactly why shopping multiple insurers matters. What disqualifies you at one company may be acceptable at another. Eva Ikonomakos at Vellum Life Group runs applicant health profiles across 15+ A-rated carriers, including Mutual of Omaha, Foresters Financial, Americo, and American Amicable, specifically to match each client's health history to the carrier whose underwriting guidelines fit best.

What Does Burial Insurance With No Waiting Period Cost?

Several factors drive your monthly premium:

- Age — the single biggest factor; locking in a rate earlier saves money

- Gender — women typically pay less than men

- Tobacco use — smokers pay meaningfully more

- Coverage amount — face values typically range from $5,000 to $25,000

- Health history — affects whether you qualify for level benefit pricing

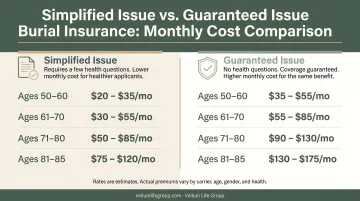

According to Aflac, the average cost of a $10,000 final expense policy is approximately $74 per month, though this figure varies widely by age, gender, health, and carrier.

That average also obscures a meaningful gap between policy types. A 2024 Policygenius analysis found that a 60-year-old male nonsmoker purchasing $25,000 in coverage paid roughly $104.60/month for simplified issue final expense versus $186.07/month for guaranteed issue — a difference of over $80 per month, with the guaranteed issue policy still requiring a two-year wait before paying the full death benefit.

Qualifying for level benefit coverage means paying less per dollar of coverage while your family is protected from day one — no waiting, no reduced payout, and no paying a premium for the privilege of both.

How to Verify If Your Policy Has a Waiting Period

Policy documents rarely include a sentence that plainly states "this policy has a two-year waiting period." The language is buried — but once you know where to look, you can find the answer in under a minute.

Locate the benefit schedule or death benefit table in your policy document. Look at what's listed for year one and year two:

- If both years show the full face amount (e.g., $15,000 from month one), you have no waiting period

- If years one and two show a lower dollar amount, a percentage, or language like "return of premiums plus 10% interest," you have a graded or full waiting period

- Common policy phrases to watch for: "Graded Benefit," "Limited Death Benefit," "first two policy years," "natural causes"

If you're unsure, ask your agent or insurer directly: "Does this policy pay the full death benefit from day one for natural causes of death?" That question should produce a clear yes or no.

One more clarification: even a no-waiting-period policy will contain a 2-year contestability provision. This is standard in every life insurance contract — it does not limit your payout, and honest applicants have nothing to fear from it.

How to Get Burial Insurance With No Waiting Period

The process is straightforward for most applicants:

- Answer health questions honestly — disclose all diagnoses and current medications. Misrepresentation is the one thing that gives an insurer grounds to contest a claim later

- Confirm beneficiary information is accurate — errors here cause unnecessary delays at claim time

- Submit the application — no exam required for simplified issue products; many are approved same day or within a few days

Choosing whether to work with an independent broker or go direct may matter more than which specific policy you select.

A captive agent or TV-marketed direct product is limited to one company's underwriting standards. If that company's guidelines don't accommodate your health profile, you either get declined or end up in a guaranteed issue product with a 2-year wait — often without realizing it.

An independent broker has access to multiple carriers and can match your health profile to the carrier most likely to approve you for level benefit coverage at the best rate. This service costs you nothing; brokers are compensated by the carrier.

The difference in outcomes can be significant:

- Captive agents offer one company's underwriting criteria — if you don't fit, you're declined or downgraded

- Independent brokers shop across carriers to find the one whose guidelines best accommodate your health history

- Level benefit coverage (immediate, full payout from day one) is far more attainable when your profile is matched to the right carrier

Vellum Life Group's founder Eva Ikonomakos works with 15+ A-rated carrier partners (including Mutual of Omaha, Foresters Financial, Americo, Transamerica, and others) and conducts a health profile review across multiple carriers before recommending a policy. Many clients who arrive assuming their health history disqualifies them from immediate coverage find they qualify for a level benefit policy once matched to the right carrier.

To find out where you stand, reach Eva at 917-363-3554 or info@vellumlifegroup.com for a free, no-obligation consultation.

Frequently Asked Questions

Is there a waiting period for final expense insurance?

Not always. Level benefit (simplified issue) policies offer day-one coverage for applicants who qualify by answering health questions. Only guaranteed issue policies — which require no health questions — always carry a mandatory 2-year waiting period.

What is the best insurance for final expenses?

A level benefit simplified issue policy typically offers the strongest combination: immediate coverage, lower premiums per dollar of benefit, and a death benefit sized for final expenses. An independent advisor who shops multiple A-rated carriers can match that to your specific health history and budget.

Does "no medical exam" mean there's no waiting period?

No. These describe two separate features. A policy can skip the physical exam while still requiring health questions — and those policies can offer full day-one coverage. Only "no health questions" policies (guaranteed issue) always have the 2-year wait.

What health conditions automatically require a waiting period?

Conditions that typically result in a 2-year waiting period regardless of carrier include: active cancer treatment, dementia or Alzheimer's disease, hospice care, dialysis, terminal illness, and current residence in a nursing home or skilled nursing facility.

What happens to my premiums if I die during a waiting period?

Under a guaranteed issue or graded benefit policy, natural-cause deaths during the waiting period trigger a refund of all premiums paid, sometimes with interest. Mutual of Omaha's guaranteed whole life, for example, returns premiums plus 10%. Accidental death is covered at the full benefit amount from day one, even under waiting period policies.