Introduction

Buying a life insurance policy feels like a major accomplishment — and it is. But too many policyholders fall into a "set it and forget it" trap, treating their coverage like a utility bill rather than a living financial tool.

A policy purchased at 25 can leave serious gaps by 45. Your income has grown, your mortgage is larger, you have kids — and that $250,000 term policy you bought when you were single barely covers two years of household expenses today.

That gap is more common than most people realize. According to LIMRA and Life Happens, 40% of American adults — nearly 100 million people — believe they are underinsured or need more coverage.

Closing that gap starts with active policy management. This guide covers how to review your coverage annually, keep beneficiaries current, monitor for lapse risks, and recognize when your needs have outgrown your existing policy.

Key Takeaways

- Review your policy at least once a year and immediately after any major life event

- Beneficiary designations override your will — outdated ones can send money to the wrong person

- Term and permanent policies require very different management approaches

- A 30-day grace period is standard, but lapses end coverage permanently if ignored

- Replacing a policy resets contestability periods and may raise premiums; updating is often the smarter move

Know What You Have: Understanding Your Policy Type

Effective management starts with knowing what you own. The two main categories — term life and permanent life — have completely different structures, and each demands a different management mindset.

Term Life Insurance

Term policies cover a fixed period, typically 10, 20, or 30 years, with no cash value component. Management is straightforward: pay premiums on time, know your expiration date, and understand your options before the term ends.

The conversion feature is where many policyholders get caught off guard. Many term policies include the right to convert to a permanent policy without a new medical exam — a valuable option if your health has changed since you first applied. But conversion windows have deadlines that vary by carrier, and once that window closes, you lose the right permanently.

Key term policy management priorities:

- Track your expiration date and set a calendar reminder 12–18 months before it arrives

- Review your conversion option and its deadline — contact your insurer if you're unsure

- Assess whether your coverage amount still reflects your current income and obligations

Permanent Life Insurance

Permanent policies — whole life, universal life, and variable life — don't expire as long as premiums are maintained. That sounds simpler, but the cash value component introduces management complexity that term policies don't have.

Universal life policies offer flexible premiums, which can become a trap. Pay too little for too long, and the policy becomes underfunded — eventually lapsing even if you believe it's active. Variable policies add investment sub-accounts that require monitoring.

Withdrawals and loans from your cash value reduce your death benefit and can trigger a lapse if balances grow unchecked. It's not a savings account you can dip into freely.

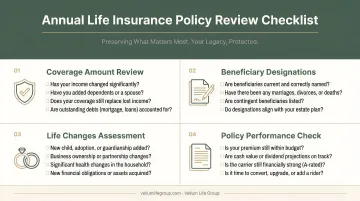

Schedule Annual Policy Reviews

Your life changes continuously. A policy that fit perfectly five years ago may be out of step with your current income, family size, and financial obligations today.

The Illinois Department of Insurance recommends reviewing life insurance at least once a year and after major life events. Annual reviews don't need to be lengthy — but skipping them is how coverage gaps accumulate unnoticed over years.

Vellum Life Group includes structured annual policy reviews as a standard part of their client service at no additional cost. These check-ins cover coverage adequacy, beneficiary status, and any life changes that might affect the policy — consistent attention that catches problems before they compound.

Life Events That Should Trigger an Immediate Review

Don't wait for the annual cycle if any of these occur:

- Marriage or divorce

- Birth or adoption of a child

- Purchase of a home

- Significant income increase or job loss

- Major financial transitions (such as a career change or large asset sale)

- New health diagnosis

- Death of a named beneficiary

What to Assess During Each Review

Use each review to work through four core areas:

- Coverage amount: Does the death benefit still cover income replacement, mortgage balance, education costs, and outstanding debts? Coverage needs tend to grow as families and financial obligations expand.

- Premium affordability: For universal life policyholders, verify that flexible payment amounts haven't inadvertently underfunded the policy over time.

- Riders: Confirm that riders added at purchase — accidental death, waiver of premium, and similar — still apply. Ask your advisor about removing ones that no longer fit; it can lower your premium.

- Cash value (permanent policies): Check the cash value balance and any outstanding loan amounts that could jeopardize the policy's standing.

Keep Your Beneficiary Designations Up to Date

Beneficiary designations are one of the most overlooked steps in policy management, and one of the most consequential. A life insurance beneficiary designation typically overrides your will entirely. If your ex-spouse is still named on a policy from your marriage, your death benefit goes to them — regardless of what your estate plan says.

The Illinois Department of Insurance notes that in many cases, a specific named beneficiary remains controlling even if a descriptive term like "wife" becomes inaccurate after divorce. The Hillman v. Maretta Supreme Court case illustrates this starkly — a named former spouse remained central to a benefit dispute despite a state law attempting to redirect the payout.

Primary vs. Contingent Beneficiaries

- Primary beneficiary — receives the death benefit directly when you die

- Contingent beneficiary — receives the benefit only if the primary beneficiary has already died

Naming at least one contingent beneficiary is a simple but widely skipped step. Without one, benefits may pass through your estate, introducing probate delays and potential complications.

Revocable vs. Irrevocable Designations

The California Department of Insurance distinguishes two types: revocable beneficiaries can be changed at any time without their consent, giving you full flexibility. Irrevocable beneficiaries, which appear in some divorce settlements and legal agreements, cannot be removed without their written consent.

If you're unsure which type you have, check your policy documents or contact your insurer directly.

When to Update Your Beneficiaries

Life changes fast, and your policy should keep pace. Update beneficiary designations after any of these events:

- Marriage or divorce

- Birth or adoption of a child

- Death of a named beneficiary

- Significant change in a beneficiary's financial or personal circumstances

The update process is straightforward — usually a form submitted to your insurer. The harder part is remembering to do it. Building a review into your annual policy check ensures your designations never fall out of date.

Prevent Policy Lapses Before They Happen

A policy lapse ends your coverage immediately — beneficiaries receive nothing, paid premiums aren't refunded, and permanent policyholders can lose accumulated cash value.

Most insurers allow a 30-day grace period after a missed premium before the policy is officially terminated. That window is your first line of defense, so don't ignore payment notices.

For permanent policies, some contracts include an automatic premium loan provision that uses available cash value to cover a missed payment. This can prevent a lapse temporarily, but it's not a permanent fix.

Loan interest accrues on the outstanding balance, and if it grows too large relative to your cash value, the policy can lapse even when you believe premiums are current. MassMutual warns that loan interest can eventually exceed cash value, triggering a lapse and potential tax consequences.

Three practical lapse prevention habits:

- Set automatic premium payments through your bank to eliminate the risk of missed due dates

- Review outstanding loan balances annually as part of your policy review

- Contact your insurer immediately if you're facing financial hardship — reinstatement is possible within a set window, but options narrow quickly once a policy terminates

Know When to Update, Upgrade, or Replace Your Policy

Not every coverage gap requires buying a new policy. Sometimes the right move is adjusting what you already have — changing the death benefit, adding a rider, or modifying a payment frequency. Updating within an existing policy avoids new underwriting, keeps your existing premium rate, and doesn't restart the contestability clock.

Replacement — purchasing a new policy — is a different decision with real trade-offs. The California Department of Insurance cautions that replacement can affect premiums based on older age and changed health, and a new contestability period of up to two years restarts from scratch. That means if you die within two years of the new policy's issue date, the insurer can investigate and potentially deny the claim based on misrepresentation.

Signals that a change is genuinely needed:

- A new dependent or additional financial obligation (mortgage, personal loan)

- A term policy within 12–18 months of expiration with no replacement plan

- Significant income growth that your current coverage no longer reflects

- A permanent policy that no longer fits your long-term goals

For term policyholders approaching expiration, conversion deserves serious consideration before replacement. Converting to a permanent policy within the same contract preserves your original insurability — no new medical exam, no new underwriting required.

If conversion isn't an option and replacement is the right path, working with an independent advisor gives you a broader view of the market. An advisor with access to multiple A-rated carriers — like Vellum Life Group's network of 15+ — can compare rates, products, and terms across insurers, so your decision is based on the full picture rather than a single company's offerings.

Common Life Insurance Management Mistakes to Avoid

Even a well-chosen policy can fall short if it's not managed carefully. These are three of the most common — and costly — mistakes policyholders make.

Keeping Your Policy Location a Secret

The NAIC's Life Insurance Policy Locator has connected consumers with more than $10 billion in unclaimed benefits. That money went unpaid simply because beneficiaries didn't know a policy existed. Store your documents somewhere secure but accessible, and make sure your family or estate executor knows where to find them.

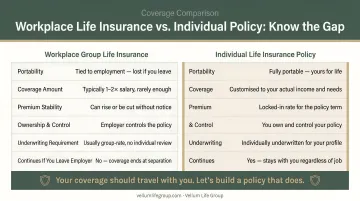

Treating Workplace Coverage as Your Only Policy

LIMRA's 2025 workplace data shows median basic workplace coverage is just $20,000 or 1x salary. Nearly half of households relying solely on that coverage would struggle financially within six months if a wage earner died — and group coverage disappears the moment you leave your job. Treat it as a supplement, not a foundation.

Tapping Cash Value Without a Clear Plan

Withdrawals and policy loans reduce your death benefit and slow cash value growth. If loan balances compound unmanaged, the policy can lapse entirely. Before accessing cash value, review the long-term impact with an advisor — not after the fact.

Frequently Asked Questions

How often should I review my life insurance policy?

At minimum, conduct a formal review once a year. Also review immediately following any major life event — marriage, divorce, a new child, a home purchase, or a significant income change. Think of annual reviews as routine maintenance and life events as the reason to act sooner.

What life events should trigger a life insurance policy update?

Major career changes and significant health changes — beyond the common milestones like marriage, divorce, a new child, or a home purchase — are often overlooked triggers. Any of these can affect your appropriate coverage amount and your beneficiary designations.

What happens if my life insurance policy lapses?

Coverage ends immediately and beneficiaries receive no death benefit. Reinstatement is possible within a specified window, but typically requires evidence of insurability and payment of overdue premiums with interest, and approval is not guaranteed.

Can I change my life insurance beneficiaries at any time?

If your beneficiary designation is revocable, yes — contact your insurer to submit a change form. Irrevocable beneficiaries require written consent from that beneficiary before any change can be made.

Is it better to update my existing policy or buy a new one?

Updating within your current policy is usually preferable: it avoids new underwriting and keeps your existing premium rate intact. Replacing a policy resets the contestability period and may increase premiums due to age or health changes.

Should I rely solely on a group life insurance plan?

No. Group plan coverage typically provides only 1–2x salary, is not portable when the plan changes, and often isn't enough to cover a family's actual financial needs. An individual policy provides coverage that stays with you regardless of your coverage status.