The reality is that most smokers in reasonable health can qualify for term life insurance from major carriers. Yes, premiums are higher. But coverage is available, and with the right approach, it's more affordable than many people expect.

This guide covers everything you need to know: why rates are higher, what counts as "smoking" under underwriting rules, what to expect in terms of actual dollar costs, and how to get your most competitive quote.

Key Takeaways

- Smokers can qualify for term life insurance — denial is rare for otherwise healthy applicants

- Most insurers classify anyone who has used tobacco or nicotine products in the past 12 months as a smoker, including vaping

- Smokers pay an average of 286% more than non-smokers for the same coverage

- Comparing multiple carriers is essential, since smoker rates vary widely from one insurer to the next

- Quitting and staying tobacco-free for 12+ months can qualify you for a rate reclassification

Can Smokers Get Term Life Insurance?

Yes — smoking alone will not get you denied. The vast majority of smokers in otherwise reasonable health can secure term life coverage from most major carriers.

What smoking does affect is your rate class, which directly determines your premium. Smokers are placed in a smoker classification rather than standard or preferred non-smoker tiers, and that classification carries higher premiums. But coverage itself is accessible.

The one meaningful exception: smokers with severe related health conditions may face limited options or outright denial. This includes conditions such as:

- Advanced COPD or chronic respiratory disease

- Recent lung cancer diagnosis or active treatment

- Other serious smoking-related complications

That's a health underwriting issue, not a blanket exclusion of smokers.

Why Do Smokers Pay More for Term Life Insurance?

The Underwriting Logic

Life insurers price risk. A term policy is a bet on whether the insurer will pay out a death benefit during the policy term — and smokers statistically represent a measurably higher risk. According to CDC data, overall mortality among U.S. smokers is roughly three times higher than among people who never smoked, and life expectancy for smokers is at least 10 years shorter. Insurers price those odds accordingly.

The Health Classification System

Most carriers assign smokers to one of two tiers:

- Preferred Smoker — tobacco use is the primary risk factor; other health markers are in good range

- Standard Smoker — tobacco use plus additional concerns such as elevated blood pressure, weight, or cholesterol

The distinction matters because it directly affects what you pay. Controlling other health metrics — keeping blood pressure in range, maintaining a healthy weight, managing cholesterol — can move you from Standard to Preferred, which translates to real premium savings. Sample data from U.S. News shows the difference between Preferred and Standard Smoker tiers running roughly $51 to $66 per month on a $1 million, 20-year term policy for a 35-year-old.

Two More Factors That Shape Your Rate

Beyond your health tier, a few other variables influence what you'll pay:

- Policy term length — the longer the term, the more cumulative risk the insurer prices in; a 10-year policy carries a smaller smoker surcharge than a 30-year one

- Accurate application disclosures — misrepresenting your smoking status is insurance fraud; insurers test for nicotine and cotinine during medical exams, and a misrepresentation discovered at claim time can result in a denied death benefit, leaving your beneficiaries unprotected

- Overall health profile — conditions like diabetes, heart disease, or a family history of cancer compound tobacco risk and can push you deeper into Standard territory

What Counts as "Smoking" for Life Insurance Purposes?

Most carriers cast a wide net. Products that typically trigger a smoker classification include:

- Cigarettes

- Cigars and pipes

- Hookahs

- Chewing tobacco and snuff

- E-cigarettes and vaping devices

- Nicotine patches and nicotine gum (at many carriers, since they contain detectable nicotine)

That list covers the straightforward cases. The more interesting question is what happens when your situation doesn't fit neatly into "cigarette smoker" or "non-smoker."

Where It Gets Nuanced

Not every carrier treats every product identically. A few examples from actual underwriting guides:

- Occasional cigars: Mutual of Omaha's fully underwritten guide allows up to 24 cigars per year at non-tobacco rates if urinalysis comes back negative — but their simplified-issue guide does not offer the same allowance

- Non-cigarette products (Prudential): Prudential's Non-Smoker Plus tier may allow cigars, pipes, chewing tobacco, and nicotine replacement products if there's been no cigarette or vaping use in the past 12 months

- Marijuana: Classification varies significantly. Mutual of Omaha's simplified-issue guide allows marijuana use at non-tobacco rates; Corebridge's guide permits best-class consideration for 8 or fewer days of use per month, while heavier use bumps to Standard Tobacco at best

If you're an occasional or non-cigarette tobacco user, carrier selection matters enormously. The same applicant can qualify for non-smoker rates at one carrier and pay full smoker rates at another — which is exactly why comparing multiple carriers before you apply is worth the extra step.

Term Life Insurance Rates for Smokers: What to Expect

Smoker vs. Non-Smoker Rate Comparison

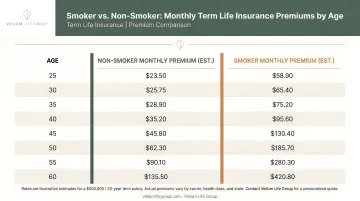

The table below shows estimated monthly premiums for a $500,000, 20-year term policy, based on 2024 Policygenius sample data. These are illustrative figures — individual rates vary by carrier, health class, and state.

| Age | Female Smoker | Female Non-Smoker | Male Smoker | Male Non-Smoker |

|---|---|---|---|---|

| 20 | $60.59 | $22.65 | $76.43 | $30.20 |

| 30 | $65.75 | $22.98 | $80.95 | $29.32 |

| 40 | $113.40 | $35.27 | $145.39 | $42.94 |

| 50 | $257.05 | $78.29 | $351.50 | $102.50 |

How Age Amplifies the Gap

The rate difference between smokers and non-smokers grows sharply with age. A 30-year-old male smoker pays roughly $51 more per month than a non-smoking peer. By age 50, that gap widens to $249 per month — nearly $3,000 per year. The same pattern holds for women: the monthly gap jumps from about $43 at age 30 to $179 at age 50.

Those numbers make the choice of term length — and when you buy — more consequential for smokers than for almost any other applicant group.

How Term Length Affects Cost

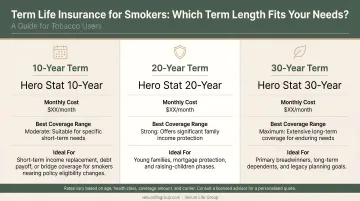

For a 40-year-old smoker, NerdWallet's 2026 sample data shows the annual cost difference across term lengths:

| Term Length | Male Smoker (Annual) | Female Smoker (Annual) |

|---|---|---|

| 10-year | $895 | $720 |

| 20-year | $1,464 | $1,157 |

| 30-year | $2,475 | $1,750 |

Each term length serves a different situation:

- 10-year: The most affordable entry point — useful if your budget is tight or your coverage needs are short-term

- 20-year: Balances cost with meaningful protection across the years your dependents need it most

- 30-year: Best for younger smokers with a mortgage or long-term dependents who want to lock in rates before age drives costs higher

Using Coverage Amount as a Lever

Smokers working with a tighter budget can reduce the face amount — $250,000 instead of $500,000 — to keep premiums manageable. Just weigh that decision against your actual income replacement needs, existing debt, and what your family would genuinely need.

How to Get the Best Term Life Insurance Quotes as a Smoker

Compare Multiple Carriers — Rates Vary More Than You'd Expect

The single most effective thing a smoker can do is shop across carriers simultaneously. Underwriting guidelines for tobacco users differ substantially from company to company. U.S. News sample data shows that a 35-year-old male at Preferred Smoker rates can see monthly premiums range from $167.57 at Pacific Life to over $197 at MassMutual for the same $1 million, 20-year policy. That's roughly a $350 annual difference for identical coverage.

Carrier variance is even more pronounced when you factor in age, health class, and product type. The cheapest carrier for a 35-year-old male smoker may not be the best option for a 50-year-old female smoker.

Improve Your Rate Class Before Applying

You may not be able to change your smoking history, but you can control other factors that determine whether you land in Preferred Smoker vs. Standard Smoker:

- Maintain a healthy weight and BMI

- Keep blood pressure in a normal range

- Manage cholesterol levels

- Address any other treatable health conditions before applying

Moving from Standard to Preferred Smoker can save $50–$66 per month — over $600 annually — without quitting.

Buy Now, Not Later

Every year you wait, premiums increase with age regardless of smoking status. Locking in coverage today at current rates is almost always cheaper than waiting, even if you plan to quit soon. If you do quit, you can apply for a rate reclassification later. A one-year delay at age 40 can add $10–$20 per month to your premium — permanently.

The No-Exam Option

If locking in coverage quickly is the priority, some carriers offer simplified-issue or accelerated underwriting term policies that skip the traditional medical exam. These are faster and more convenient — particularly for applicants with complex health histories beyond smoking. The tradeoff: no-exam policies typically cost more than fully underwritten policies, and tobacco use must still be honestly disclosed.

Working With an Independent Advisor

Direct applicants are locked into whatever rate that one carrier offers. Working with an independent advisor who has access to multiple A-rated carriers means your profile gets compared across the market.

Vellum Life Group works with 15+ carriers — including Mutual of Omaha, Transamerica, Corebridge Financial, and Foresters Financial — and takes a no-pressure, no-jargon approach to finding the right fit. For smokers specifically, that market access is where the $350+ annual savings gap gets closed. Free consultations are available at info@vellumlifegroup.com or by calling 917-363-3554.

How Quitting Smoking Can Lower Your Premiums

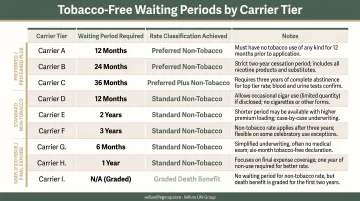

The 12-Month Rule

Most insurers require applicants to be completely tobacco-free for at least 12 consecutive months before reclassifying them from smoker to non-smoker rates. Some carriers set the bar higher:

- Mutual of Omaha Preferred: 24 months tobacco-free

- Mutual of Omaha Preferred Plus: 36 months tobacco-free

- Corebridge Preferred Plus Non-Tobacco: 5 years tobacco-free

- Prudential Preferred Best: 5 years tobacco-free

These are examples — not a complete list. Requirements vary by carrier and rate class, so it pays to shop across multiple insurers. The baseline 12-month threshold gets you access to standard non-smoker rates. Hitting the longer windows unlocks the best available rate classes, which is where the real savings show up.

What Reclassification Is Worth

Using the same Policygenius sample data from the rate table above, a 30-year-old female who quits and reclassifies on a $500,000, 20-year term drops from $65.75 to $22.98 per month — a savings of roughly $43/month or $516/year. For a 30-year-old male, the savings run about $52/month or $621/year.

Stretched over a 20-year policy, that's $10,000–$12,000 back in your pocket.

How the Re-Rating Process Works

After reaching the required tobacco-free period, you have two options:

- Request a rate reconsideration from your current insurer — this typically requires a new medical exam to confirm cessation via cotinine testing

- Apply for a new policy with a different carrier at non-smoker rates

If your health has also improved since you first applied — weight loss, resolved conditions, better blood pressure — a new policy with a different carrier often beats a rate review, particularly for anyone originally rated at Standard Smoker.

Vellum Life Group provides ongoing support to existing clients through annual reviews and life change check-ins, which includes helping policyholders navigate the reclassification process after quitting.

Frequently Asked Questions

Can you get term life insurance as a smoker?

Yes. Most major carriers offer term life insurance to smokers, and denial is uncommon for otherwise healthy applicants. You'll be placed in a smoker rate class and pay higher premiums, but coverage is available.

Do life insurance companies charge more for smokers?

They do. Smokers typically pay roughly 2–3 times more than non-smokers for the same policy. The exact multiple depends on age, health class, carrier, and term length, with older applicants generally facing a wider gap.

What tobacco products count as "smoking" for life insurance?

Most carriers include cigarettes, cigars, pipes, hookahs, chewing tobacco, snuff, e-cigarettes, vaping devices, and nicotine replacement products like patches and gum. Treatment of occasional cigar use and marijuana varies by carrier — some offer more favorable classifications than others.

How do life insurance companies test for nicotine?

Most policies include a medical exam with blood and urine samples that test for cotinine, a nicotine metabolite detectable for at least 24–72 hours after last use. Misrepresenting your tobacco use on an application puts your policy and your family's death benefit at risk.

How long do you have to quit smoking to get non-smoker rates?

Most insurers require 12 consecutive months tobacco-free before reclassifying a policyholder, though some carriers require 24 months for standard non-smoker status and up to 5 years for preferred tiers. A new medical exam is typically required to confirm cessation.

What happens if I start smoking after buying a term life policy?

Your existing premium is locked in — starting smoking after your policy is issued doesn't change your current rate. If you apply for a new policy or increase coverage, however, you'd be rated as a smoker at that point.