That gap is costly. According to LIMRA's 2025 Insurance Barometer data, roughly 100 million American adults believe they need more life insurance than they currently have. Part of the problem is confusion: 72% of Americans overestimate the cost of basic term coverage, which keeps people from acting. Choosing the wrong policy type compounds that problem — either by overpaying for features you don't need, or leaving your family underprotected during the years it matters most.

This article breaks down exactly how term and universal life work, compares them side by side, and gives you a practical framework for deciding which fits your situation.

Key Takeaways

- Term life covers a fixed period (10–30 years) at lower premiums — no cash value, maximum death benefit per dollar

- Universal life is permanent coverage that lasts a lifetime and builds tax-deferred cash value

- Term premiums are fixed; UL premiums are flexible but require active monitoring to avoid lapse

- Universal life costs more but delivers lifelong protection, cash value access, and adjustable coverage

- The right choice depends on your timeline, budget, and financial goals — there's no single right answer

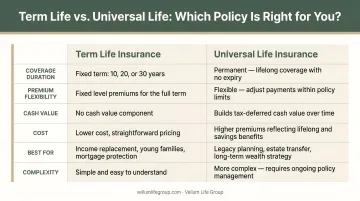

Term vs. Universal Life Insurance: At a Glance

Before going deeper, here's a direct comparison across the dimensions that matter most:

| Feature | Term Life | Universal Life |

|---|---|---|

| Coverage Duration | Fixed period: 10, 15, 20, or 30 years | Permanent — lasts a lifetime if properly funded |

| Premium Cost | Lower; locked in at purchase | Higher; flexible within policy limits |

| Premium Flexibility | Fixed; missing a payment can lapse the policy | Adjustable; cash value can sometimes cover gaps |

| Cash Value | None | Yes — grows tax-deferred; borrowable or withdrawable |

| Policy Complexity | Simple to manage | Requires active monitoring |

| Best Fit | Families, income replacement, temporary needs | Lifelong coverage, estate planning, cash value goals |

Cost

For a concrete sense of the premium difference: Guardian reports that a healthy 30-year-old can get a $500,000, 20-year term policy for roughly $30/month (male) or $23/month (female). Universal life premiums for an equivalent death benefit run higher — the exact amount varies widely based on age, health, funding pattern, and which UL type you choose. Getting a real quote is the only reliable way to compare.

Coverage Duration

Term expires. A 20-year policy bought at 35 ends at 55 — at which point renewing typically means much higher rates, or the coverage simply lapses. Universal life doesn't have that expiration problem, provided the policy is kept properly funded.

Cash Value and Premium Flexibility

Term premiums pay purely for the death benefit. With universal life, part of each payment funds the cost of insurance while the remainder accumulates as cash value. That cash value grows tax-deferred and can be accessed during your lifetime — but it also creates the policy's main vulnerability: if cash value falls too low, the policy can lapse.

What Is Term Life Insurance?

Term life is the most straightforward form of coverage available. If you die during the policy's fixed period, your beneficiaries receive the death benefit. If you outlive the term, coverage ends and no money is returned — unless you have a return-of-premium policy (a higher-cost variation that refunds premiums paid if no claim is made).

The NAIC defines term life as coverage purchased for a specific time period, with the death benefit paid only if the insured dies within that window.

How Premiums Work

Premiums lock in at purchase based on your age and health. The younger and healthier you are when you buy, the lower your rate for the entire term. This is why acting early matters — a 30-year-old pays significantly less than a 45-year-old for identical coverage.

Level term is the most common structure: both the premium and death benefit stay fixed throughout the term. Yearly renewable term (YRT) is less common — it renews annually, but premiums climb each year as you age.

Use Cases for Term Life

Term makes the most sense when your coverage need is tied to a specific time horizon:

- Young families with a mortgage and financially dependent children

- Working-age adults replacing income during the years their family depends on it most

- Individuals covering a specific loan or obligation with a defined payoff window

- Budget-conscious buyers who want maximum death benefit per premium dollar

LIMRA's 2025 data shows 47% of adults would have trouble covering basic living expenses within six months if a primary wage earner died unexpectedly. Term life is the most efficient tool for closing that gap affordably.

Many term policies include a conversion option that lets you switch to a permanent policy — like universal life — within a set window, without a new medical exam. This safety net matters if your health changes or your financial picture shifts before the term ends.

Conversion deadlines vary by policy and carrier, so confirm this detail before signing.

The core trade-off is straightforward: term delivers the highest death benefit per dollar, but if you outlive the policy, coverage ends with nothing paid out and no cash value accumulated.

What Is Universal Life Insurance?

Universal life insurance is a form of permanent coverage that combines a death benefit with a tax-deferred cash value account. Coverage can last your entire lifetime — as long as sufficient cash value or premium payments cover the policy's monthly internal charges.

The CFP Board describes permanent insurance like universal life as providing lifetime coverage alongside tax-advantaged savings that may be borrowed or withdrawn.

How the Premium Structure Works

Each premium payment splits into two pieces:

- Cost of insurance (COI) — covers the actual death benefit

- Cash value contribution — accumulates interest and grows tax-deferred

The COI charge increases as you age. If you reduce premiums too aggressively or credited interest rates drop, the policy can burn through its cash value faster than expected. The Wisconsin Office of the Commissioner of Insurance warns that underfunding can require higher premiums down the road — or trigger a lapse.

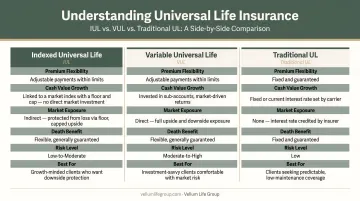

UL Subtypes

- Traditional UL — fixed credited interest rate; most predictable

- Indexed UL (IUL) — cash value tied to a market index like the S&P 500, with downside protection; the fastest-growing UL segment, with 2025 IUL new premium up 17% year-over-year

- Variable UL (VUL) — cash value invested in sub-accounts; higher potential return but also higher risk

Use Cases for Universal Life

UL is built for specific financial planning goals, not general coverage needs:

- Estate planning and wealth transfer — death benefits generally pass to beneficiaries income-tax free, per IRS guidance

- Lifelong coverage — for those who need protection regardless of age or health changes later in life

- Estate and legacy planning — funding a structured inheritance or wealth transfer; notably, studies consistently show that a large share of families with complex estates lack adequate planning in place

- Supplemental tax-deferred growth — for those who've maximized other tax-advantaged accounts

The cash value can be accessed through loans or withdrawals — useful for retirement income, emergencies, or other needs. But unpaid loans reduce the death benefit, and aggressive withdrawals can deplete cash value enough to lapse the policy. Annual check-ins matter here: interest rate changes and shifting premium payments can quietly shift a policy's long-term trajectory.

Term vs. Universal Life Insurance: Which Is Right for You?

No single policy type wins across every situation. The decision comes down to three questions:

- How long do you need coverage? A defined window (mortgage payoff, child-rearing years) points to term. Lifetime protection points to UL.

- What's your monthly budget? Term delivers far more death benefit per dollar if cost is a constraint.

- Do you have goals beyond the death benefit? Cash value access, estate planning, and legacy transfer are UL territory.

Choose Term Life If:

- You're raising children or carrying a mortgage

- You need income replacement during your working years

- Your life insurance need is temporary and tied to a specific obligation

- Budget is a primary factor

Choose Universal Life If:

- You want coverage that lasts your entire life regardless of future health changes

- You're interested in building tax-deferred cash value

- Your goals include estate planning, wealth transfer, or supplemental retirement income

- You're planning a structured wealth transfer or estate equalization

Consider Both

Some people benefit from layering a term policy with a smaller UL policy. The term provides maximum coverage during high-need years (raising kids, carrying debt), while the UL maintains permanent protection and cash value growth. The combined premium often fits a budget better than a single large UL policy would.

Whether layering makes sense depends on your finances, timeline, and goals — which vary significantly from one household to the next. Vellum Life Group, founded by Eva Ikonomakos with 15+ years of experience in financial services and legacy planning, works with 10+ A-rated carriers to compare options side by side. That carrier access matters: what one insurer offers for your age, health, and coverage amount can look very different from another's.

Conclusion

Term life and universal life are tools designed for different jobs. Term covers a specific window of risk at the lowest possible cost. Universal life provides permanent protection with flexibility and cash value for those with longer-horizon goals.

The right choice is the one that matches your timeline, budget, and what you're trying to protect — not whichever type sounds more sophisticated.

If you're weighing both options and want to see real numbers, Vellum Life Group offers a free, no-obligation consultation to help you compare them side by side across multiple A-rated carriers. Reach Eva Ikonomakos at 917-363-3554, info@vellumlifegroup.com, or book a 30-minute call at calendly.com/eva-ikonomakos/30min.

Frequently Asked Questions

What's the difference between permanent and universal life insurance?

"Permanent" is the broader category — it includes whole life, universal life, and other policies designed to last a lifetime. Universal life is one specific type of permanent insurance, distinguished by its flexible premiums and adjustable death benefit combined with a cash value component. Universal life is a subset of permanent insurance, not a synonym for it.

Why do people choose universal life insurance?

The main draws are lifelong coverage, tax-deferred cash value accumulation, premium flexibility, and estate planning utility. For those who've maxed out other tax-advantaged accounts, the cash value component offers an additional growth vehicle.

What happens to term life insurance at the end of the term?

Coverage ends. If you're still living, no death benefit is paid and no premiums are refunded — unless you have a return-of-premium policy. You can typically renew (usually at much higher rates), convert to a permanent policy before the conversion deadline, or let the policy lapse.

Can you convert term life insurance to universal life insurance?

Many term policies include a conversion privilege that lets you switch to a permanent policy — including universal life — within a set window, without a new medical exam. Conversion deadlines and available options vary by carrier, so check your specific policy terms before the window closes.

Is universal life insurance worth the higher cost?

For the right person, yes. If you need lifelong coverage, want cash value growth, or have estate planning objectives, the added cost can be well-justified. For someone who only needs temporary coverage or is working with a tighter budget, term typically delivers more value per dollar. The right answer depends entirely on your financial goals, not just the premium comparison.

Can you have both term and universal life insurance at the same time?

Yes — and it's a common strategy. Term provides high coverage during peak financial-responsibility years, while a smaller UL policy maintains permanent protection and builds cash value. The combined premium is often more manageable than funding a single large permanent policy, and the coverage structure matches different needs at different life stages.