Qualifying life events (QLEs) are the specific circumstances that allow you to adjust health insurance coverage outside the standard open enrollment window. Miss the deadline, and you may face months without coverage or stuck in a plan built for a life you no longer have.

This article covers what counts as a QLE, how long you have to act, what happens if you miss the window, and why these same events should prompt a life insurance review too.

Key Takeaways

- QLEs (job loss, marriage, a new child, moving) let you enroll in or change health coverage outside of open enrollment

- ACA Marketplace plans generally give you 60 days from the event; many group plans allow only 30 days

- Missing the Special Enrollment Period (SEP) window typically locks you out until the next open enrollment cycle

- Life insurance isn't subject to ACA SEP rules, but the same life events signal a critical need to review your coverage

- Have your documentation ready before contacting your insurer; delays can cost you your enrollment window

What Is a Qualifying Life Event?

HealthCare.gov defines a qualifying life event as a change in your situation — getting married, having a baby, losing health coverage — that makes you eligible for a Special Enrollment Period (SEP). Outside of open enrollment, a QLE is the only mechanism that allows you to enroll in a new plan or make changes to an existing one.

The word "qualifying" matters. Not every life change opens an enrollment window. The IRS, Department of Labor, and ACA each define specific triggering events for different coverage systems. An inconvenient change in your schedule doesn't qualify. A move to a new state does.

How the SEP mechanism works:

- A recognized QLE triggers a limited enrollment window

- Within that window, you can enroll in a new plan, add or remove dependents, or switch coverage

- Outside the window — or without a QLE at all — most changes are not permitted

Coverage type matters here, too. ACA Marketplace SEPs are governed by federal regulations under 45 CFR 155.420, with defined timelines and documentation requirements. Group-sponsored health plans follow separate HIPAA rules under 29 CFR 2590.701-6. Life insurance operates entirely outside these ACA frameworks — but that makes life events more relevant to it, not less. Each major life change is one of the clearest indicators that your life insurance coverage needs a fresh look.

Types of Qualifying Life Events and What They Mean for Your Coverage

HealthCare.gov groups QLEs into four main categories. The rules and documentation requirements vary slightly depending on whether you have Marketplace, group-sponsored, or individual coverage.

Loss of Health Coverage

Losing coverage is one of the most common QLEs. Triggering situations include:

- Job loss or reduction in hours

- Aging off a parent's plan at 26

- Losing Medicaid or CHIP eligibility

- End of student or school-based coverage

You generally have 30–60 days to enroll in replacement coverage. COBRA is available as a continuation option, but the cost is significant. Per CMS rules, beneficiaries can pay up to 102% of the plan cost, and standard job-loss coverage lasts up to 18 months. You keep your existing plan — at full premium.

Changes in Household

Marriage, divorce, having or adopting a child, and the death of a covered family member all qualify. Each event changes who needs to be on a plan and what dependent or beneficiary adjustments are required.

These changes also carry financial weight beyond health coverage. When you marry, your household income picture shifts. When a child arrives, 18+ years of financial dependency begin. A 2024 LIMRA report found that 42% of American adults — roughly 102 million people — say they need more life insurance than they currently have. These are the exact moments when that gap becomes most costly to ignore.

An advisor like Vellum Life Group can help you review your life insurance at these transitions to make sure your coverage reflects your actual family structure.

Changes in Residence

Moving to a new ZIP code, county, or state qualifies as a QLE, but only if the move takes you outside your current plan's service area. Relocating within the same service area generally does not trigger an SEP.

Common documentation required for a move-based SEP:

- New lease or mortgage documents

- USPS address change confirmation

- Utility bill showing new address

Note that moving solely for medical treatment or vacation does not qualify under Marketplace rules.

Other Qualifying Events

Several less common events also create SEPs:

- Gaining U.S. citizenship or lawful immigration status

- Release from incarceration (60-day Marketplace SEP)

- Income changes that affect subsidy eligibility

- Turning 65 (which triggers Medicare enrollment, not an ACA SEP)

- Losing or gaining AmeriCorps or VISTA service coverage

Some states have expanded their own QLE definitions. California and New York, for instance, have additional rules and longer windows in certain situations. Check your state exchange if standard federal rules don't appear to cover your circumstance.

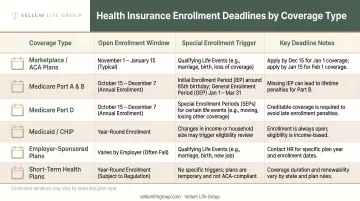

How Long Do You Have to Act After a Qualifying Life Event?

Deadlines vary by coverage type, and missing yours can mean waiting until Open Enrollment to make changes.

| Coverage Type | Standard Window | Key Notes |

|---|---|---|

| ACA Marketplace | 60 days from event | Per 45 CFR 155.420 |

| Employer group health plan | 30 days in many cases | HIPAA rules; 60 days for Medicaid/CHIP events |

| COBRA election | 60 days from coverage loss or election notice | Not a Marketplace SEP |

| Medicaid / CHIP | Year-round | Not tied to Open Enrollment |

One important caveat: if you know a qualifying event is coming — say, a job end date is confirmed or a coverage loss is expected — HealthCare.gov allows you to apply up to 60 days before the expected loss of coverage. Acting early eliminates any gap in coverage between your old plan ending and your new one beginning.

Documentation You'll Need

Most insurers require proof before activating an SEP. Gather these before initiating any changes:

- Marriage certificate (for marriage-based SEPs)

- Birth certificate or adoption documentation (for new dependents)

- Termination letter or coverage end notice from your plan administrator (for coverage loss)

- Lease, mortgage documents, or USPS address confirmation (for relocations)

- Divorce decree or legal separation documentation (for divorce-based SEPs)

HealthCare.gov requires submitted documents to arrive within 30 days of selecting a plan. Given how tight the overall SEP window already is, tracking down paperwork after choosing a plan creates real risk. Have everything gathered before you start the enrollment process.

What Happens If You Miss the QLE Window?

Missing the SEP deadline closes the door. Outside of open enrollment, you can only enroll in or change Marketplace coverage if you qualify for an SEP. Without one, you're generally locked out until the next Open Enrollment Period, which runs November 1 to January 15 each year. That's a potential gap of up to 9.5 months.

The consequences are real. KFF reports that 26.7 million people ages 0–64 were uninsured in 2024, with nearly 70% having been uninsured for more than a year — and 59% saying they likely couldn't cover a $2,000 unexpected medical expense.

If you've missed your window, limited options remain:

- Short-term health insurance: Available as a stopgap, but federally capped at a 3-month initial term and 4-month total duration under 2024 CMS rules. These plans often exclude pre-existing conditions and don't meet ACA standards.

- Medicaid and CHIP: Year-round enrollment if you meet income eligibility — not restricted by Open Enrollment or SEP windows.

- State-specific rules: Some state exchanges offer expanded timelines. Covered California, for instance, includes a 90-day SEP for loss of Medi-Cal coverage.

Life insurance carries a parallel risk. A family that has grown, taken on a mortgage, or shifted to a single income may still be carrying a policy written for entirely different circumstances. A $250,000 term policy that made sense before a second child and a $400,000 home purchase may leave a significant coverage gap — one that only becomes visible when it's too late to fix.

Steps to Take When You Experience a Qualifying Life Event

Act on Day One

The SEP clock starts on the date of the qualifying event — not the day you get around to reviewing your options. Identify the exact event date, calculate your deadline, and put it on your calendar before anything else.

Notify the Right Party

- Marketplace coverage: Log in to HealthCare.gov or your state exchange

- Group-sponsored plan: Contact your plan administrator or benefits administrator directly

- Individual plan: Call your insurer

Each route has different documentation requirements. Don't assume the process is the same across all three.

Gather Documentation Before You Start

Have your proof ready before initiating the change:

- Job loss → coverage termination letter with end date

- Marriage → certified marriage certificate

- New child → birth certificate or adoption documentation

- Move → lease, deed, or USPS address confirmation

Review Life Insurance at the Same Time

A QLE is the right moment to look beyond health coverage. Each major event reshapes your financial exposure in a specific way:

- Marriage creates new shared financial obligations immediately

- A new child adds up to two decades of dependency

- A new mortgage puts significant household debt on the line

ACLI research shows roughly 1 in 4 adults say their household would feel the financial impact of a primary wage earner's death within one month. A health insurance SEP and a life insurance review address two sides of the same problem.

Vellum Life Group works with individuals and families going through these exact life changes. A free consultation with founder Eva Ikonomakos starts with understanding your updated life situation — new dependents, new debts, new income obligations — before recommending any coverage. For qualifying applicants, many policies can be approved the same day or within a few days.

Don't Assume Auto-Updates

Most plan changes require affirmative action from you within the SEP window. Your plan administrator will not automatically update your dependents. Your insurer will not automatically adjust your coverage. The responsibility to act sits with the policyholder.

Conclusion

Qualifying life events exist as a built-in safety valve in the enrollment system — a recognition that life changes don't observe calendar schedules. But the window is short, and missing it means waiting another year.

The events that trigger a special enrollment period — a marriage, a new child, a job loss, a move — are the same events that shift what your family depends on financially. Each one is also a natural moment to ask whether your life insurance still fits your situation. Coverage that made sense before a baby arrived or before a spouse left the workforce may not be sufficient now.

If a qualifying life event is prompting you to revisit your coverage, it's worth looking at both pieces together — not because they're the same product, but because the underlying need is the same: protecting your family from what they can't predict.

Frequently Asked Questions

What life-changing events allow you to change your insurance?

There are four main categories:

- Loss of existing coverage — job loss, turning 26, losing Medicaid

- Household changes — marriage, divorce, birth, adoption, or death of a covered member

- Change in residence — moving to a ZIP code, county, or state outside your plan's service area

- Other events — income changes affecting subsidy eligibility, or gaining lawful immigration status

How long do I have to change my insurance after a qualifying life event?

For ACA Marketplace plans, the standard window is 60 days from the date of the qualifying event. Many group-sponsored plans allow only 30 days, so check your plan documents or benefits administrator immediately. Acting early is better than waiting — the deadline is fixed, and extensions are rarely granted.

What documents do I need to prove a qualifying life event?

It depends on the event: a marriage certificate for marriage, a birth certificate for a new child, a coverage termination letter for job loss, or a lease or mortgage document for a move. Confirm the specific requirements with your insurer or marketplace before submitting, as missing documentation can delay or void your enrollment.

Does a qualifying life event also affect life insurance?

Life insurance is not subject to ACA SEP rules or enrollment deadlines. However, events like marriage, the birth of a child, or buying a home significantly change your financial obligations — making them strong triggers to review whether your current coverage is still adequate for your family's needs.

What happens if I miss the special enrollment period after a qualifying life event?

Missing the SEP window typically means waiting until the next open enrollment period (November 1–January 15 for Marketplace plans). Short-term insurance may be available as a temporary bridge, and Medicaid or CHIP have year-round enrollment if you meet income eligibility requirements.

Can moving to a new state qualify as a life event for changing insurance?

Moving to a new ZIP code, county, or state that takes you outside your current plan's service area typically qualifies as a QLE and triggers an SEP. You'll generally need to provide proof of the move, such as a lease, deed, or USPS address change confirmation, before the SEP can be activated.