This isn't a "one type wins" decision. It's a "which fits your life" decision. According to LIMRA's 2024 research, 102 million Americans say they need more life insurance coverage — and much of that gap comes down to confusion about which product actually fits.

This article breaks down both types clearly, compares them side-by-side, and gives you a practical framework to decide.

Key Takeaways

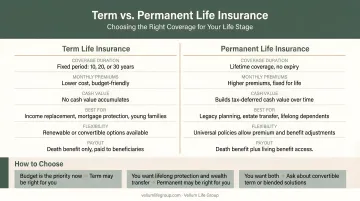

- Term life covers a set period (10–30 years) at a lower premium — the go-to choice for income replacement during peak earning years

- Permanent life covers you for life and builds cash value over time, at a higher premium and with more moving parts

- Your decision hinges on three things: how long you need coverage, what you can afford monthly, and whether cash value fits your goals

- The right choice depends on your age, budget, and long-term financial goals — not which type sounds more impressive

- Many families benefit from owning both types simultaneously

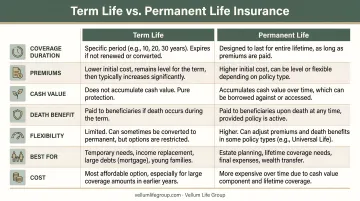

Term vs. Permanent Life Insurance: At a Glance

| Feature | Term Life | Permanent Life |

|---|---|---|

| Coverage Duration | Fixed period: 10, 20, or 30 years | Lifetime (as long as premiums are paid) |

| Premium Cost | Lower — especially at younger ages | Higher — reflects lifelong coverage + cash value |

| Cash Value | None | Grows over time on a tax-deferred basis |

| Death Benefit Guarantee | Only if death occurs during the term | Guaranteed eventually, as long as policy is active |

| Best For | Mortgages, income replacement, child-rearing years | Legacy planning, lifelong dependents, estate planning |

Permanent insurance includes several subtypes — whole life, universal life, and variable universal life — each with different structures. The details matter when you're comparing actual policies, so treat this as a starting point, not a final answer.

What Is Term Life Insurance?

Term life insurance is straightforward: pay premiums for a defined period, and your beneficiaries receive a death benefit if you pass away during that time. If the term ends while you're still alive, the policy expires with no payout and no cash value.

Coverage Structure

The most common term lengths are 10, 20, and 30 years, with level term being the most widely purchased type. With level term, both your premium and death benefit stay fixed for the entire period — so a $500,000 policy at 30 stays a $500,000 policy at 50.

Annually renewable term works differently: premiums start low and increase each year. It works for short-term coverage gaps but gets expensive quickly, so most families choose level term.

What Term Costs

Term life is the most affordable way to secure a large death benefit. A healthy 30-year-old can often get $500,000 in coverage for under $30 per month — a figure Vellum Life Group regularly sees when shopping policies across its carrier network.

That number surprises most people. LIMRA's 2025 research found that adults under 30 overestimate life insurance costs by 10 to 12 times, meaning many families who could easily afford term coverage simply assume it's out of reach.

The Conversion Option

Many term policies include a conversion provision — the ability to switch to permanent coverage within a specified window, often without a new medical exam. This matters more than most buyers realize. If your health changes during the term, conversion lets you lock in permanent coverage without going through underwriting again. It's worth asking about this feature when comparing policies.

When Term Makes Sense

Term is the right tool when your need has a clear end date:

- Covering a mortgage that will be paid off in 20–30 years

- Replacing income during the years your children depend on you

- Protecting a shared financial obligation for a defined period

- Getting maximum coverage when budget is the primary constraint

One tradeoff worth knowing: when the term ends, coverage stops. Renewal is available on most policies, but premiums increase significantly because you're older. There's no residual value — you simply walk away with nothing if you outlive the term.

What Is Permanent Life Insurance?

Permanent life insurance is designed to last your entire life, combining a death benefit with a cash value component that grows over time. As long as premiums are maintained, the policy stays active — and a death benefit will eventually be paid.

The Cash Value Feature

This is where permanent insurance differs most from term. A portion of each premium goes into a cash value account that grows on a tax-deferred basis. Over time, you can:

- Borrow against the cash value

- Make partial withdrawals

- Use it to pay future premiums in some policies

One important caveat: loans and withdrawals reduce the death benefit unless repaid. The IRS confirms that death benefit proceeds are generally excluded from a beneficiary's gross income, though interest earned is taxable. Consult a qualified tax advisor before making any tax-related decisions.

How cash value accumulates — and how much control you have over it — depends on which type of permanent policy you choose.

The Three Main Types

| Type | Key Characteristics |

|---|---|

| Whole Life | Fixed premiums, guaranteed cash value growth, potential dividends |

| Universal Life | Flexible premiums, adjustable death benefit, adapts to changing needs |

| Variable Universal Life | Market-linked cash value growth — higher potential, higher risk |

Most people comparing permanent to term will find whole life or universal life the most relevant options. Variable universal life introduces investment risk that's rarely the right fit when protection — not portfolio growth — is the primary goal.

Why Permanent Costs More

The higher premium isn't just "more expensive term." Permanent insurance is a fundamentally different product. You're paying for:

- A death benefit that will certainly be paid at some point

- Cash value that accumulates over decades

- Lifelong coverage regardless of how long you live

For clients with lifelong financial obligations — a dependent who will always need care, or an estate that needs to transfer efficiently — that higher premium buys something term simply can't: certainty.

When Permanent Makes Sense

Permanent coverage fits specific situations where the need doesn't have a clear end date:

- Supporting a dependent with a disability who will need care indefinitely

- Estate planning and transferring wealth to the next generation

- Business succession or buy-sell agreements where the obligation may last beyond a typical term window

- Building wealth with tax-deferred growth as part of a broader financial plan

Term vs. Permanent: Which Is Right for You?

The decision comes down to three questions: How long do you need coverage? What's your budget? Do you want the policy to serve as a financial tool beyond basic protection?

A Practical Decision Framework

Choose term if:

- Your primary need is income replacement during working years

- You have a mortgage, young children, or other time-bound obligations

- Budget is a real constraint and you want maximum coverage per dollar

- You prefer to invest separately rather than through a policy

Choose permanent if:

- You want guaranteed coverage that won't expire

- You have a lifelong dependent or ongoing legacy planning needs

- You're planning for estate planning, legacy transfer, or succession needs

- You're looking to build cash value in a tax-advantaged structure over time

The "Why Not Both?" Approach

Many families don't have to choose one or the other. Layering a term policy on top of a permanent policy is a widely used strategy. The term policy handles the heavy lifting during peak-need years (mortgage, kids at home, income replacement), while the permanent policy provides a lifelong foundation with cash value building underneath.

For example, a 35-year-old with young children and a 25-year mortgage might carry a $500,000 30-year term policy plus a smaller whole life policy. The term covers the years of highest financial exposure. The whole life policy stays active after the mortgage is paid and the kids are grown, continuing to build cash value and providing a permanent death benefit.

Working with an independent advisor makes this kind of side-by-side comparison practical. Vellum Life Group partners with 10+ A-rated carriers, so clients can compare term and permanent options across multiple insurers in one conversation. The result is a recommendation built around your specific situation, not a single carrier's product lineup.

Frequently Asked Questions

What is better, term life insurance or permanent?

Neither is universally better. Term is more affordable and works well for time-bound needs like income replacement and mortgage coverage. Permanent is the right choice when you need lifelong coverage or want a policy that builds cash value. The best policy depends on your budget, age, and what you need the coverage to accomplish.

Can I get life insurance if I have cirrhosis?

Eligibility depends on the severity, stage, and your overall health profile. Some carriers decline coverage outright; others offer modified or graded benefit policies. An independent advisor with access to multiple carriers — including those that specialize in higher-risk applicants — gives you the best shot at finding a fit.

Can I convert term life insurance to permanent?

Many term policies include a conversion option that lets you switch to permanent coverage within a set window, often without a new medical exam. It's worth asking about this feature when you shop — especially if your health might change before the term ends.

What happens when term life insurance expires?

Coverage ends, with no payout. If the policy includes a renewal provision, you can continue coverage — but premiums will be significantly higher based on your current age. If you have a conversion option and haven't used it, that window may also close. Without action, you're left without coverage.

Can I have both term and permanent life insurance at the same time?

Yes, and it's a common strategy. Term covers peak-need years affordably while a permanent policy builds lifelong protection and cash value. Many families find this combination addresses both short-term risk and long-term goals without overpaying during their highest-cost years.

How do I know how much life insurance coverage I need?

Start with your income replacement needs, outstanding debts, number of dependents, and long-term goals like college funding or legacy planning. A licensed advisor's needs analysis will give you a more reliable number than any online rule-of-thumb.

The right policy matches your life stage, your budget, and the people who depend on you. Term offers focused, affordable protection for the years you need it most. Permanent offers something a term policy never can: coverage that doesn't run out.

If you're not sure where you fall, a free consultation with Vellum Life Group is a good next step. Eva Ikonomakos works with clients across 14+ states and compares options across 10+ A-rated carriers, and approaches every conversation without pressure or jargon. Reach out at info@vellumlifegroup.com or call 917-363-3554 to get started.