That gap between perception and reality is bigger than you might think. According to Life Happens and LIMRA's 2024 Insurance Barometer Study, **72% of Americans overestimate the true cost of term life insurance** — and many never even get a quote because of it.

This article breaks down exactly what a $1M term life policy costs, what drives the price up or down, how to determine if that coverage level makes sense for your situation, and the mistakes that cost people the most when they go to buy.

Key Takeaways

- A healthy 30-year-old can get $1M in 20-year term coverage for roughly $28–$35/month — less than a monthly streaming subscription

- Age and health are the two biggest cost drivers — every year you wait typically means a higher premium

- Term life costs a fraction of whole life for the same $1M death benefit — sometimes 18x less

- Prices vary widely by carrier — comparing quotes across multiple insurers is the only way to find your best rate

How Much Does a $1 Million Term Life Insurance Policy Cost?

There's no fixed price for a $1M policy. Two people the same age can pay very different premiums depending on their health, gender, and the term length they choose. That said, published rate data from major carriers gives a clear picture of what most healthy non-smokers actually pay.

Typical Monthly Premiums by Age and Term

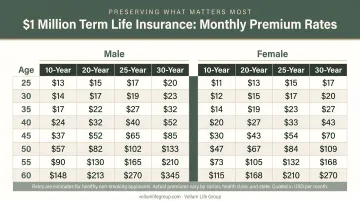

According to Forbes Advisor's 2026 rate data, here's what healthy non-smoking applicants pay for $1M in term life coverage:

| Age | Gender | 10-Year Term | 20-Year Term | 30-Year Term |

|---|---|---|---|---|

| 30 | Female | $19 | $28 | $46 |

| 30 | Male | $23 | $35 | $59 |

| 40 | Female | $28 | $45 | $80 |

| 40 | Male | $32 | $55 | $103 |

| 50 | Female | $64 | $105 | $198 |

| 50 | Male | $78 | $141 | $272 |

The age difference is striking. A 30-year-old male pays $35/month for a 20-year term policy. By age 50, that same coverage runs $141/month — four times the cost, per the Forbes Advisor data above. That gap underscores why locking in a rate early matters.

What Your Premium Covers (and What It Doesn't)

Your term life premium buys one thing: a guaranteed death benefit paid income-tax-free to your beneficiaries if you die during the policy term.

Term life does not include:

- No cash value or savings component

- Pays nothing if you outlive the term

- No return of premiums (unless you add a rider at extra cost)

That stripped-down structure is exactly why term life premiums are so much lower than whole life. You're paying for pure protection — nothing else.

Key Factors That Affect the Cost of a $1 Million Term Life Policy

Life insurance underwriting is a risk assessment. Insurers evaluate the likelihood they'll pay a claim, and every factor below shapes that number.

Age

Age is the most straightforward pricing factor. Older applicants have statistically shorter life expectancies, which increases the insurer's risk. According to Investopedia, premiums generally rise 8% to 10% each year after age 30 for the same coverage.

The Guardian Life data above illustrates this clearly: a male applicant's 20-year term premium jumps from $61/month at 30 to $92/month at 40 to $234/month at 50. Every year you delay locks in a higher rate for the entire term.

Health and Health Classification

Insurers place every applicant into a health tier that determines their rate:

| Classification | General Criteria |

|---|---|

| Preferred Plus | Excellent vitals, no tobacco 36+ months, clean family history, no major conditions |

| Preferred | Good health, no tobacco 24+ months, minor history acceptable |

| Standard Plus | Average health, some medical history, no tobacco 12+ months |

| Standard | Below-average health, some conditions present |

| Substandard/Rated | Significant health history; premiums increase substantially |

Tobacco use has one of the biggest single impacts on premiums. For a $1M 20-year term policy, Policygenius rate data shows the monthly cost difference between smokers and non-smokers:

| Age/Gender | Non-Smoker | Smoker |

|---|---|---|

| 30 Female | $36.90 | $117.20 |

| 30 Male | $48.89 | $143.89 |

| 40 Female | $60.65 | $207.38 |

| 40 Male | $75.24 | $266.49 |

A 40-year-old male smoker pays $191 more per month than his non-smoking counterpart for identical coverage.

Gender

Women statistically live longer than men — the CDC reported a 5.3-year life expectancy gap in 2023. That lower mortality risk translates directly to lower premiums. A healthy 40-year-old woman pays roughly $45/month for a 20-year term policy; a man the same age pays about $55/month.

Term Length

Longer terms cost more because the insurer's exposure window is wider. The probability of a claim on a 30-year policy is higher than on a 10-year policy. A healthy 40-year-old male, for example, pays $32/month for a 10-year term but $103/month for a 30-year term — more than three times as much for the additional coverage window.

Occupation and Lifestyle

High-risk occupations — construction, commercial fishing, law enforcement, aviation — and hazardous hobbies like skydiving or scuba diving can result in higher premiums or specific policy exclusions.

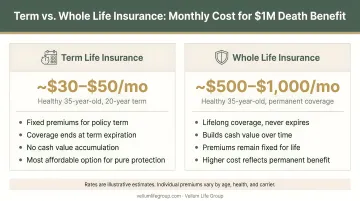

Term vs. Whole Life: How Policy Type Affects Your $1M Premium

The type of policy you choose matters as much as your age and health. A $1M term policy and a $1M whole life policy are not remotely close in price.

Term life provides a death benefit for a set period. Whole life is permanent coverage that also builds cash value over time — and that added complexity comes with a significantly steeper premium.

Policygenius data for a healthy 40-year-old non-smoker makes the contrast clear:

| Policy Type | Male (Age 40) | Female (Age 40) |

|---|---|---|

| $1M 20-Year Term | $75/month | $61/month |

| $1M Whole Life | $1,372/month | $1,161/month |

That's roughly 18 to 19 times more expensive for the same death benefit amount.

Which type makes sense for most people:

- Choose term life for income replacement, mortgage protection, and covering dependents during working years — it's the lowest-cost path to a $1M benefit

- Choose whole life for permanent estate planning, guaranteed cash value growth, or high-net-worth situations where coverage needs outlast a typical career

For most families, term life delivers $1M in coverage at a fraction of the cost — leaving more room in the budget for the life it's meant to protect.

Do You Actually Need $1 Million in Coverage?

Before assuming $1M is the right number, it's worth calculating what your family would actually need. Three common approaches:

- 10–15x annual income rule — Multiply your gross income by 10 to 15. A household earning $80,000/year might need $800K to $1.2M in coverage.

- DIME formula — Add up: Debt (excluding mortgage) + Income replacement (annual income × years until retirement) + Mortgage balance + Education costs for children. This often produces a higher number than the income multiple alone.

- Human Life Value — Estimates the present value of your future earnings, factoring in expenses and taxes. Useful for high-income households.

Run the numbers using any of these methods and you'll often land at — or above — $1 million. That's not a coincidence.

Who Typically Needs $1M in Coverage

Several common profiles point directly to this coverage level:

- Growing families with young children — replacing 10–20 years of income requires substantial coverage

- Homeowners with a large mortgage — a $400K+ mortgage alone accounts for most of that benefit

- Single-income households — the financial stakes of losing that income are high

- High earners — a 10x income rule for a $100K earner lands squarely at $1M

- High earners with significant obligations — coverage often needs to match the full scope of income, debts, and legacy goals, which frequently exceeds $1M

Premiums vary meaningfully across carriers for the same applicant profile. Comparing quotes across multiple insurers — rather than accepting the first rate you see — is the most practical way to find accurate pricing for your situation. Vellum Life Group works with 10+ A-rated carriers, which makes it straightforward to see how your options stack up side by side.

What Most People Get Wrong About $1 Million Life Insurance

Assuming It's Unaffordable Without Checking

LIMRA found that adults ages 18 to 30 overestimate the cost of a $250,000 20-year term policy by 10 to 12 times. The actual monthly cost for a healthy 30-year-old buying $1M in coverage is often around $35. For most households, that's a negligible line item compared to the income it protects.

Waiting Until "The Right Time"

If you have dependents or financial obligations, delay has a real cost. Every year you wait, your premium increases by roughly 8% to 10%. A health event in the meantime — even something minor like elevated blood pressure — can push you into a higher rate class or result in a decline altogether. Once you need coverage, the clock is already running.

Shopping With Only One Carrier

Premiums for the identical $1M policy can vary substantially from one insurer to another. One carrier might rate your blood pressure history as Standard; another might place you at Standard Plus. Without comparing multiple quotes, you have no way of knowing whether you're getting a competitive rate — or paying hundreds more per year than necessary.

Frequently Asked Questions

How much is a $1,000,000 term life insurance policy?

The monthly cost depends on your age, health, gender, and term length. A healthy 30-year-old typically pays $28 to $35/month for a 20-year term; a healthy 50-year-old might pay $105 to $141/month for the same policy. A quick quote from Vellum Life Group will give you an accurate number based on your specific profile.

Can someone with cirrhosis, Parkinson's, or dementia get a million-dollar term life insurance policy?

Serious progressive conditions like these typically make it very difficult or impossible to qualify for a standard $1M term policy. Simplified issue policies may be available, though they generally cap benefits at $250,000 to $500,000. Guaranteed issue policies are an option but typically max out around $25,000 in coverage.

How much does a $1 million term life policy cost per month at age 40?

A healthy 40-year-old non-smoker can expect to pay roughly $45 to $55/month (female and male respectively) for a 20-year term policy, based on Forbes Advisor's published rate data. Your health classification and carrier selection will shift that number up or down.

Do I need a medical exam to get a $1 million term life insurance policy?

Most $1M policies do require a medical exam, though some carriers offer accelerated underwriting that skips the exam for qualifying applicants — coverage up to $1M or more is possible through this path.

Is a million-dollar life insurance policy worth it?

For most families with dependents, a mortgage, or income to replace, the monthly cost is modest relative to the financial protection it provides. At $35/month, a policy protecting $1M in family income is one of the most cost-efficient financial decisions a household can make.

How long should my million-dollar term life insurance policy be?

Match the term to your longest financial obligation — typically 20 to 30 years for families with young children or a significant mortgage. Choosing a shorter term to save on premiums creates a risk of outliving your coverage while obligations remain.