This crossroads matters more for seniors than any other age group. Term availability narrows with age, health complications affect eligibility, and the reason most seniors want $50,000 in coverage — final expenses, small debts, a modest legacy — doesn't look the same as a 35-year-old's income replacement need.

This article breaks down how each policy type works at the $50,000 level, what seniors realistically pay, and a clear framework for deciding which fits your situation.

Key Takeaways

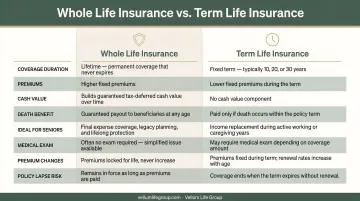

- Whole life provides permanent, locked-in coverage with modest cash value — best for final expense planning and legacy goals.

- Term life costs less upfront but expires, and seniors risk outliving the policy with no payout.

- Those in their early 60s covering a specific debt or time-bound obligation may find term more cost-efficient.

- At 70 or older — or with health conditions — whole life or guaranteed issue is typically the practical path.

- The right choice hinges on age, health, budget, and purpose — there's no universal answer.

Whole Life vs. Term at $50,000: A Quick Comparison

Both options can work for seniors — the right choice depends on your goals, budget, and health. Here's how they compare at the $50,000 coverage level.

| Feature | Whole Life | Term Life |

|---|---|---|

| Coverage Duration | Permanent — never expires if premiums are paid | Temporary — typically 10 or 20 years |

| Monthly Cost (Age 70) | ~$305–$344/month (female/male, non-smoker) | Lower, but exact $50K rates vary by carrier |

| Cash Value | Builds over time; can be borrowed against | None |

| Medical Exam | Usually not required (simplified underwriting) | Health questions required; stricter underwriting |

| Age Availability | Available up to age 85 with most carriers | 20-year terms often cut off at 65–70 |

| Guaranteed Issue Option | Yes, for those who can't medically qualify | No — term generally doesn't offer guaranteed issue |

The rate shown for whole life at age 70 comes from Policygenius's senior life insurance comparison data (updated July 2024, based on MassMutual policies in Preferred health class). These are illustrative benchmarks — your actual rate will vary by carrier, state, and health profile.

What Is $50,000 Whole Life Insurance for Seniors?

Whole life is permanent coverage that lasts your entire life. The $50,000 death benefit is guaranteed from day one, and your premiums are locked in at the age you apply — they never increase even if you turn 80 or get a new diagnosis.

How the Cash Value Works

A portion of each whole life premium goes into a cash value account that grows at a guaranteed rate. At $50,000 in coverage, this isn't a wealth-building tool. But after 10–15 years, a senior could borrow against it for unexpected expenses — a medical bill Medicare doesn't cover, a home repair, or a family emergency.

What Seniors Pay for $50,000 Whole Life

Verified benchmark rates for non-smokers in Preferred health (based on Policygenius data, October 2024):

| Age | Female | Male |

|---|---|---|

| 60 | ~$175/month | Not publicly verified |

| 70 | ~$305/month | ~$344/month |

Rates for ages 65, 75, and 80 were not found in verified public sources — the figures above are illustrative. For accurate pricing, compare rates across carriers including Mutual of Omaha, Transamerica, and Foresters Financial directly.

How Seniors Qualify

Most $50,000 whole life policies for seniors use simplified underwriting — a set of health and lifestyle questions with no blood draw or physical exam required. Many can be approved within days.

For seniors who can't pass health questions — due to serious conditions like Parkinson's, cirrhosis, or recent cancer — guaranteed issue whole life is the alternative. It asks no health questions and approves everyone who applies, but comes with two important trade-offs:

- A 2-year waiting period for natural death claims (accidental death is typically covered immediately)

- Lower per-policy coverage caps — Mutual of Omaha, for example, caps guaranteed issue coverage at $2,000–$25,000 per policy, meaning you'd need two policies from different carriers to reach $50,000

When Whole Life Makes Sense

- Covering funeral and burial costs — the 2023 national median funeral with burial runs $8,300, and $50,000 covers this plus outstanding medical bills and small debts

- Leaving a modest, tax-free inheritance for children or grandchildren

- Ensuring permanent coverage regardless of future health changes

- Seniors 70+ for whom term is no longer practical or available

What Is $50,000 Term Life Insurance for Seniors?

Term life pays the $50,000 death benefit only if the insured dies during the policy's term. Once the term ends (whether 10 or 20 years), coverage stops, no payout is made, and no cash value is returned.

The Age Cutoff Reality

Term availability shrinks fast with age. Banner Life's OPTerm product illustrates the pattern: OPTerm 20 is available to non-tobacco applicants up to age 70, while OPTerm 10 extends to age 75. Many carriers stop offering 20-year terms at 65–70, and some stop term coverage altogether at 75.

That means a 68-year-old shopping for a 20-year term may find their options already limited — and a 73-year-old may find only 10-year terms, if anything.

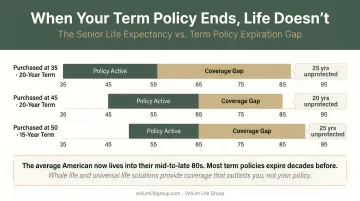

The Outliving Risk

This is the scenario that trips up many seniors. Consider the math: according to SSA actuarial life tables, a 65-year-old male has an average remaining life expectancy of 18.12 years, and a female's is 20.66 years. A 10-year term policy at age 65 expires at 75 — well before average life expectancy for both sexes.

The gap widens further at older entry ages. A 70-year-old buying a 10-year term is covered only until 80, yet average life expectancy at 70 is another 14–17 years depending on sex — meaning most buyers in this bracket will outlive the policy and leave nothing behind.

When Term Actually Makes Sense for Seniors

Term is a smart fit in specific situations:

- A 62-year-old with 12 years left on a mortgage who wants the lowest possible premium during that window

- A senior who co-signed a child's loan and needs coverage only until the debt is paid off

- Someone in excellent health in their early 60s who wants to maximize coverage per dollar during their healthiest years

- A spouse who wants coverage until their partner reaches full retirement age and Social Security income increases

Whole Life vs. Term: Which Is Right for You?

Before picking a policy type, work through four questions:

- What is this $50,000 for? Final expenses, a specific debt, or a legacy goal all point to different answers.

- Do I need coverage for life, or for a defined window? If there's an end date on the need, term may suffice.

- What can I realistically afford each month? Whole life premiums run higher — on a fixed income, the payment needs to be sustainable indefinitely.

- What's my current health status? Medically underwritten term requires health qualification. Seniors with serious conditions may not qualify.

Choose Whole Life If:

- Your primary goal is covering final expenses or leaving a legacy

- You are 70 or older — term availability is too limited to be reliable

- You want the certainty that premiums won't increase and coverage won't expire

- Health conditions may worsen over time, making future coverage harder to obtain

Choose Term If:

- You're in your early-to-mid 60s and in good health

- You have a specific obligation — a mortgage, a co-signed loan — with a clear end date

- You want the maximum coverage per dollar during a defined window

- You're comfortable with the risk that the policy may expire before you do

The Third Path: Guaranteed Issue Whole Life

If neither standard whole life nor term is a realistic option due to health, there's still a path forward: guaranteed issue whole life. No health questions, no medical exam, no possibility of denial. The trade-offs are real — higher premiums, a 2-year limited benefit period for natural death, and per-policy caps (typically $25,000 per carrier) that may require buying two separate policies to reach $50,000.

For seniors navigating these health-based limitations, comparing carriers side by side matters. Eva Ikonomakos at Vellum Life Group works with 10+ A-rated carriers — including Mutual of Omaha, Transamerica, and Foresters Financial — and can run those comparisons across guaranteed issue and simplified issue options to find the most favorable terms available.

Frequently Asked Questions

How much does a $50,000 life insurance policy for seniors cost per month?

Costs vary significantly by policy type and age. Illustrative benchmarks: a 70-year-old in Preferred health might pay roughly $305–$344/month for whole life (female/male). Term runs considerably lower but exact $50K senior rates vary by carrier. Health status and gender both affect final pricing.

What is the best life insurance for seniors over 65?

For most seniors over 65, whole life is the more practical choice — term becomes harder to obtain and increasingly expensive with age, while whole life offers permanent coverage with locked premiums. The best option depends on individual health, budget, and what the coverage is meant to accomplish.

Can seniors with conditions like cirrhosis or Parkinson's get $50,000 life insurance?

Serious pre-existing conditions typically disqualify seniors from medically underwritten policies. Guaranteed issue whole life is available regardless of health history, but it carries higher premiums, a 2-year waiting period for natural death benefits, and per-carrier caps near $25,000, so two policies are often needed to reach $50,000.

Does $50,000 in life insurance cover funeral expenses?

Yes — $50,000 comfortably exceeds the 2023 NFDA national median funeral cost of $8,300 for burial and $6,280 for cremation, leaving room for medical bills, small debts, or a family bequest.

Is term life insurance available for seniors over 70?

Options narrow sharply after 70. Most carriers limit 20-year terms to applicants under 70, and 10-year terms may extend to 75 with select carriers. For most seniors past 70, whole life or guaranteed issue is the more accessible and reliable path.

What is the difference between whole life and guaranteed issue life insurance?

Whole life with simplified underwriting requires health questions and offers immediate full coverage. Guaranteed issue asks no health questions and approves everyone, but includes a 2-year waiting period before natural death benefits pay out in full.