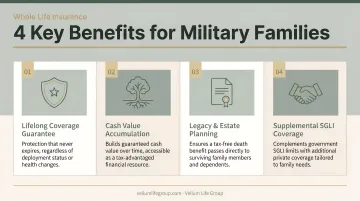

Whole life insurance solves problems that government programs simply don't. It doesn't expire, doesn't require re-underwriting when your health changes, and builds cash value over time — features that matter enormously for families managing deployment risk, frequent relocations, and long-term financial obligations.

This guide compares the best whole life insurance options for military families in 2026, what sets each carrier apart, and how to evaluate your options before a health event or age increase changes what's available to you.

Key Takeaways

- Whole life insurance is permanent: premiums lock in at issue age and coverage doesn't expire due to health changes.

- SGLI ends at separation; VGLI premiums escalate sharply with age, making private whole life a more sustainable long-term option.

- USAA and AAFMAA offer the strongest military-specific features, including no war exclusion clauses.

- Veterans with service-connected conditions should prioritize carriers with flexible underwriting — Guardian is one example worth evaluating.

- Always verify war clause language before purchasing any private policy.

Why Military Families Need Whole Life Insurance

SGLI provides up to $500,000 in coverage during active duty — a solid starting point, but one with real limitations. It carries no cash value, no portability, and it ends when you leave the service. If your health has declined due to a service-connected condition, applying for private coverage post-separation can mean higher premiums or outright denial.

Whole life insurance addresses each of these gaps directly:

- No expiration — coverage stays in force regardless of age or health changes after issue

- Locked premiums — the rate you're quoted at 28 stays the same at 55

- Cash value growth — tax-deferred savings you can borrow against for emergencies, education, or retirement income

- Portability — follows you through every PCS move and career transition

These benefits matter most when secured early. According to the VA's 2024 Annual Benefits Report, nearly 6 million veterans were receiving service-connected compensation. That's 6 million people whose health histories now complicate private insurance applications. Locking in whole life coverage before separation — or before a diagnosis — is what keeps those options open.

Best Whole Life Insurance for Military Families in 2026

Each carrier below was evaluated on financial strength (AM Best rating), military-specific policy features, cash value growth potential, war/combat clause language, and coverage flexibility for servicemembers and veterans.

USAA

USAA serves exclusively military members, veterans, and their families. Its Secure Whole Life product is built with military circumstances in mind, and the policy details reflect that focus directly.

| Factor | Details |

|---|---|

| AM Best Rating | A++ (Superior), affirmed July 2025 |

| War/Combat Coverage | No war exclusion clause on whole life policies |

| Military-Specific Benefit | Up to $25,000 severe injury benefit on eligible policies |

| Coverage Adjustments | Option to increase coverage after qualifying life events without a medical exam |

Best for: Active-duty servicemembers and veterans who want a carrier built entirely around military life, with no war exclusion and built-in deployment protections.

Note: USAA's universal life products are issued through John Hancock — confirm product type before applying.

MassMutual

For military families planning coverage that needs to last decades, MassMutual's dividend track record is hard to ignore. It has paid dividends to eligible participating policyholders every year since 1869 — a 155-year uninterrupted run from a mutual company with no obligation to outside shareholders.

| Factor | Details |

|---|---|

| AM Best Rating | A++ (Superior), affirmed September 2024 |

| Cash Value | Guaranteed growth; participating policies eligible for annual dividends (not guaranteed) |

| Dividend History | Uninterrupted since 1869 |

| Best For | Long-term financial planning, estate building, families with lifelong dependents |

Best for: Military families focused on long-term wealth accumulation alongside permanent protection. Confirm current guaranteed cash value growth rates and Whole Life 100 product details directly with MassMutual before applying.

New York Life

New York Life is one of the largest mutual life insurers in the country, and its Custom Whole Life product offers something particularly useful for veterans on fixed incomes: early pay-off options. You can structure the policy to be fully paid up in 10 or 20 years while keeping lifetime coverage — a meaningful advantage if your income shifts post-service.

| Factor | Details |

|---|---|

| AM Best Rating | A++ (Superior), affirmed July 2025 |

| Early Pay-Off Options | 10- and 20-year paid-up structures available |

| Notable Rider | Chronic Care Rider — access to death benefit for long-term care costs if certified chronically ill |

| Best For | Veterans and retirees who want premium flexibility and policy customization |

Best for: Veterans planning for retirement who want to reduce premium obligations over time without sacrificing lifetime coverage.

AAFMAA

The Armed Forces Mutual Aid Association has served the U.S. military community exclusively since 1879. As a nonprofit, member-owned organization, its policy language reflects priorities shaped by that mission: no war exclusion, no aviation clause, no terrorism clause on any policy.

| Factor | Details |

|---|---|

| Membership | Active duty, Guard, Reserve, veterans, retirees, and families |

| War Clause | No war exclusion, no aviation clause, no terrorism clause — on any policy |

| No-Exam Option | Guaranteed Acceptance+ available without medical exam ($5,000–$25,000 coverage) |

| Survivor Support | Dedicated survivor services included with membership |

Best for: Military families who want a mission-aligned insurer with guaranteed no-war-exclusion language and access to no-exam coverage for veterans with health conditions.

AAFMAA carries $22.9 billion of insurance in force and $1.25 billion in total admitted assets as of December 31, 2025. Note: AAFMAA is not AM Best-rated; verify current financial strength through their annual reports or your state regulator.

Guardian Life

Guardian is a top-rated mutual insurer that stands out for underwriting flexibility. It's one of the few major carriers that will write whole life policies for applicants with complex health histories, including (per their own underwriting guidelines) HIV-positive applicants meeting certain criteria.

| Factor | Details |

|---|---|

| AM Best Rating | A++ (Superior), affirmed September 2025 |

| Underwriting Flexibility | Accommodates complex health histories including HIV diagnosis |

| Best For | Veterans with service-connected conditions who have been declined elsewhere |

Best for: Veterans with PTSD diagnoses, service-connected injuries, or other health conditions resulting from service who need a carrier willing to underwrite non-standard cases. Confirm specific PTSD and TBI underwriting guidelines directly with Guardian before applying.

SGLI, VGLI, and Private Whole Life: Understanding the Difference

Most servicemembers know about SGLI. Fewer understand what happens to that coverage — and how much it costs — after they leave.

SGLI provides up to $500,000 in group term coverage during active duty at $31/month for the maximum amount. No cash value, no portability. Coverage ends at separation.

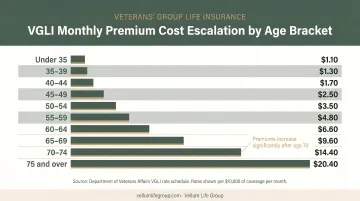

VGLI lets veterans convert SGLI to term coverage post-service without a medical exam — but premiums increase every five years. The escalation is significant. According to current VA rate tables, monthly premiums for $500,000 of VGLI coverage climb as follows:

| Age Bracket | Monthly Premium |

|---|---|

| 50–54 | $145 |

| 55–59 | $250 |

| 60–64 | $425 |

| 65–69 | $690 |

| 70–74 | $1,075 |

| 75–79 | $1,925 |

A veteran paying $145/month at 50 reaches $1,925/month — over $23,000 per year — by their mid-70s, with no cash value accumulation and no guarantee of coverage at the next renewal.

Private whole life locks in premiums at the age you apply. A veteran who purchases a whole life policy at 45 pays the same premium at 75. The policy also builds tax-deferred cash value, never expires, and carries no renewal re-rating. For veterans planning legacy giving, mortgage payoff, or dependent care, whole life becomes the more cost-predictable option once coverage is expected to last beyond the 50s.

One timing detail matters here: veterans must apply for VGLI within 1 year and 120 days of separation. Applying within 240 days requires no proof of good health. After that window, evidence of insurability is required — which is also when exploring private whole life becomes especially relevant for veterans with any health history.

How to Choose the Right Whole Life Policy for Your Military Family

Verify the War Clause First

Some private whole life policies contain war exclusion clauses that void the death benefit if the insured dies in combat or in a declared war zone. This isn't a minor footnote — it's a coverage gap that could leave a military family unprotected precisely when they need the policy most.

USAA and AAFMAA explicitly exclude war clauses on their whole life products. For any other carrier, request the actual policy language and confirm in writing before purchasing.

Confirm Portability and Premium Lock-In

A policy that lapses or requires re-underwriting if you leave active duty defeats the purpose. Look specifically for:

- Premiums fixed at issue age (not adjustable by the carrier)

- Coverage that remains fully in force regardless of coverage status

- No military-status conditions that affect the death benefit

Evaluate Spousal and Dependent Coverage

Military spouses often face career gaps from PCS moves, making their own insurability and coverage needs distinct. When comparing policies, confirm:

- Whether the carrier offers separate spousal whole life policies

- Whether child or dependent riders are available

- How spouse coverage is handled if the servicemember separates or the family relocates

Work With an Advisor Who Can Compare Multiple Carriers

Each carrier handles these factors differently:

- War clause language and how strictly it's applied

- Underwriting standards for service-connected conditions

- Cash value growth rates and dividend history

- Rider availability for spouses and dependents

Comparing these across carriers at once — rather than meeting with individual agents one at a time — saves time and surfaces the best fit faster.

Vellum Life Group works with 10+ A-rated carriers and can review whole life options for military families side by side in a single consultation. Contact Eva Ikonomakos at info@vellumlifegroup.com or 917-363-3554 to get started.

Conclusion

SGLI and VGLI serve an important purpose — but they were never designed to be permanent financial planning tools. They expire, escalate in cost, and build no long-term value. Whole life insurance fills that gap with coverage that doesn't expire, premiums that stay fixed, and cash value that grows independent of market conditions.

The right time to lock in whole life coverage is before a health change, before a deployment, and before an age bracket increase makes the same policy significantly more expensive. Every year of delay typically means higher premiums for the same coverage — a cost military families don't need to absorb.

If you're a military family evaluating your options, Vellum Life Group offers free, no-obligation consultations to compare whole life policies across multiple A-rated carriers, with straightforward guidance and no sales pressure.

Get in touch:

- Email: info@vellumlifegroup.com

- Phone: 917-363-3554

Frequently Asked Questions

What is the best whole life insurance for military families?

There's no single best option — the right policy depends on deployment status, health history, and coverage objectives. USAA and AAFMAA lead for military-specific features and no war exclusions. MassMutual stands out for cash value growth and building wealth across a 20- to 30-year horizon.

Can I get life insurance with a serious medical condition like cirrhosis or Parkinson's?

Guaranteed issue whole life products like AAFMAA's Guaranteed Acceptance+ require no medical exam and are accessible for applicants with serious conditions. Coverage amounts are typically lower ($5,000–$25,000) and premiums higher than standard underwritten policies.

What happens to SGLI coverage when you leave the military?

SGLI ends at separation. Veterans have 1 year and 120 days to convert to VGLI without a medical exam, or apply for private coverage. Delaying that decision until after a health decline often means higher premiums or outright denial.

Is whole life insurance better than VGLI for veterans?

For most veterans who plan to maintain coverage past their 50s, yes. VGLI premiums increase every five years and build no cash value; whole life locks in premiums at issue age and accumulates tax-deferred savings, making it the more cost-effective choice by retirement age.

Do private whole life policies cover death during combat or deployment?

It depends on the carrier. USAA and AAFMAA explicitly cover all causes of death with no war exclusion. Some other carriers include war exclusion clauses — read the policy language carefully before signing.

How much whole life insurance does a military family need?

A common starting point is 10x annual income, per NerdWallet's 2026 coverage guidance. Military families should also weigh mortgage balance, number of dependents, and any existing SGLI or VGLI coverage. The VA's Insurance Needs Calculator includes military-specific inputs like SBP and DIC.