Short-term life insurance exists for exactly these moments. It's not a permanent solution, and it's not designed to replace a long-term policy. But when you need protection for a few weeks or months while your life is mid-transition, it does the job.

This guide covers what short-term life insurance actually is, the two main types you'll encounter, when it makes sense to use it, what it costs, and how to apply — so you can make a clear-headed decision about whether it fits your current situation.

Key Takeaways

- Short-term life insurance provides temporary coverage — typically 90 days to one year — designed to fill gaps, not replace long-term protection

- Two main types exist: temporary life insurance (tied to a long-term application) and annual renewable term (standalone, one-year coverage)

- Common use cases include job transitions, underwriting wait periods, and short-term financial obligations

- Premiums for annual renewable term start lower but increase every year at renewal, adding up significantly over time

- Many short-term policies are approved same-day or within a few business days due to simplified underwriting

What Is Short-Term Life Insurance and How Does It Work?

Short-term life insurance provides temporary death benefit coverage — generally lasting no more than one year — paying a lump sum to named beneficiaries if the policyholder dies during the active coverage period.

The mechanics are identical to standard life insurance: you pay premiums, your beneficiaries are protected, and the insurer pays out if you die during the term.

The critical distinction is duration. Standard term life policies run 10–30 years. Short-term coverage runs months, sometimes just 60–90 days, and it's designed as a bridge to fill a temporary gap — not a long-term foundation.

What It Covers (and What It Doesn't)

Short-term policies pay a death benefit for most causes of death during the coverage period, similar to traditional term life. What they don't include:

- No cash value — purely a death benefit tool

- No investment or savings component

- No long-term financial planning benefits

Common exclusions worth knowing before you sign:

- Suicide clauses (the Insurance Compact's term standards cap these at two years)

- Deaths resulting from fraud or material misrepresentation (also contestable for up to two years)

- Hazardous activities not disclosed at application — aviation, skydiving, and certain occupations can be specifically excluded

If your occupation or hobbies fall into a higher-risk category, confirm how your specific policy handles those exclusions before coverage begins.

A Common Misconception

Short-term life insurance is not a cheaper workaround for long-term coverage. It's a tactical, temporary tool. Using it as a substitute for long-term planning leaves families underprotected — and annual renewable premiums climb year over year, making that substitution increasingly expensive anyway.

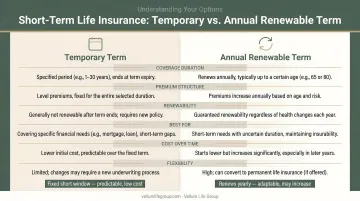

Types of Short-Term Life Insurance

Short-term life insurance isn't one product — it's two. Each works differently, costs differently, and fits a different situation.

Temporary Life Insurance

Temporary life insurance is coverage issued by an insurer while your long-term policy application is under review. It bridges the underwriting period — typically up to 90 days — so you're not unprotected while the insurer evaluates your application.

Key facts about how it works:

- Cannot be purchased standalone — it's tied directly to your long-term policy application. Carriers like Banner Life require both the application and temporary agreement to be completed together, with payment submitted at the same time.

- Benefit limits vary by carrier. Banner Life, for example, caps temporary coverage at the lesser of the applied-for amount or $1,000,000.

- Coverage expires when your application is approved or declined — whichever comes first.

- Pre-existing health conditions may affect eligibility during the underwriting period. This varies by carrier form.

On costs: some carriers require an advance premium payment upfront, while others credit that amount toward your long-term policy once issued. The net cost is sometimes zero for the bridge period — but this is carrier-specific, not a universal rule.

Annual Renewable Life Insurance

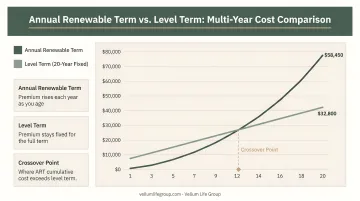

Annual renewable term (ART) is a standalone one-year policy that renews each year without requiring a new medical exam. According to New York Life, yearly renewable term starts with low premiums that increase annually as the insured ages.

The trade-off is straightforward: premiums start lower than a comparable level-term policy, but rise every year at renewal based on your age. Over several years, ART becomes significantly more expensive than locking in a 10- or 20-year level-term rate from day one.

ART works well for people who expect to move to a longer-term policy soon.

Ideal candidates for ART:

- Someone recovering from a health condition who plans to apply for better rates in 12 months

- A person who recently quit smoking and wants to wait for their tobacco-free period to qualify for lower rates

- Someone in a temporarily high-risk occupation who doesn't want that job to drive up permanent premiums

When Does Short-Term Life Insurance Make Sense?

Short-term coverage isn't for everyone — but in the right circumstances, it solves a problem that a standard 20-year policy simply can't.

Waiting for Underwriting to Complete

Traditional underwriting takes time. According to LIMRA, the average final decision takes 9 days under accelerated underwriting programs and 27 days through traditional underwriting. If you applied for a 20-year policy and have no coverage in the meantime, temporary life insurance closes that window.

Between Group Plans

Group life insurance ends when the plan lapses. With median plan tenure at just 3.5 years in the private sector as of January 2024, coverage transitions are common — and coverage gaps don't need to be. A short-term policy bridges the period between your last group plan and your next one (or a private policy you're securing).

Working Toward Better Rates

If you quit smoking six months ago, lost significant weight, or recovered from a health condition, insurers may not yet reflect that progress in your rate class. Annual renewable term lets you maintain coverage while you build the health history that unlocks lower premiums — typically 12 months of documented improvement is enough to re-apply for preferred rates.

Covering a Specific Financial Obligation

Short-term policies can be matched to a specific risk window — a bridge mortgage, a personal loan, or any short-term debt where your death would create a financial problem for someone else. Coverage that mirrors the obligation timeline is more precise than carrying a 20-year policy for a 12-month liability.

Temporary High-Risk Work

Someone working a short-term job in an elevated-risk environment — offshore, logging, or construction — may not want that occupational classification driving their permanent premiums for decades. A one-year policy covers the period without affecting their long-term cost structure.

How Much Does Short-Term Life Insurance Cost?

ART premiums aren't published in widely available tables the way level-term rates are. What carriers do make clear is which factors drive the cost:

Factors that affect your short-term premium:

- Age (the most significant driver for ART)

- Gender

- Health status and tobacco use

- Coverage amount

- Type of policy (temporary vs. annual renewable)

- The specific carrier

For context on level-term costs: Guardian's 2025 rate data shows average monthly premiums for a 10-year term policy at roughly $13/month for $250,000 and $37/month for $500,000 in coverage. ART premiums for younger, healthy applicants tend to start in a similar range — but those premiums increase every year at renewal, while level-term rates stay flat for the entire policy period.

A 35-year-old who buys ART and renews for 10 years will pay significantly more over that decade than someone who locked in a 10-year level-term policy from day one. The starting price looks similar — the cumulative cost does not. ART wins on cost only when the coverage need is genuinely short: two years or less.

| Scenario | ART | Level-Term |

|---|---|---|

| Year 1 premium | Low (similar to level-term) | Fixed |

| Year 5 premium | Higher (increases annually) | Same as Year 1 |

| Best for | Gaps under 2 years | Needs of 3+ years |

For temporary life insurance costs during underwriting: in some cases, one month's premium is collected and later credited to your long-term policy, making the bridge period effectively free. In other cases, the insurer requires a payment upfront. Ask your advisor which applies before you commit to a carrier.

How to Apply for Short-Term Life Insurance

The application process is straightforward, and approval is often faster than most people expect.

Step-by-step:

- Identify your coverage type — Do you need temporary coverage tied to a long-term application you're already submitting? Or a standalone annual renewable policy?

- Gather basic information — Age, health history, tobacco use status, coverage amount needed, and beneficiary details

- Compare carriers — Not every insurer offers both types of short-term coverage, and underwriting criteria vary significantly

- Submit the application — For temporary coverage, this happens alongside your long-term policy application; for ART, it's a separate submission

- Receive approval — Simplified-issue and no-exam policies can be approved the same day or within a few business days

The speed advantage of short-term policies comes from simplified underwriting. Rather than a full medical exam, many policies use health questionnaires or database checks to reach a decision quickly. Policies requiring a medical exam take longer (typically 2–4 weeks).

Knowing which path fits your situation — and which carriers will approve you — is where working with an independent licensed advisor makes a real difference. Eva Ikonomakos at Vellum Life Group handles exactly that. Rather than approaching carriers individually, an advisor can evaluate your health profile, identify which carriers are most likely to approve your application, and simultaneously determine whether a longer-term policy might be a better fit from day one — all in a single free consultation. Vellum Life Group works with 10+ A-rated carrier partners, which matters when your health profile or situation doesn't fit cleanly into a single carrier's underwriting criteria.

Frequently Asked Questions

Is short-term life insurance a good idea?

It's a good idea for specific transitional situations — coverage gaps between jobs, waiting periods during underwriting, or short-term financial obligations. For most people, it should be a temporary bridge, not a long-term strategy. Relying on annual renewable term for more than a couple of years becomes costly.

Can I get short-term life insurance if I have a pre-existing condition?

Eligibility varies by condition and carrier. Some conditions may disqualify applicants from temporary coverage tied to a long-term application, while annual renewable policies often carry more underwriting flexibility. An independent advisor can identify the carriers most likely to approve your specific health profile.

How long does short-term life insurance last?

Temporary life insurance typically lasts up to 90 days — covering the underwriting period for a long-term application. Annual renewable life insurance lasts one year and can be renewed each year without a new medical exam.

What's the difference between short-term and term life insurance?

Short-term life insurance covers a period of one year or less; traditional term life covers 10–30 years. Both offer a death benefit without cash value, but they serve entirely different purposes and have very different cost structures over time.

Can you convert short-term life insurance to a long-term policy?

Temporary life insurance is already tied to a long-term application, so conversion is built into the process. Annual renewable term generally doesn't convert, but you can start a new long-term application at any point while your ART policy remains active.

How quickly can short-term life insurance be approved?

Many short-term policies use simplified or no-exam underwriting, meaning approval can happen the same day or within a few business days. Policies that require a medical exam take longer — typically 2–4 weeks.