Introduction

Picture this: a family loses a parent unexpectedly. Within 48 hours, they're fielding calls from funeral directors, making decisions about caskets, flowers, and burial plots — all while grieving. Then comes the bill.

According to 2023 NFDA data, the national median cost of a funeral with viewing and burial is $8,300. Add cemetery fees, headstones, and flowers, and a traditional service can climb well past $10,000. For cremation with a service, the median is $6,280 — still a significant expense families rarely see coming.

Two tools exist to avoid leaving that burden behind: final expense insurance and prepaid funeral plans. Both fund your end-of-life costs before you die. But they work differently, suit different situations, and come with risks most people don't realize until it's too late.

This article breaks down how each option works, where each falls short, and a practical framework to help you decide which fits your life.

Key Takeaways

- Final expense insurance pays a cash benefit to a named beneficiary, usable for any end-of-life expense, not just funeral costs

- Prepaid funeral plans pay directly to a specific funeral home, locking in today's prices for pre-selected services

- Insurance offers portability and flexibility; prepaid plans offer price certainty and advance arrangement

- The right choice depends on your priorities — neither option suits everyone

- Many people use both in combination: a prepaid plan for the service, final expense insurance for everything else

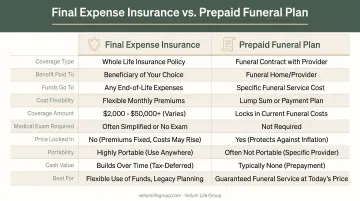

Final Expense Insurance vs. Prepaid Funeral Plans: Quick Comparison

| Feature | Final Expense Insurance | Prepaid Funeral Plan |

|---|---|---|

| Benefit Recipient | Named beneficiary (family member) | Funeral home directly |

| Flexibility of Funds | Any expense — funeral, debt, medical bills | Funeral services only |

| Inflation Protection | No price lock; benefit is fixed | Yes — prices locked at today's rates |

| Medical Requirements | Usually none (simplified or guaranteed issue) | None |

| Portability | Travels with you regardless of location | Tied to a specific funeral home |

| Payment Structure | Fixed monthly premiums for life | Lump sum or installments to funeral home |

| Covers Non-Funeral Expenses | Yes | No |

| Key Risk Factor | Premiums may exceed face value if lived long | Funeral home closure, ownership changes, limited refunds |

Both options address end-of-life costs, but they work differently — and which one fits depends on your priorities, flexibility needs, and family situation.

What Is Final Expense Insurance?

Final expense insurance is a type of whole life insurance designed specifically to cover end-of-life costs. A fixed death benefit — typically ranging from $2,000 to $25,000 — is paid directly to a named beneficiary when the policyholder dies. That beneficiary can use the money however they see fit: funeral services, medical bills, credit card debt, or daily living expenses.

How It Works

- Fixed premiums paid monthly for life — they never increase

- No medical exam required for most policies (simplified or guaranteed issue underwriting)

- Cash value accumulates over time, typically at a modest rate

- Graded death benefit clauses apply to some policies — particularly guaranteed issue products — meaning that if the insured dies from a natural cause within the first two years, the payout is typically limited to premiums paid plus interest, not the full face amount. Accidental death usually receives the full benefit from day one.

Pros of Final Expense Insurance

- Flexibility — beneficiary decides how to use the funds

- Portability — policy is not tied to any funeral home or location

- No medical exam in most cases, making it accessible for seniors with health conditions

- Fast payout — life insurance claims typically settle within days to weeks

- Broader coverage — can cover medical bills, debt, or support surviving family members financially

Cons of Final Expense Insurance

- Cumulative premiums can exceed the policy's face value if the insured lives many more years

- Graded benefit clauses delay full coverage for the first two years on some policies

- Family still makes decisions — beneficiaries handle funeral arrangements during a stressful time

- Inflation exposure — a $10,000 benefit purchased today may not fully cover services that cost $13,000 in 15 years

These tradeoffs — graded periods, inflation risk, premium accumulation — are worth mapping against your specific situation before committing. Vellum Life Group compares options across 15+ A-rated carriers, including Mutual of Omaha, Corebridge Financial, and Foresters Financial, to match policies to your budget and health profile. Schedule a free consultation to explore your options.

What Is a Prepaid Funeral Plan?

A prepaid funeral plan (also called a preneed contract) is a direct agreement between you and a specific funeral home. You pay in advance for particular funeral goods and services — casket, cremation or burial, transportation, viewing — and those services are guaranteed to be delivered when you die.

From there, funds are typically held in a state-regulated trust account or used to purchase a preneed insurance policy managed by the funeral home. When you die, payment goes directly to that funeral home.

How It Works

The defining feature is the price lock: a guaranteed price preneed contract fixes exactly what will be charged for the specific goods and services listed, per Michigan consumer guidance. Funeral costs have been rising — NFDA data shows the burial funeral median climbed from $7,848 in 2021 to $8,300 in 2023, and the 2025 NFDA Cremation and Burial Report found cremation costs increased at an average rate of 2.3% annually over the past decade. Locking in today's price shields your family from that trend.

Pros of Prepaid Funeral Plans

- Price protection against future funeral cost inflation

- Complete control over every detail of your service

- Relieves family of planning decisions during grief

- No ongoing premiums once fully paid

Cons of Prepaid Funeral Plans

- Limited portability — if you move, change your mind, or the funeral home closes, transferring funds can be difficult or impossible

- No flexibility — funds can only be used for the specific services purchased

- Refund policies vary widely — Georgia's 2024 consumer guidance notes that revocable contracts must be refunded within 3 business days, while irrevocable contracts are generally non-refundable

- Doesn't cover anything else — medical bills, debt, and family living expenses are not addressed

The funeral home closure risk is real, not hypothetical. Michigan regulators shut down Cantrell Funeral Home in Detroit in 2018, requiring the assignment of all prepaid contracts to another provider within 60 days. Florida maintains a Preneed Funeral Contract Consumer Protection Trust Fund for qualifying situations when a preneed seller goes out of business — but protections like this vary significantly by state.

The FTC advises consumers to ask specifically whether prepaid funds are protected if a provider closes, and whether the contract can be transferred if you move.

Key Differences That Matter

Who Controls the Money

Final expense insurance puts cash in your beneficiary's hands. They manage the funeral process, negotiate with providers, and handle any excess or shortfall. A prepaid plan pays the funeral home directly — execution of your wishes is guaranteed, but the family has no financial flexibility.

That distinction matters beyond logistics. If your priority is protecting a grieving family from decision fatigue, a prepaid plan delivers that. If you trust a specific person to manage funds wisely, insurance gives them that power.

Inflation Protection vs. Coverage Flexibility

Prepaid plans lock in prices, which has real value as funeral costs rise steadily each year. Final expense insurance doesn't track price inflation — a $10,000 policy stays at $10,000. But the beneficiary can shop around, choose a lower-cost provider, or use any leftover funds elsewhere. If the funeral ends up costing less than expected, that flexibility is an advantage.

Portability and Life Changes

Final expense insurance follows you. Whether you move from New Jersey to Texas, switch funeral homes, or simply change your preferences, the policy remains intact.

A prepaid plan is anchored to one funeral home. If that provider closes, changes ownership, or you relocate, recovering your funds depends on whether your state requires funeral homes to hold prepaid money in a protected trust — and not all states do. Always verify contract terms before signing.

Coverage Scope

Final expense insurance can address the full financial picture after a death. Prepaid plans cover only what's listed in the contract — nothing more. For families expecting broader financial needs after a death, the difference is meaningful:

- Outstanding medical bills left by the deceased

- Credit card balances or joint debts

- Immediate living expenses for a surviving spouse

- Any other cost not tied to the funeral itself

A prepaid plan addresses none of these. Final expense insurance can.

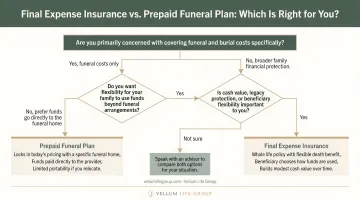

Which Option Is Right for You?

Choose Final Expense Insurance If:

- You want flexibility in how funds are used

- You may relocate or haven't chosen a funeral home

- You want to cover costs beyond the funeral (debt, medical bills)

- You're not ready to make detailed funeral arrangements today

- You want to leave financial support to a loved one, not just pay a funeral home

Choose a Prepaid Funeral Plan If:

- You have a specific funeral home you trust and plan to stay local

- You want every detail of your service arranged exactly as you specify

- Price lock against inflation is a top priority

- You want to remove all planning burden from your family completely

Consider Both

Some people use a prepaid plan to lock in specific funeral service details, then add a final expense insurance policy to cover everything else — debt, medical bills, and ongoing family expenses. This combination offers both certainty and flexibility.

If you're unsure which path fits your situation, Eva Ikonomakos at Vellum Life Group can help you think it through. She works with 15+ A-rated carriers and takes a pressure-free approach to finding coverage that actually matches your needs. Call 917-363-3554 or book a free consultation to get started.

Frequently Asked Questions

Can you have both final expense insurance and a prepaid funeral plan?

Yes — many people use both. A prepaid plan handles the specific funeral service details and locks in pricing, while final expense insurance covers remaining costs like medical bills, debt, and family living expenses. The combination gives you both certainty and financial flexibility.

What happens to a prepaid funeral plan if the funeral home closes?

Protection varies by state and contract terms. Some states, like Florida, maintain a consumer protection fund for qualifying claims — others offer limited coverage. Before purchasing, ask whether funds are held in a state-regulated trust and what happens if the provider closes.

Does final expense insurance cover all funeral costs?

Coverage depends on the benefit amount you choose. Policies typically range from $2,000 to $25,000, and the median cost of a funeral with burial is currently $8,300. Select an amount that matches anticipated funeral costs in your area — then factor in any other expenses you want to cover.

Is final expense insurance worth it if I already have life insurance?

Only if your existing coverage can handle both funeral costs and other financial obligations. Some people add a small final expense policy specifically so funeral costs don't deplete a larger benefit intended for income replacement or mortgage payoff.

Can I change or cancel a prepaid funeral plan after signing?

It depends on your contract type. Revocable contracts generally allow cancellation with a refund; irrevocable contracts often do not. Ask about refund rights before signing.

How much does final expense insurance typically cost per month?

Premiums vary by age, health, and coverage amount. According to MoneyGeek's 2026 benchmark, a 65-year-old woman pays approximately $48/month and a 65-year-old man approximately $58/month for $10,000 in coverage. Premiums are fixed for life once the policy is issued.