Many families never need to think much about how the benefit eventually reaches them, and that's perfectly okay. Still, understanding the basics ahead of time tends to bring real peace of mind. It means your loved ones won't be left guessing, and you can feel confident that the protection you've chosen will do exactly what you intended.

This guide gently walks through what life insurance is, what beneficiaries can generally expect, the payout options families typically have, and the small, simple steps you can take now so everyone feels prepared and supported.

Key Takeaways

- Life insurance is a caring way to protect the people who depend on you, providing financial support for your family's future

- A death benefit is paid to the people you name as beneficiaries — choosing and updating them thoughtfully matters

- Families usually have several payout options, from a single lump sum to ongoing payments, depending on what suits them best

- Death benefits are generally not subject to federal income tax, which means more of the protection reaches your loved ones

- Keeping documents accessible, designations current, and coverage reviewed are simple, low-effort ways to look after your family today

What Life Insurance Does for Your Family

At its heart, life insurance is a promise. You pay a premium, and in return the insurer agrees to pay a sum of money — the death benefit — to the people you've chosen, should something happen to you. That money can help cover everyday living costs, a mortgage, education, or simply give your family room to breathe during a difficult season.

The people who receive the benefit are called your beneficiaries. You name them when you set up the policy, and you can update them over time. This is one of the most meaningful parts of any policy, because it decides exactly who your protection is meant to reach.

Thinking about coverage early, while life is calm, tends to be far easier than waiting. It lets you choose thoughtfully, match the policy to your family's real needs, and rest knowing the plan is in place.

What Beneficiaries Can Generally Expect

If you already hold a policy, it can be reassuring to understand, in broad terms, how the benefit eventually reaches your family. None of this needs to be memorized — it's simply meant to take the mystery out of the process so your loved ones feel less alone if the day ever comes.

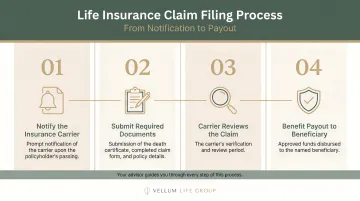

A Benefit Is Requested, Not Automatic

A death benefit is typically paid once a beneficiary lets the insurer know and shares a few details. Insurers are generally required to acknowledge a request and provide clear instructions promptly. Under NAIC model claims regulations, carriers usually acknowledge a request and provide the necessary information within about 15 days.

A Few Simple Documents Are Usually Involved

Insurers generally ask for a certified copy of the death certificate, some basic information about the policy and the beneficiary, and a completed form. A certified death certificate can usually be obtained from the funeral home, the attending physician, or the local vital records office. It's common to request a few copies, since other institutions may each need their own.

A Gentle Review, Then the Benefit

The insurer confirms the policy was active and that the beneficiary details match what's on file, then arranges payment. MassMutual reports that many benefits are paid within a matter of weeks once everything is in order, and some straightforward cases resolve even faster.

The most important thing to know is that this process exists to deliver on the promise you made. Insurers are obligated to honor valid policies, and the benefit is there to support your family — exactly as you intended.

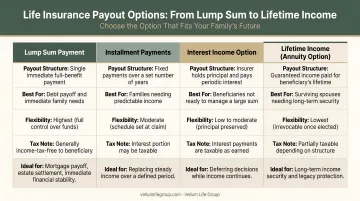

How Life Insurance Payouts Work

When the time comes, families usually have a choice in how they'd like to receive the benefit. Knowing these options ahead of time can make a thoughtful conversation easier:

| Option | How It Works |

|---|---|

| Lump Sum | The full benefit is paid at once — the most common choice |

| Installment Payments | The benefit is distributed in scheduled amounts over a fixed period |

| Lifetime Income | The benefit is converted to ongoing monthly payments for life or a set term (administered directly by the carrier) |

| Interest-Only | The insurer holds the principal while paying interest; the beneficiary decides later |

Tax Considerations

One of the reassuring features of life insurance is its favorable tax treatment. According to IRS Publication 525, life insurance death benefits are generally excluded from federal income tax. A few things are worth keeping in mind:

- Interest earned on proceeds (common with installment options) is generally taxable as income

- Federal estate taxes may apply only if the total estate exceeds $13,990,000 in 2025 (per IRS estate tax thresholds)

- State-level estate or inheritance taxes can apply at lower thresholds in some states — Oregon at $1 million, Massachusetts at $2 million, Illinois at $4 million, for example

For most families, the benefit arrives largely intact. If your estate is sizable, a tax advisor can help you plan thoughtfully.

What Shapes the Final Amount

The amount a family receives is usually the policy's face value, though it can differ if outstanding policy loans remain, premiums were unpaid, or multiple beneficiaries share the proceeds. Understanding your own policy's details today means there are no surprises later.

Simple Ways to Prepare Your Family Today

The most caring step isn't navigating paperwork — it's planning ahead so your family never has to wonder. A little preparation now goes a long way, and it takes very little time.

What to Do Now

- Let your beneficiaries know they're named. Your loved ones simply benefit from knowing a policy exists and what it's meant to provide.

- Store your details somewhere accessible. Keep the policy document, insurer name, policy number, and contact information alongside your will or estate papers — not locked away where no one else can reach it.

- Keep beneficiary designations current. Marriage, divorce, or the birth of a child are all natural moments to revisit who receives the benefit.

- Name a contingent beneficiary. If your primary beneficiary is no longer able to receive the benefit, naming a backup keeps everything clear and smooth.

These small habits ensure the protection you've put in place reaches exactly the people you intended, with as little friction as possible.

The Value of an Annual Policy Review

Life changes, and so do a family's needs. A relaxed, no-pressure review of your coverage from time to time helps keep everything aligned:

- Beneficiary names stay current

- Coverage continues to match your family's real financial picture

- Premium payments and policy details stay in good standing

Eva Ikonomakos at Vellum Life Group sees these check-ins as a natural part of caring for the families she works with — a chance to make sure your coverage still fits your life and to answer any questions, gently and without obligation.

Families who plan thoughtfully tend to feel calmer and more confident. The goal isn't to dwell on difficult moments — it's to put a quiet, dependable plan in place so the people you love are looked after.

Frequently Asked Questions

How do I choose the right beneficiaries?

Think about who depends on you financially, and consider naming both a primary and a contingent beneficiary as a backup. It also helps to revisit your choices after major life events like marriage, divorce, or a new child, and to review designations as part of a broader life insurance check-in.

Can someone buy life insurance on another person — for example, a son buying a policy for his father?

Yes, provided the purchaser has an insurable interest — meaning they have a genuine financial stake in the insured's life. Adult children insuring a parent typically qualify. The insured must consent to and take part in the application process.

How is a life insurance benefit usually received?

Families generally choose from a lump sum, installment payments, lifetime income, or an interest-only arrangement. A lump sum is the most common, and understanding how the benefit works ahead of time helps everyone feel prepared.

Why does keeping my policy details accessible matter?

Keeping your policy document and insurer details somewhere your family can find them — and staying on top of your policy over time — means your loved ones aren't left searching during an already tender moment.

Are life insurance death benefits taxable?

Death benefits are generally not subject to federal income tax, which is one of the most reassuring features of life insurance. Very large estates exceeding $13,990,000 in 2025 may face federal estate taxes, and some states impose estate or inheritance taxes at lower thresholds. Interest earned on installment payouts is generally taxable — a tax advisor can help with larger estates.