Introduction

Most parents spend real energy protecting their children — car seats, helmets, healthy food, pediatrician checkups. But according to LIMRA's 2024 Insurance Barometer Study, 42% of U.S. adults — roughly 102 million people — say they need life insurance or more of it. That gap is especially risky for parents, where the financial consequences of being underinsured fall directly on children.

The right coverage amount isn't a single fixed number. It shifts based on your income, how many children you have, outstanding debt, whether one or both parents work, and what you plan to fund — college, ongoing childcare, or both.

This article walks through coverage tiers, the factors that move your number up or down, three calculation methods, and real-world scenarios for common family structures. By the end, you'll have a realistic starting number you can actually stand behind.

Key Takeaways

- Most parents need coverage of 10–15× their gross annual income, adjusted upward for each child, an outstanding mortgage, and planned education costs

- Coverage increases for: single-income households, multiple young dependents, significant debt, or a non-earning parent at home

- Coverage may be lower for: dual-income couples with substantial savings and older children nearing independence

- Choose a term policy that ends when your youngest child reaches financial independence

- Revisit your coverage after any major life event: new child, home purchase, divorce, or income change

How Much Life Insurance Do Parents with Children Need?

There's no universal dollar figure, but financial professionals consistently point to a baseline range parents can use as a starting point. The real risk is at the extremes: buying too little leaves children without adequate support; buying more than necessary strains your monthly budget and may eventually lead to a lapsed policy.

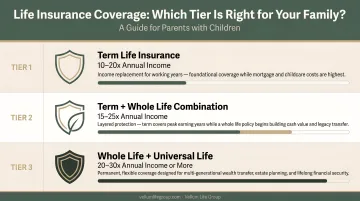

Here are the three most commonly cited coverage tiers:

| Coverage Tier | Range | Best For |

|---|---|---|

| Minimum | $250,000–$500,000 | Dual-income households with low debt and existing savings |

| Standard | $500,000–$1,000,000 | Single-income families, mortgage holders, two or more young children |

| Comprehensive | $1,000,000+ | High earners, single parents, large families, or complex financial situations |

Minimum Coverage: $250,000–$500,000

This range addresses immediate expenses — funeral and final medical costs, short-term income replacement for one to two years, and clearing smaller debts like credit cards or a car loan.

Fits best when: You're in a dual-income household with one or two children, carry lower debt, and have existing savings or assets that could help the surviving partner stay afloat.

Standard Coverage: $500,000–$1,000,000

This range covers sustained income replacement for 10 or more years, mortgage payoff, ongoing childcare costs, and a college education fund. It's the tier most parents with young children end up in.

Fits best when: You're a single-income family, carry a mortgage, or have two or more young children where the surviving parent would need time — and money — to restabilize.

Comprehensive Coverage: $1,000,000+

This range is designed to fully replace income across the entire child-rearing period, eliminate all household debt, and fully fund college for multiple children. It removes the need for the surviving parent to make hard trade-offs.

Fits best when: You're a high-income earner, single parent, or part of a large family — or any household where losing one income would permanently reshape what the family can afford.

Key Factors That Determine How Much Coverage You Need

The right coverage amount comes from a combination of financial obligations, household structure, and long-term goals. No two families land in the same place.

Income Replacement Needs

The core function of life insurance for parents is replacing lost income over the years a child remains financially dependent. A parent earning $70,000 per year with a 15-year runway represents over $1,050,000 in gross income before factoring in any returns if the benefit is invested.

- Single-income households need to replace 100% of that income

- Dual-income households still face significant disruption — the surviving spouse often can't simply continue working at the same level while managing solo parenting

Number and Age of Your Children

More children extend the financial support horizon. A parent of a newborn needs coverage that lasts 18–22 years; a parent of a 15-year-old may only need 5–8 more years of income replacement.

NerdWallet's 2026 coverage guidance recommends adding $100,000 per child for estimated education costs on top of base income replacement.

Outstanding Debt and Mortgage

All household debt should be factored in directly. The goal is to ensure the surviving parent isn't forced to sell assets or absorb unexpected financial strain. Common line items include:

- Mortgage balance (typically the largest single item)

- Car loans and student debt

- Credit card balances

Each of these becomes the surviving parent's responsibility — without a buffer in place.

The Stay-at-Home Parent Factor

At four years per degree, even the in-state option clears $116,000 — and that figure doesn't include room, board, or the inflation that will accumulate before your child enrolls.

How to Calculate Your Life Insurance Coverage as a Parent

Several calculation methods exist. Use at least two approaches and take the higher result as your starting point.

The Income Multiplier Rule

Multiply your gross annual income by 10–15, then add $100,000 per child to account for education costs. This is a quick estimate — useful for getting into the right range, not for precision planning.

Example: $80,000 × 12 = $960,000 + $200,000 (two children) = $1,160,000 coverage target

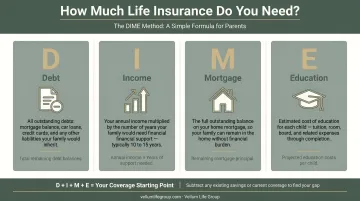

The DIME Method

DIME stands for:

- D — Debt: Add up every outstanding liability — credit cards, car loans, and student loans

- I — Income: Multiply your annual income by the years until your youngest child is financially independent

- M — Mortgage: Include the full remaining balance on your home loan

- E — Education: Factor in projected college costs for each child

Add all four figures together. The total gives you a coverage target that accounts for every major financial obligation, not just income replacement.

The Needs Analysis Approach

Total all projected family expenses if you were to pass away, then subtract existing financial resources — savings, investments, the surviving spouse's income, and any existing life insurance. The remainder is the coverage gap a new policy needs to fill.

This method tends to produce the most accurate figure because it accounts for what your family already has, not just what they'd lose.

Working with an Advisor to Model Scenarios

These formulas are starting points, not finished answers. Running two or three methods and comparing results gives you a much clearer target range than any single formula alone.

An independent advisor can model those scenarios side by side and pull actual quotes across multiple carriers. Vellum Life Group works with 10+ A-rated carriers, including Mutual of Omaha, Corebridge Financial, Transamerica, and Ameritas. A free 30-minute consultation is available with no obligation.

Policy Term Length: How Long Should Coverage Last?

Choose a term that extends until your youngest child reaches financial independence, typically age 22–25. A 20-year term covers most parents of young children. A 30-year term makes sense for parents of newborns who also carry a long mortgage. Match the term to the actual financial runway, not a round number.

Real-World Scenarios: Coverage by Family Size and Situation

Coverage needs shift significantly based on household structure. The examples below illustrate how the same income produces very different recommended amounts.

Dual-Income Couple, Two Young Children, Mortgage

Consider a household where both parents earn $75,000 annually. Each parent should carry their own separate policy — the household can't function on one income alone. Each policy should reflect that parent's individual income × 10–15, plus a share of the outstanding mortgage, plus $100,000 per child for education.

With a $400,000 mortgage and two young children, each parent ends up in the $1,000,000–$1,200,000 range. The obligations are specific and the math drives the number.

Single Parent with One or More Children

Single parents carry the entire financial burden. A typical target is 15× income plus full debt elimination plus full education funding — often $1,000,000 or more even at moderate income levels.

Beyond the policy itself, name a trusted guardian in your will and designate a financial trustee to manage any death benefit on behalf of minor children.

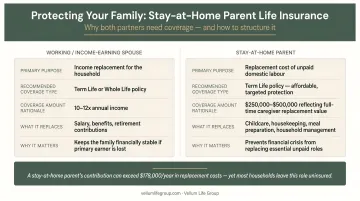

Stay-at-Home Parent Household

This structure requires two separate policies with different purposes:

- Working parent carries high income-replacement coverage — typically 15× salary or more, plus full debt coverage

- Stay-at-home parent needs a policy sized to replace years of childcare and household management at actual market rates, for as long as the children remain at home

What Most Parents Get Wrong About Life Insurance Coverage

Three patterns come up repeatedly among families who discover their coverage is inadequate:

Relying on group life insurance as their primary coverage. Group plan policies typically provide only 1–2× your annual salary — well below the 10–15× recommended range. They also disappear the moment a plan changes or lapses, leaving no coverage during transitions.

Buying based on monthly premium alone. Saving $30–$50 per month by choosing a lower face amount can create a six-figure coverage gap. The premium is what you pay; the coverage amount is what your family actually receives. Work backward from the coverage need, then find the best rate for that amount.

Failing to update coverage after major life events. A policy purchased before children, before a mortgage, or before a salary increase may be severely undersized for your current reality. Annual reviews — or a review after any major life change — keep your coverage matched to your actual obligations, not a snapshot of your life from five years ago.

The right coverage reflects what your family genuinely needs — not a round number chosen because the premium felt manageable. If your last review was more than a year ago, that's the first thing worth fixing. An independent advisor like Vellum Life Group can compare options across multiple carriers and identify gaps in your current coverage, typically within a single conversation.

Frequently Asked Questions

How much life insurance should I have with three kids?

Parents with three children should target roughly 12–15× gross income plus mortgage payoff plus education costs for each child. A single-income household with three young children will typically need $1,000,000 or more, even at moderate income levels.

How much is life insurance for a family of three?

For a healthy 35-year-old non-smoker, NerdWallet's 2026 rate data estimates a $500,000 / 20-year term policy at roughly $22.79/month for women and $28.17/month for men. Most families find the cost more manageable than they anticipated. For coverage amounts, see the calculation methods above.

Does having more children mean I need more life insurance?

Yes. Each additional child extends your income replacement horizon, adds education costs, and increases total household expenses. Coverage should be reassessed after every new child is born.

Do both parents need life insurance, even if one stays at home?

Both parents need coverage. The working parent replaces income; the stay-at-home parent covers the cost of childcare and household services that would need to be hired — at real market rates — if they were to pass away.

What term length should parents with young children choose?

Align the term to the year your youngest child is expected to be financially independent. A 20-year term works for most parents of young children; a 30-year term may be appropriate if you also carry a long mortgage.

How does my mortgage affect how much life insurance I need?

The outstanding mortgage balance should be added directly to your coverage calculation. It's typically the largest single line item in a family's total coverage need, and leaving it out could force the surviving spouse to sell the family home.